Download

1 / 34

340 likes | 491 Views

Why do property values melt when funds go into liquidation?. Sebastian Gläsner 18.06.2011. Agenda. Performance of funds in liquidation Data and research design Testing hypothesis on drivers of capital growth of standing investment properties of GOEFs

E N D

Why do property values melt when funds go into liquidation? Sebastian Gläsner 18.06.2011

Agenda • Performance of funds in liquidation • Data and research design • Testing hypothesis on drivers of capital growth of standing investment properties of GOEFs • H1: German valuation practice results in smoothed capital growth • H2: High NAV-discount is associated with negative capital growth • H3: Property acquisition date in boom phase results in negative capital growth thereafter • H4: Properties of funds in liquidation show negative capital growth

Redemption stops of German open ended funds • As to March 2011, 22 GOEFs open for retail investors comprise 75.4 bn. EUR NAV • Nine out of those funds with NAV of 21.7 bn. EUR have stopped the redemption of shares • Two funds with 1.8 bn. EUR NAV are in liquidation • Funds in liquidation recently have shown very negative performance, which is unprecedented in the 50-year-history of German open ended funds Public data

Performance of funds in liquidation NAV-base performance • While the performance of the group of funds with redemption stops is only slightly worse than the performance open funds, funds in liquidation loose about a third of their value in comparison to the third quarter 2008 Public data Source: NAV-publications of the funds

Performance of funds in liquidation Discounts on the NAV at the secondary market • Besides poor NAV-based performance, funds in liquidation also show a high discount on NAV • Within the first year of redemption stops, discounts were lower than 10% • Starting 2010, discounts increased up to 50% • Investors forced to or willing to sell off their shares of funds in liquidation lost more than 50% of their investment over the last two years Public data Source: Stock exchange Hamburg

Agenda • Performance of funds in liquidation • Data and research design • Testing hypothesis on drivers of capital growth of standing investment properties of GOEFs • H1: German valuation practice results in smoothed capital growth • H2: High NAV-discount is associated with negative capital growth • H3: Property acquisition date in boom phase results in negative capital growth thereafter • H4: Properties of funds in liquidation show negative capital growth

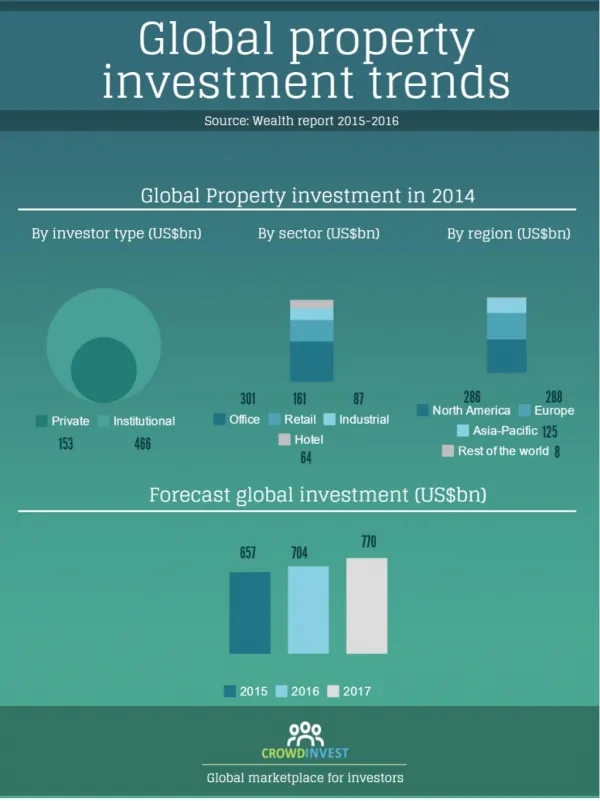

Focus on French and Dutch offices Asset allocation of GOEFs as to 12/2010 • Germany, France, UK and the Netherlands are the biggest investment markets of German funds • Real estate performance of GOEFs is analysed using French and Dutch office investments because: • Office properties are the predominant assets in GOEF portfolios and analysis is limited for comparability reasons • German properties are not being analysed, as the IPD dataset used for comparison is too much influenced by GOEFs • UK properties are not being analysed due to very few investments held by the two funds in liquidation • Dutch properties may interest audience in Eindhoven Public data Source: BVI

Data: Fund reports • German funds publish capital values (and other information) of each single asset on a yearly basis since 2006 • The reports are in the public domain, and no confidentiality issues arise, which is in sharp contrast to IPD client data • When using IPD client data as a benchmark, confidentiality is maintained on fund level and on property level • The capital values of standing investments of French and Dutch offices have been collected from publicly available sources to calculate the annual capital growth rate (cg) • Four frequently stated hypotheses on German funds are being investigated

Agenda • Performance of funds in liquidation • Data and research design • Testing hypothesis on drivers of capital growth of standing investment properties of GOEFs • H1: German valuation practice results in smoothed capital growth • H2: High NAV-discount is associated with negative capital growth • H3: Property acquisition date in boom phase results in negative capital growth thereafter • H4: Properties of funds in liquidation show negative capital growth

