Download

1 / 17

170 likes | 309 Views

"Lessons from the 2013 Public Debt and Growth Debate: How to Assess Economic Sustainability". Thomas Herndon, Doctoral Candidate University of Massachusetts Amherst, Department of Economics and Political Economy Research Institute 9-23-2014. Outline.

E N D

"Lessons from the 2013 Public Debt and Growth Debate: How to Assess Economic Sustainability" Thomas Herndon, Doctoral Candidate University of Massachusetts Amherst, Department of Economics and Political Economy Research Institute 9-23-2014

Outline • 2013 Reinhart-Rogoff/HAP Public Debt and Growth Debate • Problems Identified in literature • Problems with Causality: Debt -> Growth? • Endogeneity • Panizza and Presbitero • Problems with estimating debt thresholds • Endogeneity • Kourtellos, Stengos, Tan • Heterogeneity • Eberhardt and Presbitero

Problems with Causality • Does high debt cause slow growth, or is it reverse causality? • Early review of Literature – Panizza and Presbitero (2013) • “While many papers have found a negative correlation between debt and growth, our reading of the empirical literature is that theres is no paper that can make a strong case for a causal relationship going from debt to economic growth.” • Dube (2013) Comment

Problems with Estimating Debt Threshold Identified by the Literature • Endogeneity • Most papers use a PSTR model based on either Hansen (1999) or Hansen and Caner (2005), however these rely on an exogenous threshold variable. • Kourtellos, Stengos and Tan (2012) – “One difficulty with the above studies is that they ignore the problem of endogeneityin the threshold variable. This is important because, as Kourtellos, Stengos, and Tan (2011) argue, if the threshold variable is endogenous, the above approaches will yield inconsistent parameter estimates for the regime-specific partial effects.” • Heterogeneity • Eberhardt and Presbitero (2013) – Heterogeneity makes it difficult to determine whether threshold is within or across countries.

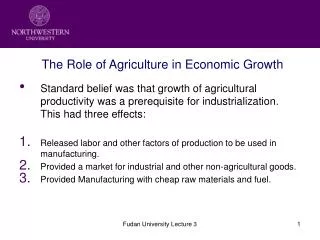

Checheritaand Rother (2010) replication with RR data. They fit a quadratic curve in their regression, and found an inverted U-shape. Below is a loess regression for five year future growth and debt/GDP, which replicates their finding.

But there’s a lot of heterogeneity, with many countries showing a positive relationship at high levels of debt. The inverted U-shape appears to be driven by the outlier of Ireland. (Note, RR dataset doesn’t include Luxembourg, while C-R does. )

More Recent Lit on Debt and Growth confirms our finding of lack of threshold. • Pescatori, Sandri, and Simon (2014) - Debt and Growth: Is There a Magic Threshold? • Lof and Malinen (2014) – Does Sovereign Debt Weaken Growth? A Panel VAR Analysis • Eberhardt (2013) - Nonlinearities in the Relationship between Debt and Growth: Evidence from Co-Summability Testing • Eberhardt and Presbitero (2013) - This Time They’re Different: Heterogeneity and Nonlinearity in the Relationship between Debt and Growth • Egert (2013) – The 90% Public Debt Threshold: The Rise and Fall of a Stylized Fact • Bell, Johnston and Jones (2013) - Stylised fact or situated messiness? The diverse effects of increasing debt on national economic growth

Bank of England: 300 Years of Public Debt and Interest Rates

Results of Austerity? De Grauwe and Ji (2013) Austerity and Increases in Debt/GDP 2011-2012 Austerity and GDP Growth 2011-2012 Source: Financial Times and Datastream. Note: The Greek debt ratio excludes the debt restructuring of end 2011 that amounted to about 30% of GDP.