Download

1 / 8

80 likes | 312 Views

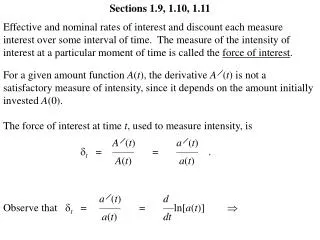

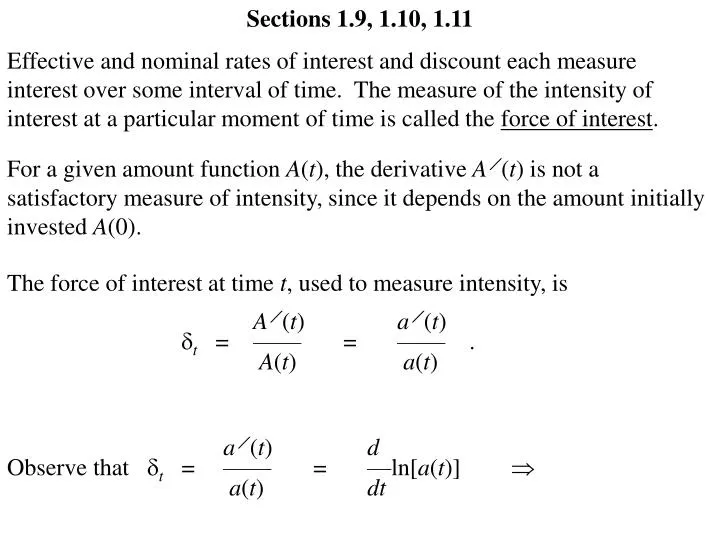

Sections 1.9, 1.10, 1.11. Effective and nominal rates of interest and discount each measure interest over some interval of time. The measure of the intensity of interest at a particular moment of time is called the force of interest .

E N D

Sections 1.9, 1.10, 1.11 Effective and nominal rates of interest and discount each measure interest over some interval of time. The measure of the intensity of interest at a particular moment of time is called the force of interest. For a given amount function A(t), the derivative A (t) is not a satisfactory measure of intensity, since it depends on the amount initially invested A(0). The force of interest at time t, used to measure intensity, is A (t) a (t) t = —— = —— . A(t) a(t) a (t) d Observe that t = —— = —ln[a(t)] a(t) dt

t t t d —ln[a(r)] dr= dr ln[a(t)] – 0 r dr = ln[a(r)] = 0 0 0 t r dr a(t) = e 0 An analogous definition to measure force of discount would be d — dt d — dt d — dt [a(t)]–1 [a(t)]–2 [a(t)] [a(t)] – – = = [a(t)]–1 [a(t)]–1 [a(t)] = –t , which is the negative of the force of interest. Consequently, we do not need a separate measure for the force of discount.

Find the force of interest with compound interest, that is, with an accumulation function a(t) = (1 + i)t , a (t) t = —— = a(t) (1 + i)t ln(1 + i) ——————— = (1 + i)t ln(1 + i) = We see that with compound interest, the force of interest is constant. With compound discount, the force of interest must also be constant. In general, if the force of interest is constant over an interval of time, then the effective rate of interest will also be constant over that interval. That is (with n a positive integer), if t = for 0 t n, then t r dr a(t) = e = 0 et a(1) = e = 1 + i a(t) = (1 + i)t , which is the accumulation function for compound interest, where effective rate of interest is constant.

We may now write –p m i(m) 1 + — = m d(p) 1 –— = e . p 1 + i = v–1 = (1 –d)–1 = Using Maclaurin series expansions, we can write the following: 2 3 4 i = e– 1 = + — + — + — + … 2! 3! 4! A similar expansion is possible for i(m), for d, and for d(m). (See page 33.) We can then show i(m) and d(m) each as m. i2i3i4 = ln(1 + i) = i – — + — – — + … 2 3 4

Using Maclaurin series expansions, we can write the following: 2 3 4 i = e– 1 = + — + — + — + … 2! 3! 4! A similar expansion is possible for i(m), for d, and for d(m). (See page 33.) We can then show i(m) and d(m) each as m. i2i3i4 = ln(1 + i) = i – — + — – — + … 2 3 4 Observe that i(m) = m[(1 + i)1/m 1] = m[e/m 1] = (/m)2 (/m)3(/m)4 m/m + —— + —— + —— + … = 2! 3! 4! 2 3 4 + —— + —— + —— + … 2! m 3! m2 4! m3 It should be obvious that the limit as m is .

Suppose $2000 is invested at a rate of compound interest of 9% per annum. (a) Find the accumulation function. (b) Find the force of interest. (c) Find the value of the investment after 3 years. a(t) = (1 + 0.09)t = ln(1 + 0.09) 0.08618 2000(1 + 0.09)3 = $2590.06 Suppose $2000 is invested with a constant force of interest equal to 9% per annum. (a) Find the accumulation function. (b) Find the effective rate of compound interest. (c) Find the value of the investment after 3 years. a(t) = e0.09t i = e0.09– 1 = 0.09417 2000e(0.09)(3)= $2619.93 Note: an accumulation function of the form a(t) = et is often considered as representing a rate of compound interest of compounded continuously.

Find the force of interest with simple interest, that is, with an accumulation function a(t) = 1 + it . Find the force of interest with simple discount, that is, with an accumulation function a(t) = (1 –dt)–1for 0 t< 1/d . a (t) t = —— = a(t) i —— 1 + it a (t) t = —— = a(t) – (1 –dt)–2 (–d) ——————– = (1 –dt)–1 d ——— for 0 t< 1/d (1 –dt) Find the accumulated value of $200 invested for 5 years if the force of interest is t = 1 / (8 + t). 5 5 (8 + t)–1 dt ln(8 + t) a(5) = e = e = 13/8 0 0 This is the force of interest function for simple interest with i = A(5) = 200(13/8) = $325 0.1250.

Find the accumulated value of $500 invested for 9 years if the rate of interest is 5% for the first 3 years, 5.5% for the second 3 years, and 6.25% for the third 3 years. 500(1 + 0.05)3(1 + 0.055)3(1 + 0.0625)3 = $815.23 Table 1.1 on page 38 summarizes much of the material in Chapter 1.