Download

1 / 14

140 likes | 148 Views

This symposium explores the role of private labels in competition between retailers and suppliers, discussing their impact on brand growth, competition policy, and the changing focus of competition.

E N D

Trends in Retail Competition: Private Labels, Brands and Competition Policy A Symposium on the Role of Private Labels in Competition between Retailers and between Suppliers The Institute of European and Comparative Law in conjunction with the Centre for Competition Law and Policy Oxford, 9 June 2005 Sponsored by Bristows CCLP (S) 04/05 (III)

Private Label Their Role for Retailers & Their Impact Upon Competition Part II

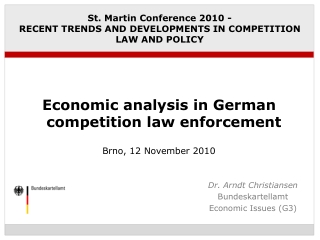

Source of Own Label Growth - UK 100% 90% 31.8 34.2 80% Brand Leader 70% 13.7 No 2Brand 60% 15.3 50% Brands over 2% 15.6 19.4 40% Brands under 2% 8.8 30% Own Label 14.7 20% 30.0 10% 16.4 0% 1975 1997

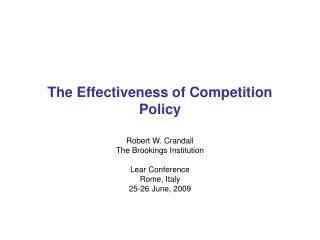

100% 90% 22 26 26 27 29 30 30 31 32 35 40 80% 47 48 15 70% 13 14 12 5 9 12 7 12 5 60% 2 11 10 11 17 9 12 15 15 9 14 11 2 3 2 50% 3 2 2 3 1 8 7 2 2 3 11 3 8 11 12 10 3 4 15 40% 14 11 12 11 11 5 4 6 7 6 6 6 30% 8 6 10 9 9 10 20% 35 35 33 32 31 31 30 26 25 23 23 23 22 10% 0% 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 MTD Private Label Other Brands KP Sooner Golden Wonder Smiths Walkers Share of UK Crisp Market

Changing the Focus of Competition • From Relevance based on • Consumer Research • Product Development • Perceived Value • To Price

Category Management For a Retailer it is the means for determining pricing, merchandising, promotions and product mix based on category goals, the competitive environment, and consumer behaviour Centre for Retail Management Northwestern University (1993)

Category Management:The Annual Plan • Retail Complexity • Thousands of SKU’s • Hundreds of Categories • Frequent Promotions – Price Change & Gondola Ends • Numerous New Product Introductions:Recipe change, Pack Size, New Brands • Branded Suppliers Submit Advance Plans of Promotions, Price Changes & New Line Introductions • Year End Rebates Linked to Planned Activities

Category Management:The Annual Plan • Retail Complexity • Thousands of SKU’s • Hundreds of Categories • Frequent Promotions – Price Change & Gondola Ends • Numerous New Product Introductions:Recipe change, Pack Size, New Brands • Branded Suppliers Submit Advance Plans of Promotions, Price Changes & New Line Introductions • Year End Rebates Linked to Planned Activities

The Retailer as A Double Agent • Agent For Their Own Label Products • Agent for Manufacturer Brands • Controls the Pricing, Listing, Space Allocation and Promotion of ALL Brands • Has Advance Notice of Planned Activities of Manufacturer Brands • Has a Margin Incentive to Promote Own Brands

Summary • UK grocery retailing is characterised by vertically integrated oligopolists • Control of the supply chain has facilitated the expansion of private label • Private label facilitates differentiation and higher retail margins • Retailers act as agents for their products and their suppliers brands • Retailers control all of the in-store marketing variables and have advance notice of the brand plans of their suppliers • Most product innovation is initiated by producer brands

Retail Integration “CONNECTIVITY” The linking of hitherto individual processes of distribution (customer dialogue; merchandising; shelf replenishment;inventory control; depot management and delivery;procurement; buying; supplier operations) by information technology to provide total transparencyand instant communication, thereby reversing the Supply Chain. From Producer Push to Consumer Pull

Category Management What is it? • Partnership with Suppliers? • Managing the In-Store Marketing levers? • Space • Promotion • Range • Price • Part of efficient consumer response? • Measured performance? • A new business process?