Download

1 / 9

90 likes | 309 Views

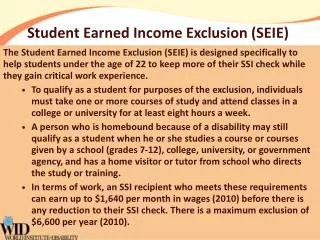

Two-month Earned Income Exclusion. Introduction. When a KTAP/ET recipient reports new earnings, he/she is potentially eligible for a 2-month exclusion of wages. This exclusion began as an incentive for KTAP recipients to become employed.

E N D

Introduction When a KTAP/ET recipient reports new earnings, he/she is potentially eligible for a 2-month exclusion of wages. This exclusion began as an incentive for KTAP recipients to become employed. This presentation will explain the rules for allowing the 2-month earned income exclusion, and demonstrate system entry on KAMES.

General Rules • The 2-month earned income exclusion is allowed for each active adult KTAP member. • A recipient can only receive the 2-month earned income exclusion ONCE in a lifetime. • The recipient chooses when to use the exclusion. They may choose to save it for a future job.

Who Gets It? • Each active adult member of the case is eligible for the exclusion. (Including sanctioned or penalized members) • A teen parent under 18 is only eligible for the exclusion if he/she is coded the SR (M03) or SP (M04) in the KTAP case. (If his/her wages are not otherwise excluded due to school attendance) • A teen parent age 18 or 19 is considered an adult, and is eligible for the exclusion, if appropriate.

Who Doesn’t? • This exclusion does NOT apply to new approvals. • This exclusion does NOT apply to new members added to the case with wages. • The earnings are NOT excluded in the related food stamp case. • If not coded M03 or M04, a teen parent or a teen child under 18 years old is NOT eligible for the 2-month exclusion.

Timely Reporting • The employment must be reported timely (within 10 days), and must be verified in order to receive the 2-month earned income exclusion. • If the individual fails to verify the income, discontinue the KTAP case for failure to return verification, and the exclusion is not given. • If the individual provides all the needed verification in the adverse action period, and the KTAP case is reinstated, the 2-month exclusion of wages is allowed.

Applying the Exclusion • The first month of exclusion begins when the K-TAP check would be affected had the earnings not been excluded. • For example: Nelson is employed on the 10th of January and reports it to the agency timely. His 2-month exclusion begins the following month of February, as the change could be made prior to cut-off, and would end in March. • Or if Nelson began working on the 27th of January and reported it timely, his excluded months would be March and April, as the change couldn’t be made until after January cut-off.

Applying the Exclusion • Two full months earnings are excluded regardless of the amount of income, number of hours, or the type of work. • The 2 months income excluded are consecutive, not cumulative. • The 2-month earned income exclusion applies to only one job. • If an individual chooses to use the exclusion for one job, and then gets a second job, the $30 and 1/3 or $30 disregard may be applied to the second job. • Track the 2-month earned income exclusion manually on form PAFS-116, Supplement A, Tracking Log.

KAMES System Entry Do NOT wait for verification before entering wages on KAMES! Show the months the earned income is excluded in the “KTAP/ET Exclude Begin” and “End” fields. KAMES excludes the income from the IM case, and counts it in the FS accordingly.