Download

1 / 17

190 likes | 502 Views

FORWARD AND FUTURES CONTRACTS. Obligation to buy or sell an asset at a future date at a price that is stipulated now Since no money changes hands now, contract value should be zero

E N D

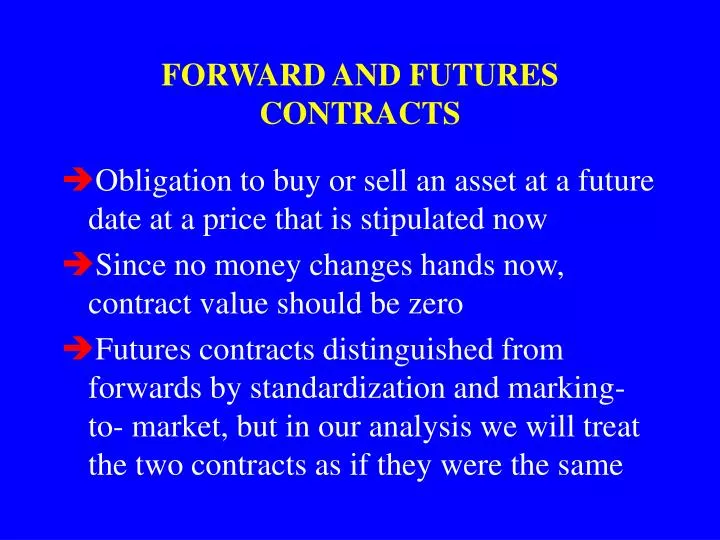

FORWARD AND FUTURES CONTRACTS • Obligation to buy or sell an asset at a future date at a price that is stipulated now • Since no money changes hands now, contract value should be zero • Futures contracts distinguished from forwards by standardization and marking-to- market, but in our analysis we will treat the two contracts as if they were the same

NO-ARBITRAGE SPOT-FORWARD PRICING RELATIONSHIP F0T = forward price on underlying asset to be delivered at T S0 = spot price of underlying asset Assume: underlying asset makes no cash payments between now and T

If F0T > S0(1+rf)T: Borrow S0 Buy underlying asset Sell underlying asset for future delivery If F0T < S0(1+rf)T: Sell underlying asset short Invest in riskless asset Buy underlying asset for future delivery WHAT IF IT DOESN’T HOLD?

Long Bill (due 12/22) discount = 4.48 Price = (1-.0448(139/360))mil = 982,702.22 Short Bill (due 9/22) discount = 4.13 Price = (1-.0413(48/360)) =.99449333 T-BILL SPOT FUTURES ARBITRAGE

Futures (due 9/22) Quote = 95.38 discount = 100-95.38 = 4.62 Price = (1-.0462(91/360))mil = 988,321.67 Buy 1 mil face val. long bills: 982,702.22 Buy 988,321.67 face value short bills: .99449333(988321.67) = $982,879.31 Buy 1 mil face 91 day bills for delivery 9/22: 988,321.67 T-BILL SPOT FUTURES ARBITRAGE

SPOT-FORWARD PRICING (Underlying asset has cash payout) • Discrete-time version • d = cash flow payout rate (e.g., dividend yield)

SPOT-FORWARD PRICING (Underlying asset has cash payout) • Continuous-time version • d = instantaneous cash flow payout rate (e.g., dividend yield)

8/5 S&P 500 index spot = 457.09 futures = 459.8 (12/16 delivery - 129 days from now) 129-day T-bill yield = 4.774% S&P div. yld. = 2.83% EXAMPLE: STOCK INDEX ARBITRAGE

CALENDAR SPREADS • We have two futures contracts on the same asset but with different delivery dates, near (n) and far (f) • How should the contracts be priced relative to one another?