Download

1 / 9

90 likes | 198 Views

The Illusion of Precision in Target-date Funds. Presenters Stephen Sexauer, Chief Investment Officer, Allianz Global Investors Solutions; Paul Pietranico, CFA , Senior Vice President, Portfolio Manager, and Director of Research, Allianz Global Investors Solutions; and

E N D

The Illusion of Precision in Target-date Funds Presenters Stephen Sexauer, Chief Investment Officer, Allianz Global Investors Solutions; Paul Pietranico, CFA, Senior Vice President, Portfolio Manager, and Director of Research, Allianz Global Investors Solutions; and Laurence B. Siegel, Research Director, Research Foundation of CFA Institute Moderated by Robert Powell Type questions in dialog box on right hand side of screen

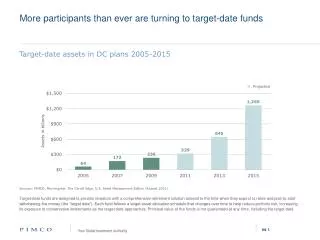

About this webinar TOPIC OUTLINE I. The seemingly precise “efficient frontier” is actually a cloud II. Evidence from, and application to, target date funds III. Consequences for investment strategy, financial planning, and spending SUMMARY • In this webinar, the authors suggest that target-date funds as an optimization solution are a “cloud,” so that precision in the desired asset mix and in its variation over time is only an illusion. • They discuss how the illusion of precision in target-date glidepaths and the implications for investors are well known within the quantitative practitioner community, but not in the wider community of retirement income professionals. • “Given the vast sums of retirement savings on autopilot in target-date glidepaths, making target date glidepaths reliably successful in practice requires full knowledge of their limits, in both theory and practice,“ according to Sexauer, Pietranico, and Siegel. “Armed with this knowledge, we think plan sponsors and investors can make better-informed lifetime savings and investment decisions.”

Efficient Frontier of Major Asset Classes Portrayed as a Cloud

Optimal asset mixes by participant age, with variation in savings rate

Optimal asset mixes by participant age, with joint variations of savings rate and risky asset volatility

Target-date glidepaths • Target date glidepaths are created using optimization methods • Optimization methods use objective function and need input data • Optimization inputs themselves are statistical estimates, not precise measures: Expected returns Required income in retirement Risk or volatility estimates Assumed savings rates Assumed future income growth Mortality rates

The use of statistical estimates • All inputs are subject to measurement error. • A point estimate must be entered, but there are many equivalent point estimates • Any optimization output is therefore a “cloud” or a “fuzzy frontier,” not a single line

Three logical consequences • For investors who use the default option, prudential principle calls for application of experience and judgment in choosing glidepaththat is biased towards the lower edge of the optimal glidepath cloud in terms of risk level • Investors would benefit from target date providers using public benchmark that also is at lower edge of glidepath cloud • Benchmark offers plan sponsors and investors clear insight into performance and risk exposures of the target date fund • Using target date fund based on glidepathat lower edge of cloud allows participants to make informed choice to default into the prudentially proper lower edge of the cloud, or • to make a potentially utility-enhancing decision to add risk, or • to take away risk by adding cash or selecting a lower risk fund • But starting point for any decision should be the theoretically sound low-risk default choice • Making target date glidepathsserve the customer requires full knowledge of limits of optimization, in both theory and practice