Distribution of capital growth France GOEFs • Turning point 2010, peaks at 0% cg, fat tails at -5% and +5% in 2006 • Mean returns range between -1.4% and 6.5%, compared to -5.3% and 9.9% of local investors Public data Source: Annual fund reports

Distribution of capital growth The Netherlands GOEFs • Turning point 2009, peaks at 0% cg, fat tails at -5% and +5% in 2006 • Mean returns range between -1.9% and 1.5%, compared to -5.2% and 4.8% of local investors Public data Source: Annual fund reports

Valuation inertia Analysis of value changes of +-1% of GOEFs, FR+NL • Classes: <-5%<-1%<1%<5%<20% • Areas of histogram misleading regarding density • In the years 2007 and 2008 about one fifth of all properties showed a capital growth between -1% and +1% • In the years 2009 and 2010 more than one third of all properties showed a capital growth between -1% and +1% • Funds in liquidation (red figures): • Five out of eight properties (63%) maintain (+-1%) their values in 2009 • Only one out of nine (11%) maintains its value in 2010 • Sum up: Similar valuation inertia of funds in liquidation in 2008 and 2009, differences in 2010 20% 22% 2/2 2/4 1 1 red = # properties of funds in liquidation Public data 33% 5/8 37% 6/9 1 1 1 2 1 Source: Annual fund reports

Valuation inertia Analysis of value changes of +-1% of GOEFs in France • Classes: <-5%<-1%<1%<5%<20% • Areas of histogram misleading regarding density • 2007: Strong appreciation, 20% stable • 2008: Tendency towards appreciation, 32% stable • 2009: Indifference, 44% stable • 2010: Strong tendency towards (minor) depreciation, 30% stable 20% 13% Public data 26% 41% Source: Annual fund reports

Valuation inertia Analysis of value changes of +-1% of local investors in France • Classes: <-40%<-20%<-5%<-1%<1%<5%<20%<40% • Areas of histogram misleading regarding density • Lower proportion of stable capital values in times of positive value changes in 2007 • Highest proportion of stable capital values in years of market turning 2008 and 2010 • Maximum of 16% stable capital values in 2010 much lower than 41% stable capital value of German funds in 2010 13% 5% IPD data 16% 11% Source: IPD

Valuation inertia Analysis of value changes of +-1% of GOEFs in The Netherlands • Classes: <-5%<-1%<1%<5%<20% • Areas of histogram misleading regarding density • 2007: Indifference between appreciation and depreciation, 25% stable • 2008: Tendency towards appreciation, 32% stable • 2009: Indifference, 44% stable • 2010: Strong tendency towards (minor) depreciation, 30% stable 25% 32% Public data 44% 30% Source: Annual fund reports

Valuation inertia Analysis of value changes of +-1% of local investors in The Netherlands • Classes: <-40%<-20%<-5%<-1%<1%<5%<20%<40% • Areas of histogram misleading regarding density • Lower proportion of stable capital values in times of negative value changes 2008 and 2009, highest in 2010 • Maximum of 17% stable capital values in 2010 much lower than 44% stable capital value of German funds in 2009 13% 6% IPD data 17% 7% Source: IPD

H1: German valuation practice results in smoothed capital growth Sum up • With the exception of France in 2008 where results match, properties of GOEF show a much higher proportion of stable capital values than properties of local investors • The average rate of unchanged capital values of GOEF properties reach 25% in France compared to 11% of local investors, and 33% in The Netherlands compared to 11% of local investors • As the proportion of stable capital values of GOEFs is double to three times the figure of local investors, H1 seems plausible Source: IPD

Agenda • Performance of funds in liquidation • Data and research design • Testing hypothesis on drivers of capital growth of standing investment properties of GOEFs • H1: German valuation practice results in smoothed capital growth • H2: High NAV-discount is associated with negative capital growth • H3: Property acquisition date in boom phase results in negative capital growth thereafter • H4: Properties of funds in liquidation show negative capital growth

Explaining capital growth by NAV-discount Discounts on the NAV at the secondary market • Three groups are formed: • Funds with avg. discounts lower than 20% over the last 12 months • Funds with discounts above 20% • Funds in liquidation Public data Source: Hamburg stock exchang

Capital growth France Local investors vs. GOEFs • Indices calculated using capital weighted individual property growth rates • French offices held by local investors strongly appreciate in 2006 and 2007, and strongly depreciate in 2008 and 2009, recovery in 2010 • French offices held by German funds appreciate from 2006 until 2009, and depreciate in 2010 • Offices held by funds in liquidation depreciate in 2009 and strongly depreciate in 2010 Public data IPD data Source: IPD 2011, annual fund reports

