Download

1 / 19

190 likes | 255 Views

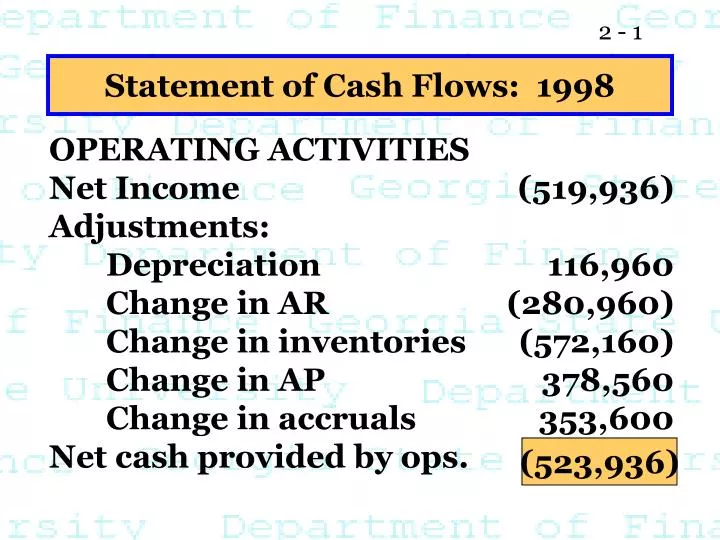

Statement of Cash Flows: 1998. OPERATING ACTIVITIES Net Income (519,936) Adjustments: Depreciation 116,960 Change in AR (280,960) Change in inventories (572,160) Change in AP 378,560 Change in accruals 353,600 Net cash provided by ops. . (523,936).

E N D

Statement of Cash Flows: 1998 OPERATING ACTIVITIES Net Income (519,936) Adjustments: Depreciation 116,960 Change in AR (280,960) Change in inventories (572,160) Change in AP 378,560 Change in accruals 353,600 Net cash provided by ops. (523,936)

L-T INVESTING ACTIVITIES Investments in fixed assets (711,950) FINANCING ACTIVITIES Change in s-t investments 48,600 Change in notes payable 520,000 Change in long-term debt 676,568 Payment of cash dividends (11,000) Net cash from financing 1,234,168 Sum: net change in cash (1,718) Plus: cash at beginning of year 9,000 Cash at end of year 7,282

Analysis of Statement of Cash Flows • What were the major sources and uses of cash? • What % of inflows and outflows came from the three areas? • What lifecycle stage is the firm in? • Is cash being created internally or externally? • Is the pattern typical (and sustainable), or not?

What can you conclude about the company’s financial condition from its statement of cash flows? • Net cash from operations = -$523,936, mainly because of negative net income. • The firm borrowed $1,185,568 and sold $48,600 in short-term investments to meet its cash requirements. • Even after borrowing, the cash account fell by $1,718.

NOTES • Balance Sheet is “Stock” (as of) • Other Statements are “Flow” (through time) • When analyzing, keep “unusual events” in mind”

1997 Tax Year Single IndividualTax Rates Taxable Income Tax on Base Rate* 0 - 24,650 0 15% 3,697.50 24,650 - 59,750 28% 59,750 - 124,650 13,525.50 31% 124,650 - 271,050 33,644.50 36% Over 271,050 86,3480.50 39.6% *Plus this percentage on the amount over the bracket base.

Assume your salary is $45,000, and you received $3,000 in dividends.You are single, so your personal exemption is $2,650 and your itemized deductions are $4,550. On the basis of the information above and the 1997 tax year tax rate schedule, what is your tax liability?

Calculation of Taxable Income Salary $45,000 Dividends 3,000 Personal exemptions (2,650) Deductions (4,550) Taxable Income $40,800

$40,800 - $24,650 • Tax Liability: TL = $3,697.50 + 0.28($16,150) = $8,219.50. • Marginal Tax Rate = 28%. • Average Tax Rate: Tax rate = = 20.15%. $8,219.5 $40,800

1997 Corporate Tax Rates Taxable Income Tax on Base Rate* 0 - 50,000 0 15% 50,000 - 75,000 7,500 25% 75,000 - 100,000 13,750 34% 100,000 - 335,000 22,250 39% ... ... ... Over 18.3M 6.4M 35% *Plus this percentage on the amount over the bracket base.

Assume a corporation has $100,000 of taxable income from operations, $5,000 of interest income, and $10,000 of dividend income. What is its tax liability?

Operating income $100,000 Interest income 5,000 Taxable dividend income 3,000* Taxable income $108,000 Tax = $22,250 + 0.39 ($8,000) = $25,370. *Dividends - Exclusion = $10,000 - 0.7($10,000) = $3,000.

Taxable versus Tax Exempt Bonds State and local government bonds (municipals, or “munis”) are generally exempt from federal taxes.

Exxon bonds at 10% versus California muni bonds at 7%. • T = Tax rate = 28%. • After-tax interest income: Exxon = 0.10($5,000) - 0.10($5,000)(0.28) = 0.10($5,000)(0.72) = $360. CAL = 0.07($5,000) - 0 = $350.

At what tax rate would you be indifferent between the muni and the corporate bonds? Solve for T in this equation: Muni yield = Corp Yield(1-T) 7.00% = 10.0%(1-T) T = 30.0%.

Implications • If T > 30%, buy tax exempt munis. • If T < 30%, buy corporate bonds. • Only high income, and hence high tax bracket, individuals should buy munis.

General Concepts (Taxes) • Only Marginal Tax Rates Matter (not average rates) • After tax return matters, not pre-tax • After tax return = Pre-tax return x (1 - marginal effective tax rate)

Got questions?Get answers!! • Voicemail: • Email: (404) 651-2691 chodges@gsu.edu • Electronic Bulletin Board: http://www-cba.gsu.edu/ ~wwwfin/finconf/finba862/finba862.html