Download

1 / 16

160 likes | 271 Views

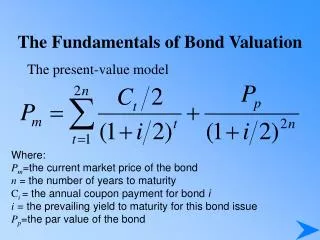

The 5% Problem Double Jeopardy for Traditional Bond Investors. Nicholas Millikan , CAIA Investment Specialist. Why Reconsider Your Income Strategy: The 5% Problem. The bull market in bonds may be winding down Higher interest rates may be accompanied by excessive risk

E N D

The 5% ProblemDouble Jeopardy for Traditional Bond Investors Nicholas Millikan, CAIA Investment Specialist

Why Reconsider Your Income Strategy: The 5% Problem • The bull market in bonds may be winding down • Higher interest rates may be accompanied by excessive risk • Rates cannot go much lower • Flows to bond funds have reached unprecedented levels • Alternative sources of yield are looking more attractive

A Bond Bull Market for More than Three Decades Source: Ibbotson Associates Bonds = Ibbotson Associates SBBI U.S. Intermediate-Term Government Bond Index Past performance does not guarantee future results.

Investors Have Gravitated to Bonds Despite Falling Yields Source: Investment Company Institute, 12/31/12

Real Treasury Yields Have Dipped Below Zero Source: Ibbotson Associates, 01/31/13 Past performance does not guarantee future results.

Headlines on Unsettled Bond Markets Fixed Income: Out of the Frying Pan, Into the Fire Yahoo! Finance, April 9, 2013 Billionaire Wilbur Ross: Long Term Bonds Are a ‘Huge Risk’ CNBC, March 22, 2013 Beyond the Bond: Three Alternative Income Strategies as Price Risk Looms Minyanville, April 9, 2013 How to rate-proof your fixed income strategy Citywire Wealth Manager, April 9, 2013 Fixed Income: Fewer Places To Hide Seeking Alpha, March 15, 2013

Risks from Higher Interest Rates May Exceed Potential for Reward Note: Assumes 39.6% Federal and 3.8% Affordable Care Act tax rate; does not include state/local taxes. Sources: Asset classes in the chart above are represented by the following indexes: Muni High-Yield—Barclays High-Yield Municipal Bond Index; U.S. Corp High-Yield—Barclays U.S Corporate High-Yield Index; Municipal Bond—Barclays Municipal Bond Index; U.S. Mortgage-Backed Securities—Barclays U.S. Mortgage Backed Securities Index; U.S. Credit—Barclays U.S. Credit Index; U.S. Treasury—Barclays U.S. Treasury Index.Past performance does not guarantee future results.

Diminished Return Spreads Point to a Bond Market Shift Source: Ibbotson Associates, 12/31/12 Stocks = S&P 500 Index, Bonds = Ibbotson Associates SBBI U.S. Intermediate-Term Government Bond Index Past performance does not guarantee future results.

Dividend Stocks: An Important Source for Yield S&P 500 Earnings Yield – 10 Yr Treasury Yield 12/31/69 – 12/31/12 S&P 500 Dividend Yield – 10 Yr Treasury Yield Adjusted for Inflation 12/31/69 – 12/31/12 Source: Bloomberg Past performance does not guarantee future results.

Public Debt and Yields Tightly Correlated Source: U.S. Treasury, Ibbotson Associates, 12/31/12 Past performance does not guarantee future results.

Bond Macro Market Outlook Shift in 10-year Treasury relative performance of stocks and bonds1 Extreme optimism in the form of historically high bond fund inflows2 Negative real yields on the 10-year Treasury3 Stabilizing housing prices4 Improving employment5 Slowing of personal, government and corporate deleveraging6 Historically high earnings and dividend yield relative to the 10-year Treasury7 1. Source: Ibbotson Associates, 12/31/12 2. Source: Investment Company Institute, 12/31/12 3. Source: Ibbotson Associates, 12/31/12 4. Source: Bloomberg, 12/31/12 5. Source: Bureau of Labor Statistics, 12/31/12 6. Source: U.S. Treasury, Ibbotson Associates, 12/31/12 7. Source: Ibbotson Associates, 12/31/12

Reasons to Cast a Wider Net for Income • With yields near record lows, traditional bond strategies are failing to meet investor needs. • Long-only bond portfolios are vulnerable to rising interest rates and inflation. • Only time will tell if the bond bull market is truly over. • A diversified approach to investment income makes sense in any market climate. • Investors need dynamic asset allocation that is responsive to global trends.

A Diversified Income Portfolio Did Well in Historical Testing Historical Asset Class Performance During the 1941-81 Bond Bear Market January 1, 1941—December 31, 1981 1. Based on Ibbotson Time Series 2. Based on S&P 500 Index 3. Based on Ibbotson Time Series for Japanese long-term government bonds 4. Adjusted for 4.7% inflation 5. Ibbotson Associates SBBI U.S. Intermediate-Term Government Bond Index Source: Ibbotson. Associates, as of 12/31/12. Past performance does not guarantee future results.

Rethinking an Income Allocation Strategy Shifting some assets from Treasuries to a flexible, tactical approach means investing across a variety of sectors, securities, and strategies: • Municipal bonds • Corporate and high yield bonds • Dividend stocks • Global stocks and bonds • REITs • Active risk management with ability to sell short Treasuries and short-term bonds can still be part of a diversified strategy. They offer: • Capital preservation • Income stability • Consistency of payments • Possible tax benefits

Discover More About the 5% Problem • Investors have been conditioned to believe that traditional bonds are safe and can deliver 5% annualized yields over the long term. • In the current climate, neither may be true. • To learn more, download out new white paper, The 5% Problem: Double Jeopardy for Bond Investors, at www.forwardinvesting.com or call us at (888) 312-4100.

Important Information You should consider the investment objectives, risks, charges and expenses of the Forward Funds carefully before investing. A prospectus with this and other information may be obtained by calling (800) 999-6809 or by downloading one from www.forwardinvesting.com. It should be read carefully before investing. RISKS There are risks involved with investing, including loss of principal. Past performance does not guarantee future results, share prices will fluctuate and you may have a gain or loss when you redeem shares. • Alternative strategies typically are subject to increased risk and loss of principal. Consequently, investments such as mutual funds which focus on alternative strategies are not suitable for all investors. Diversification and asset allocation do not assure profit or protect against risk. There is no guarantee the companies in our portfolio will continue to pay dividends. Nathan Rowader is a registered representatives of ALPS Distributors, Inc. Forward Funds are distributed by Forward Securities, LLC. Not FDIC Insured | No Bank Guarantee | May Lose Value FWD004599 013114