Capital growth Netherlands Local investors vs. GOEFs • Dutch offices held by local investors strongly appreciate in 2006 and 2007, and strongly depreciate in 2008 and 2009, still depreciate in 2010 • Dutch offices held by German funds appreciate from 2006 until 2008, and depreciate in 2010 • Offices held by funds in liquidation depreciate in 2009 and strongly depreciate in 2010 Public data IPD data Source: IPD 2011, annual fund reports

Influence on NAV-Discount on valuation? Open funds vs. redemption stop w/o funds in liquidation • When excluding funds in liquidation from the high-discount group, differences diminish • France: Open funds’ properties depreciate slightly less in 2009 and 2010 than both groups of redemption stop • Netherlands: High discounts on NAV are associated with about one percentage point more depreciation from 2007 to 2010 Public data Source: Annual fund reports

H2: High NAV-discount is associated with negative capital growth Sum up • Only minor effects of NAV-discount on capital growth • H2 cannot be affirmed Source: IPD

Agenda • Performance of funds in liquidation • Data and research design • Testing hypothesis on drivers of capital growth of standing investment properties of GOEFs • H1: German valuation practice results in smoothed capital growth • H2: High NAV-discount is associated with negative capital growth • H3: Property acquisition in a boom phase results in negative capital growth thereafter • H4: Properties of funds in liquidation show negative capital growth

Accounting for portfolio differences Explaining capital growth by hard property characteristics • Only factors taken into account that are not influenced by appraisal assumptions • In France, long leases are associated with positive capital growth, and later acquired properties tend to depreciate in 2009 and 2010 • In the Netherlands, only lease duration in 2009 has a significant positive impact, but much lower sample size • No impact of economic building year Public data

Accounting for portfolio differences Explaining French capital growth by acquisition date • Negative impact of newly purchased properties in 2009 and 2010 • French properties of funds in liquidation have been acquired recently and fall into the pattern 1998 2001 2004 2007 1998 2001 2004 2007 Public data 1998 2001 2004 2007 2010 1998 2001 2004 2007 2010

Accounting for portfolio differences Explaining Dutch capital growth by acquisition date • No significant negative impact of newly purchased properties • Dutch properties of funds in liquidation show negative capital growth in 2010, regardless of the acquisition date 1992 1998 2004 1992 1998 2004 Public data 1992 1998 2004 2010 1992 1998 2004 2010

H3: Property acquisition date in boom phase results in negative capital growth Sum up • Some evidence found for French properties, but no dominant pattern • Fund belonging has to be added as control variable, because funds in liquidation tend to have acquired their properties at a late point of time Source: IPD

Agenda • Performance of funds in liquidation • Data and research design • Testing hypothesis on drivers of capital growth of standing investment properties of GOEFs • H1: German valuation practice results in smoothed capital growth • H2: High NAV-discount is associated with negative capital growth • H3: Property acquisition date in boom phase results in negative capital growth thereafter • H4: Properties of funds in liquidation show negative capital growth

Explaining capital growth Model including funds as dummy variables • No significant influence of construction year and vacancy rate on capital growth • Purchase date only significant when looking at the entire period (weak effect) • Rent multiplier and rental value per sqm positively correlated to cg • Market value per sqm negatively correlated to cg • Funds in liquidation showed lower cg over the entire period, but DEGI EUROPA had higher cg rates in 2007 • Out of 20 funds not in liquidation, only one fund showed significantly lower cg rates in 2010 • Inclusion of fund dummies into the regression model strongly increase the explanatory power in 2007 and 2010 Public data

H4: Properties of funds in liquidation show negative capital growth Sum up • Both funds in liquidation show significantly lower capital growth rates in 2010 • H4 cannot be rejected Source: IPD

Summary I • H1: German valuation practice results in smoothed capital growth • Evidence: Percentage of stable property values of GOEFs between 2007 and 2010 about factor 2 to 3 higher • Interpretation: Given the strong economic crisis and recovery of the period, valuations of GOEFs seem to smooth capital growth • H2: High NAV-discount is associated with negative capital growth • Evidence: No evidence found • H3: Property acquisition date in boom phase results in negative capital growth thereafter • Evidence: Evidence found only for French properties in 2009 and 2010, but when controlling for fund belonging, no single years but the 2007-2010 period reaches significance • Interpretation: Effect weaker than often assumed, but valuations of funds not in liquidation may show the assumed depreciations in the years to come

Summary II • H4: Properties of funds in liquidation show negative capital growth • Evidence: Both funds in liquidation show significantly lower capital growth rates of their properties in 2010, and the regression model for 2010 reaches 40% R² when including fund dummies, and 0% R² when not • Interpretation: The fact that despite limited sample sizes of the French and the Dutch properties of the individual funds the fund belonging variable of the funds in liquidation is highly significant shows that liquidation is the central driver of capital growth of GOEFs in 2010 • Research outlook • The analysis of the valuations as presented in combination with the transaction results of the portfolios being sold at the moment will show to which extend valuations match transaction prizes. At this point of time, for the two funds in liquidation only one sales prize of Dutch and French standing investments was available

Thank you for your attention! Sebastian Gläsner 18.06.2011