Download

1 / 9

90 likes | 107 Views

Explore the reasons why inflation is a concern for policy makers and how it impacts individuals and the economy. Discover the costs of inflation, such as shoe-leather costs and menu costs, and the degradation of the unit-of-account role of money. Learn about the winners and losers of inflation, including the impact on loans and interest rates.

E N D

Inflation: An Overview Why is inflation something to worry about? Why do policy makers even now get anxious when they see the inflation rate move upward?

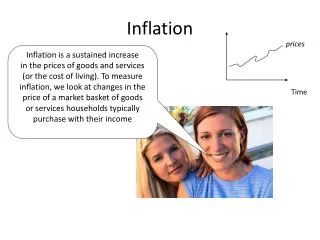

THE LEVEL OF PRICES DOESN’T MATTER • The most common complaint about inflation is that it makes everyone poorer because of higher prices. But that is not true. • Real wage • The wage rate divided by the price level • Real income • Is income divided by the price level • The level of prices does not matter but the inflation rate does matter.

Rate of Price Change does Matter It is crucial to distinguish between the level of prices and the inflation rate. • Inflation rate • Price level in year 2- Price level in year 1divided by price level in year 1 X 100 • Economists believe that high rates of inflation impose significant economic costs.

Shoe- leather costs • Are the increased costs of transactions caused by inflation. • People hold money for transactions but a high inflation rate discourages people from holding on to money because the purchasing power of the cash erodes as the overall level of prices rise. • People look for ways to reduce the amount of money they hold often at considerable economic cost. • (wear and tear caused by the extra running around that takes place when people are trying to avoid holding money.)

Menu Costs • In a modern economy, most of the things we buy have a listed price. Changing a listed price has a real cost (menu costs) • In times of high inflation rates, menu costs can be substantial (Brazil/Israel) • Menu costs are also present in low-inflation economies, but they are not severe. In this case businesses might update their prices only sporadically • Technological advances are leading to menu costs being less important, since prices can be changed electronically and fewer workers are needed.

Unit-of –Account Costs • We state contracts in monetary terms • Renter owes so much money a month • Company that issues a bond promises to pay the bondholder the dollar value of the bond when it comes due • We make our economic calculations in dollars: • Family budget • Small business owner trying to figure out how his or her business is doing (money in money out) • Role of the dollar as a basis for contracts and calculation is called unit-of –accounts role of money and it is an important part of the economy.

Inflation can degrade the unit –of-account role of money • Causes the purchasing power of the dollar to change over time, dollar next year is worth less than a dollar this year. • The effect is to reduce the quality of economic decisions: the economy as a whole makes less efficient use of its resources because of the uncertainty caused by changes in the unite of account, the dollar. • Unit-of-account costs of inflation are the costs arising from the way inflation makes money a less reliable unit of measurement. • Real important in the tax system • Inflation can distort the measures of income on which taxes are collected (capital gains) (phantom gain) • Less investment spending Phantom gains

Winners and Losers from Inflation • The main reason inflation sometimes helps some people while hurting others is that economic transactions ,loans,often involve contracts that extent over a period of time and they are normally specified in normal, that is, in dollars terms. • Think of a loan • What that dollar repayment is worth in real terms that is purchasing power depends a lot on the rate of inflation of the years of a loan.

The interest rate on a loan is the percentage of the loan amount that the borrower must pay the lender, annual, in addition to the loan amount. • Economists summarize the effect of inflation on borrowers and lenders by distinguishing between nominal and real interest rates. • Nominal interest rates • Is the interest rate that is actually paid for a loan, unadjusted for the effects of inflation. • Real interest rates • Nominal interest rate adjusted for inflation. That is done by subtracting the inflation rate from the nominal interest rate (8% nominal and inflation is 5% the real interest rate 8%-5%= 3%) • How does this all make winners and losers?