Download

1 / 22

300 likes | 659 Views

Commercial Paper Overview. January 20, 2012. Strictly Private and Confidential. Table of Contents. 1. Overview of Commercial Paper.

E N D

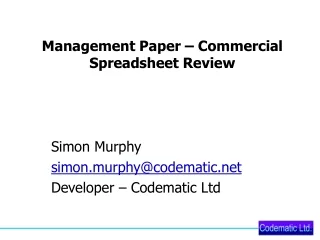

Commercial Paper Overview January 20, 2012 Strictly Private and Confidential

The U.S. CP market is a large and liquid market with approximately $1.0 trillion in outstandings from three main sectors: bank/financial, non-financial and ABCP. Overview of Commercial Paper (“CP”) 1 Overview of Commercial Paper

CP provides issuers with a cost effective, flexible capital markets funding tool. Advantages of Issuing CP 2 Overview of Commercial Paper

Who Issues Commercial Paper? Breakdown by Type Breakdown by Rating Breakdown by Maturity (Days) Source: Federal Reserve, Citi and Moody’s 3 Overview of Commercial Paper

U.S. CP is purchased by a broad group of investors including 2a-7 Money Funds, asset managers, corporate treasuries, banks, municipalities and insurance companies. Who Buys U.S. Commercial Paper? U.S. CP Outstandings vs. Money Fund Holdings Sample U.S. CP Investor Breakdown Source: Citi Source: iMoneyNet and Federal Reserve • 2a-7 money funds and related fund complexes are the largest liquidity providers in the U.S. CP market • Money Funds are SEC-regulated mutual funds that are required to invest in low risk securities such as government and agency securities, repurchase agreements and U.S. CP • In January 2010, the SEC adopted new rules intended to strengthen the framework for money funds. The new rules became effective in May 2010 and have been phased in since then 4 Overview of Commercial Paper

Historical U.S. CP Outstandings: An Unprecedented Drop -53% Total U.S. CP: $1,010 BN -70% Financial: $480 BN Total ABCP: $352 BN Non-Financial: $178 BN Tier-2: $69 BN Source: Federal Reserve as of 1/11/12 ABCP and Financial Outstandings Non-Financial and Tier-2 Outstandings 5 Overview of Commercial Paper

Historical U.S. CP Spread Volatility September/October 2008: Government extends extraordinary support to money markets (AMLF, CPFF) August 1998: Russian Financial Crisis followed by the collapse of LTCM September 2008: Lehman Brothers files for bankruptcy and the Reserve Primary Fund “breaks the buck” September 11, 2001 August-December 2011: U.S. debt ceiling negotiations and European sovereign debt crisis August 2007: Concerns over subprime mortgage exposure disrupts global financial markets (including ABCP) November-December 1999: Y2K fears cause large cash withdrawals from financial markets Source: Federal Reserve 6 Overview of Commercial Paper

U.S. CP programs have fairly standardized characteristics allowing for easy comparison among different issuers. Program Establishment Considerations 7 Overview of Commercial Paper

Best practice for CP issuers is to have two short-term ratings. Short-term ratings are correlated to long-term ratings. Commercial Paper Ratings Fitch’s Categories Moody’s Categories Standard & Poor’s Categories 8 Overview of Commercial Paper

Commercial Paper Documentation 9 Overview of Commercial Paper

U.S. CP is sold through three exemptions from the registration requirements of the Securities Act of 1933 - Sections 3(a)(3), 3(a)(2) or 4(2). CP sold pursuant to any of these exemptions is also exempt from the registration requirements of the 1934 Act. Securities Act of 1933 Exemption Overview • Section 3(a)(3) is known as the commercial paper exemption under the ‘33 Act. To qualify for this exemption the commercial paper must satisfy the following criteria: • mature in 9 months or less • be of prime quality evidenced by an investment grade rating by at least one U.S. nationally recognized rating agency • proceeds from the sale of commercial paper must be used for working capital and pass the “current transaction test” • In applying the current transaction test, tracing of proceeds is not required. It is sufficient if an issuer, on a consolidated basis, has current assets and operating expenses for the previous twelve months in an amount equal to or exceeding the amount of its outstanding commercial paper • Section 4(2) is often referred to as the private placement exemption under the ‘33 Act • requires that notes only be sold to large, sophisticated investors (e.g., QIBs) or accredited investors • 4(2) exemption allows for more flexible use of funds such as acquisition financing or stock repurchases • Section 3(a)(2) is a less frequently used exemption and applies to the direct or guaranteed obligations of institutions already regulated by the Federal Reserve and State Banking Commission, or the Comptroller of the Currency • used primarily in the case of letter of credit backed CP, which allows an issuer to “borrow” a high quality bank’s ratings in the form of a letter of credit in order to gain access to the CP market 10 Overview of Commercial Paper

