Download

1 / 42

420 likes | 436 Views

Gross Domestic Product. EQ: how are gross domestic product and gross national product influenced by business cycles? In this lesson, students will be able to identify characteristics of the Gross Domestic Product. Students will be able to identify and/or define the following terms:

E N D

Gross Domestic Product EQ: how are gross domestic product and gross national product influenced by business cycles? In this lesson, students will be able to identify characteristics of the Gross Domestic Product. Students will be able to identify and/or define the following terms: Gross Domestic Product (GDP) Real GDP Inflation Durable Goods E. Napp

Do you remember the Invisible Hand? It was the idea that the economy would always fix itself. E. Napp

But when the Great Depression happened, the economy didn’t seem to fix itself. E. Napp

The Effects of the Great Depression on Economists: • The Great Depression taught economists that they needed some way of tracking the nation’s economy. • By tracking the nation’s economy, economists could determine if the economy was in danger of a recession or a depression and could try to apply economic policies to prevent such hardships from occurring. E. Napp

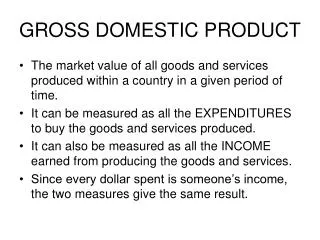

The Gross Domestic Product (GDP) is a tool for tracking macroeconomic progress. E. Napp

Gross Domestic Product (GDP) • The Gross Domestic Product is the dollar value of all final goods and services produced within a country’s borders in a given year. • In order for a good to be included in a nation’s GDP, it must be made in that country. • It doesn’t matter if the factory is owned by a foreign company as long as the factory is located in the country where GDP will be calculated. E. Napp

By tracking GDP, economists can tell whether an economy is growing (expanding) or shrinking (contracting). E. Napp

Real GDP • While nominal GDP is expressed in current prices, real GDP is adjusted for inflation. • Inflation means rising prices. The problem with GDP is it could appear to rise when in reality only prices rose. • In other words, one million in1970 dollars is not the same as one million in 2006 dollars. The 2006 dollars must be adjusted to 1970 dollars in order to effectively compare the two amounts. E. Napp

Real GDP is GDP that has been adjusted for inflation. E. Napp

Durable and Nondurable Goods • The goods included in GDP are durable and nondurable goods. • Durable goods are goods that last for a relatively long time, such as refrigerators and cars. • Nondurable goods last for a short period of time like food and paperback books. E. Napp

A refrigerator is a durable good. It lasts a long time. E. Napp

Food is a nondurable good. It does not last a long time. E. Napp

Just like going for your yearly physical allows you to track your health and prevent more serious problems from occurring, GDP tracks the economy’s health. E. Napp

Questions for Reflection: • What did economists believe about the economy before the Great Depression? • What is Gross Domestic Product or GDP and why is it important? • Why do economists adjust GDP for inflation and what is this adjusted GDP called? • What is the primary difference between durable and nondurable goods? E. Napp

Business Cycle In this lesson, students will be able to identify characteristics of the business cycle. Students will be able to identify and/or define the following terms: Business Cycle Expansion Peak Contraction Trough E. Napp

A business cycle is a period of macroeconomic expansion followed by a period of contraction. E. Napp

The Four Phases of a Business Cycle • There are four phases in a business cycle: Expansion: a period of economic growth Peak: the height of the expansion Contraction: a period of economic decline Trough: the lowest point of the contraction E. Napp

When an economy is expanding or growing, many people have jobs and many goods and services are being produced and sold. At the peak of the expansion, Gross Domestic Product is as high as it will go for that particular business cycle. E. Napp

During a period of contraction, more people are unemployed and fewer goods and services are being produced and sold. Not all contractions are equally severe. E. Napp

Recessions and Depressions • Each phase of the business cycle is determined by monitoring Gross Domestic Product. • A contraction that lasts for at least six months is called a recession. • A particularly severe and long contraction is called a depression. E. Napp

The Great Depression was the most severe economic contraction in the history of the world. It permanently changed the way economists think. E. Napp

Factors Which Affect the Business Cycle • The following four factors can affect the business cycle: Investment in Businesses Interest Rates Consumer Expectations External Shocks E. Napp

The more money people invest in businesses, the more money businesses have to grow. Investment affects the business cycle. E. Napp

Interest is the price of borrowed money. When interest rates are high, people borrow less. Businesses borrow less too. Interest rates affect the business cycle. E. Napp

When people are optimistic about the future, they spend more money. Optimism affects the business cycle. E. Napp

External shocks can be positive or negative. An earthquake is a negative external shock. It affects the business cycle. E. Napp

Throughout American history, there have been many business cycles. E. Napp

Questions for Reflection: • Define the business cycle. • What are the four phases of the business cycle and explain each phase? • What are the four factors that affect the business cycle and how does each factor affect the business cycle? • What is the relationship between Gross Domestic Product and the four phases of the business cycle? E. Napp

Economic Growth In this lesson, students will be able to identify factors which lead to macroeconomic growth. Students will be able to identify and/or define the following terms: Real GDP per capita Capital Deepening Savings Rate Technological Progress E. Napp

Our world’s population has increased greatly in the last 200 years. E. Napp

Population and the Economy • A nation’s population tends to grow. • Gross Domestic Product must keep up with the population growth rate. • If the economy does not continue to grow as population grows, unemployment and hunger will increase. E. Napp

The economy is like a pie. The bigger the pie, the more people can be fed. E. Napp

Real GDP Per Capita • It is important to remember that real GDP is GDP that has been adjusted for inflation. • Per capita means per person. • Therefore, real GDP per capita is a way of determining how much money each person in a society would receive if wealth from GDP was divided equally among the people of that nation. E. Napp

A country with a high standard of living has a high real GDP per capita. E. Napp

Capital Deepening • One way to increase economic productivity is through capital deepening. • Capital deepening is the process of increasing the amount of capital per worker. • Better educated workers can produce more output per hour of work. E. Napp

Better educated workers are more productive workers. Education helps the economy to grow. E. Napp

Savings Rate • Money that is saved is available for investment. • The savings rate is the portion of disposable income spent to the portion of disposable income saved. • A country with a higher savings rate will be more likely to experience economic growth because more money will be available to invest in businesses. E. Napp

The more money citizens of a country save, the more money is available for businesses to expand. E. Napp

When education rates and savings rates increase, the economy grows. And when the economy grows, people have jobs, shelter, food, and the comforts of life. E. Napp

Technological Progress • Another key source of economic growth is technological progress. • This is an increase in efficiency gained by producing more output. • Email replacing slower “snail mail” is an example of technological progress. E. Napp

Technological progress like email greatly increases business efficiency. Greater efficiency means greater profits. E. Napp

Questions for Reflection: • Why must the economy continue to grow as population increases? • Why is it important for economists to calculate real GDP per capita? • What is capital deepening and how does it affect economic growth? • How does the savings rate help the economy to grow? • Why is technological progress important? E. Napp