Download

1 / 29

290 likes | 429 Views

Incentive regulation of prices when costs are sunk. Lewis T. Evans and Graeme Guthrie Presentation by Collin Philipps. Suppose….

E N D

Incentive regulation of prices when costs are sunk Lewis T. Evans and Graeme GuthriePresentation by Collin Philipps

Suppose… • Evans and Guthrie propose a model where capital investment is irreversible. Future demand is uncertain, but the firm must choose an amount of capital based on its expectations. Here there is a risk that the firm will over-invest, but there is also a drawback if the firm has insufficient capital.

Suppose that the firm’s expected number of customers, x, changes over time according to: • Here, Xi represents a stochastic process. • The firm provides a service connection to these customers.

Suppose also that the cost of new connections follows a random process: • Where Sigma is related to Xi by

How does the firm respond to changes in the marketplace?If the number of customers demanding a connection exceeds the capacity of the network, the firm will immediately invest in expanding its network. If the number of customers falls, the network capacity does not decline.

What does this mean for regulation? • If the regulator wishes to set an acceptable amount of revenue for the firm, it must determine the cost structure. How does the regulator measure the firm’s cost?

If the firm has excess capacity, It is still cheaper for the firm to operate its existing network than to replace it with one that is smaller and “optimally configured”.

The firm knows that it will have to invest more in capital than the ‘efficient’ quantity.If it costs cz to build a network that serves all the present customers, the firm must be allowed to collect revenue greater than (not merely equal to) cz or it will not build the network.

The firm’s allowed revenue must therefore be equal to the costs of a hypothetical replacement firm.This revenue is a function of present demand, not of capacity.

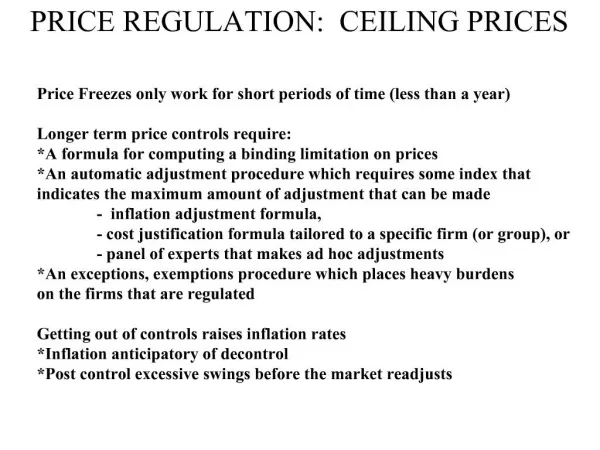

Prices! • If the regulator sets the price for the firm’s product:Regulation could be reasonable if the firm can collect revenue as a function of capital prices continuously over time, where the price moves in the same direction as capital costs.This is not realistic.

More realistically, we suppose that the regulator sets fixed prices and holds them constant until capital costs change sufficiently to justify price revisions.When this occurs, we assume that the regulator sets a price to ensure that the present value of all future revenue is equal to the costs of a hypothetical replacement firm.

In theory, incentive regulation should protect customers from demand shocks.That is to say that, if the number of customers declines, the price should not increase on the remaining customers to maintain revenue.This can cause losses to the firm.

There are four special cases. • If the price changes continuously, regulation is reasonable. (the firm collects revenue equal to the costs of a hypothetical replacement firm)

A second special case: Prices are fixed indefinitely. • In this case, there is a single solution for the reasonable price.

If regulated prices can be adjusted upwards, but not downwards, then a low price is reasonable if it will be adjusted upwards in the future. • If regulated prices are adjusted downwards, but never upwards, then a high price is reasonable if it will be adjusted downwards.

Higher expected demand leads to lower regulated prices.Higher demand growth raises the present value of the firm’s revenue stream, reduces the risk of investment in new capacity, and also leads to lower prices. The risk of demand shocks is greater when revision intervals are longer, though the risk of capital price shocks is decreased.

When the network has very little excess capacity, demand shocks affect revenues and expectations about future investment expenditures.These two effects offset one another. • When the network has large excess capacity, demand shocks will affect revenue more dramatically than expected future investment expenditures.

Conclusions • When a firm is modeled over time with uncertainty about demand and capital costs, output prices can be derived in order to fulfill the requirements of incentive regulation. • Unlike rate of return regulation, customers will not be exposed to risks from demand shocks. In the long run, they could feel effects of capital price fluctuations.

Conclusions • However, the owners of the firm bear the risk of both demand shocks and capital price fluctuations. • The frequency of price revisions affects the firm’s optimal pricing by affecting its risk. • The market value of the regulated firm exceeds the replacement cost of its assets. The difference can be attributed to the value of its excess capacity.