Size of the Asset-Backed Commercial Paper Market Global ABCP Outstandings The Global ABCP sector has contracted by over 70% since it’s peak in July 2007. Peak – Jul-07: $1,475 Billion Current – Jan-12: $387 Billion Source: Federal Reserve, Dealogic – CP Ware, as of 1/11/12 11 Introduction to Asset-Backed Commercial Paper

Commercial Paper Market Breakdown U.S. Commercial Paper Euro Commercial Paper July 2007 July 2007 January 2012 January 2012 Source: Federal Reserve, Dealogic – CP Ware, as of 1/11/12 12 Introduction to Asset-Backed Commercial Paper

Asset-Backed Conduit Definitions ABCP Structural Elements 13 Introduction to Asset-Backed Commercial Paper

Basic “Multi-Seller” Partially Supported Conduit Structure Seller’s Piece Seller’s Piece Seller’s Piece Seller’s Piece Pool #1 Pool #2 Pool #3 Pool #4 Asset Sales Cash Liquidity “Special Purpose Vehicle” Conduit Manager Program Credit Support Cash Commercial Paper Issuance Dealer Investors Multi-seller programs comprised 68% of ABCP market as of 4Q2011 14 Introduction to Asset-Backed Commercial Paper

Structured Investment Vehicles: A Simple Overview AAA / AA / A Securities Portfolio MTNs CP SIV Manager “Special Purpose Vehicle”/Operating Company Sub-debt Equity 15 Introduction to Asset-Backed Commercial Paper

ABCP Program Type Description ABCP Market Post 2007 “Credit Crunch” • Multi-Seller:Combines assets from multiple sellers into one diverse portfolio • In “multi-seller” programs, the Sponsor is often a major bank that offers selected clients an opportunity to sell receivables or other financial assets into the SPV • Assets:Term and trade receivables, can also hold securities (i.e., Amsterdam Funding, CAFCO, CHARTA) • Single-Sellers: Purchases assets from one originator/seller • Assets: Mortgages, Credit Cards, Auto Loans, etc. (i.e., DAKOTA, Amstel) • Securities Arbitrage Vehicles: Finances long term securities with short term Commercial Paper • Assets: Highly rated assets such as ABS, CLO, CDO, RMBS, etc. (i.e., Curzon, Solitaire, Surrey Funding) No Longer in the ABCP Market • Structured Investment Vehicles (SIVs): Similar to Securities Arbitrage but with several structural differences such as dynamically sized liquidity (usually less than 100% of the CP), credit enhancement through subordinate tranches, and a mark to market asset portfolio • Assets: Highly rated assets such as ABS, CLO, CDO, RMBS, and Corporate/Bank Paper • Extendible: Extendible feature of up to a total of 390 days from date of CP issuance with a penalty yield step up of an average of 1-month Libor +25 bps (e.g. 7-day CP can extend 1 time up to 383 days). Programs tend to have assets which either can generate cash flow, be easily liquidated or have liquidity banks to pay off CP investors at the end of the extension period, subject to an asset-based formula • Assets: Mortgages, term and trade receivables, etc. • CDO-CP:Managed by private investment companies,banks and insurance companies to finance a portfolio of assets. This structure issues different tranches of liabilities (most senior is CP). This structure benefits from strong liquidity put / interest swap to highly rated Counterparty equal to 100% of CP issuance • Assets: Highly rated assets such as ABS, CLO, CDO, RMBS, etc. 16 Introduction to Asset-Backed Commercial Paper

Moody’s Global ABCP Market Breakdown June 2007 Global ABCP Breakdown by Program Type 2008 Global ABCP Breakdown by Program Type 2010 Global ABCP Breakdown by Program Type 2011 Global ABCP Breakdown by Program Type Source: Moody’s ABCP Program Index (3Q07, 1Q09, 1Q10, 4Q11) 17 Introduction to Asset-Backed Commercial Paper