Download

1 / 12

120 likes | 267 Views

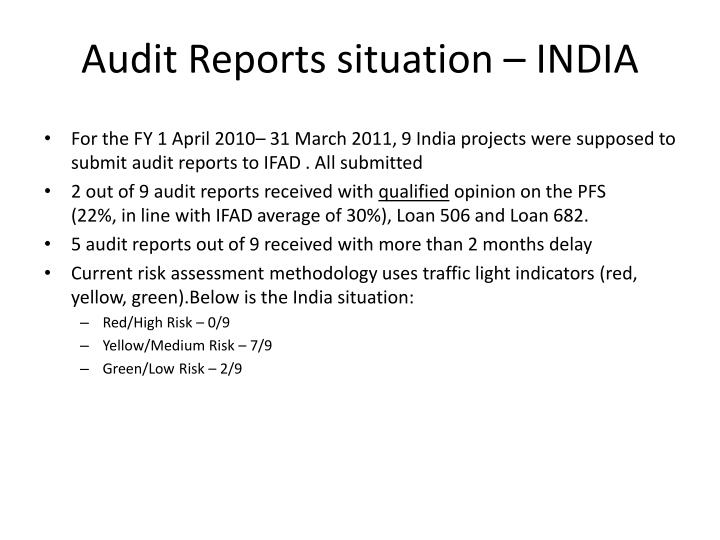

Audit Reports situation – INDIA. For the FY 1 April 2010– 31 March 2011, 9 India projects were supposed to submit audit reports to IFAD . All submitted 2 out of 9 audit reports received with qualified opinion on the PFS (22%, in line with IFAD average of 30%), Loan 506 and Loan 682.

E N D

Audit Reports situation – INDIA • For the FY 1 April 2010– 31 March 2011, 9 India projects were supposed to submit audit reports to IFAD . All submitted • 2 out of 9 audit reports received with qualified opinion on the PFS (22%, in line with IFAD average of 30%), Loan 506 and Loan 682. • 5 audit reports out of 9 received with more than 2 months delay • Current risk assessment methodology uses traffic light indicators (red, yellow, green).Below is the India situation: • Red/High Risk – 0/9 • Yellow/Medium Risk – 7/9 • Green/Low Risk – 2/9

Most common internal control issues identified by auditors 1 - Accounting area (Accounting methodology used is not consistent, Accounts are kept manually, the accounting system allows recording of back-dated accounting entries without proper authorization, no regular bank reconciliations) – Risk of errors and mis-representation of the financial position of the project 2 – Fixed Assets management (Asset registers not maintained properly) - risk of loss/misuse of assets 3 – Unused Funds(2 Projects have a huge balance of unused funds) - risk of mismanagement of funds with consequences on project's implementation; In general projects should avoid having material cash availability and link request of funds to disbursements needs 4 – Communications with CAAA (As all the SAs are held at ministry level, there are reconciliation issues between projects, CAAA and IFAD)

Completeness of financial statements and quality of the audit work COMPLETENESS OF FINANCIAL STATEMENTS • The projects which submitted a complete set of financial statements are Loan 779, Loan 194, Loan 585 and Loan 682. • Other projects submitted an incomplete set of financial statements to IFAD ; none of them provided a comparison between actual expenditures and budget estimates, 3 did not submit a WA schedule/SOEs and a cumulative status of funds by category QUALITY OF THE AUDIT WORK • In many cases, the assessment of the audit work is mostly satisfactory • In 3 cases the audit work is satisfactory (Loan 682 , 779 and 784)