Download

1 / 19

190 likes | 789 Views

Marketing Analysts, LLC. Variable Selection in R. Fun with carets, elasticnets, and the Reverend Thomas Bayes … . Charles Ellis, MAi Research Mitchell Killian, Ipsos Marketing. Why do Variable Selection?. "Pluralitas non est ponenda sine neccesitate"

E N D

Marketing Analysts, LLC Variable Selection in R Fun with carets, elasticnets, and the Reverend Thomas Bayes … Charles Ellis, MAi Research Mitchell Killian, Ipsos Marketing

Why do Variable Selection? "Pluralitas non est ponenda sine neccesitate" • Overcoming the “Curse of Dimensionality” and developing more efficient data mining activities • Identifying relevant features & discarding those that are not • Enhancing the performance of data mining algorithms • Better prediction/classification • This applies to almost all fields, but especially those that are “data rich and theory poor” (e.g., Marketing)

Options for Tackling the Problem • Many different approaches have been suggested … it is a growing field, and many of them are implemented in R code. • BMA • rfe • glmnet • stepPlr • subselect • varselectRF • WilcoxCV • clustvarsel • Party • Boruta • PenalizedSVM • spikeslab • glmulti • BMS

Options for Tackling the Problem • Today we focus on three approaches, which range in degree of complexity and applicability. • Recursive Feature Elimination (package: caret [Kuhn]) • Bayesian Model Averaging (package: bma [Raftery et al.]) • Penalized regression (package: glmnet [Friedman et al.])

Recursive Feature Elimination(with resampling) • Implemented in the package caret • The basic idea (from Kuhn, 2009) • For each resampling unit (default is 10-fold cross-validation) do the following: • Partition the data into training & test sets • Train the model on the training set using all predictors • Predict outcomes using the test data • Calculate variable importance for all predictors

Recursive Feature Elimination (cont’d)(with resampling) • For each subset size (Si)to be considered keep the Si most important variables • Train the model on the training set using the Si predictors • Predict outcomes using the test data [Optional] Recalculate the rankings for each predictor • Calculate the performance profile over the Si predictors using the held-back samples • Determine the appropriate number of predictors • Fit the final model based on the optimal Si using the original training set

Recursive Feature Elimination An Example • Data set up (same across all examples) • Hot Breakfast Cereal Category • N = 310 consumers • Outcome Variable – Overall Liking • 5 point scale • Predictors – 31 Agree-Disagree statements measuring attitudes toward package and its components • 5 point scale • Outcome and predictors are treated as continuous (although they need not be)

Recursive Feature Elimination • The top 5 variables are: q4b_2, q4b_28, q4b_21, q4b_24, q4b_9 Results:

Recursive Feature Elimination Results (cont’d):

Recursive Feature Elimination Results (cont’d):

Bayesian Model Averaging • Implemented in the package BMA (also BMS) • The basic idea (from Hoeting et al., 1999) • All models are wrong, some are useful (Box, 1987) • Approach is to average over model uncertainty • Average over the posterior distribution of any statistic (e.g., parameter estimates) • Can be problematic for models with a large number of potential predictors • For “r” predictors, the set of potential models is 2r • Occam’s Window – Average over the subset of models that are supported by the data

Bayesian Model Averaging Note the similarity in the predictors chosen across the 5 best models (compared to the rfe algorithm) Results:

Bayesian Model Averaging Results (cont’d):

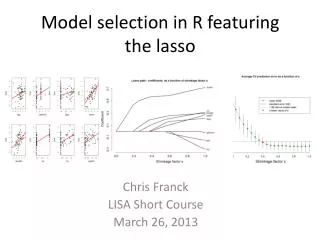

Penalized Regression • Implemented in the package glmnet • glmnet is an extension/application of the elasticnet package (Zou & Hastie, 2008) • The basic idea (from Friedman et al., 2010) • Ridge regression – applies an adjustment (the “ridge”) to the coefficient estimates, allowing them to borrow from each other, and shrinks the coefficients values. • However, Ridge aggressively shrinks coefficients to be equal to each other, allowing for no meaningful interpretation • Additionally, there is no easy way to determine how to set the penalization parameter

Penalized Regression (cont’d) • Lasso regression also adjusts the coefficients but tends to be “somewhat indifferent to very correlated predictors” • Essentially turns coefficients on/off, elevating one variable over another • Elastic Net – a compromise between Ridge and Lasso • Averages the effects of highly correlated predictors to create a “weighted” contribution of each variable • Lambda, a ridge regression penalty, shrinks coefficients toward each other • Alpha influences the number of non-zero coefficients in the model. • Alpha=0 is Ridge Regression and Alpha=1 is Lasso

Penalized Regression (cont’d) Alpha=0 Alpha=1 Alpha=0.2 At each step there is a unique value of lambda

Penalized Regression α= 0.75 α= 0.10 Results: The impact of different parameterizations of alpha

Penalized Regression Again, notice the similarity wrt predictors chosen with the other two algorithms Results: