Download

1 / 20

220 likes | 396 Views

Present Value and Bonds. A dollar today is worth more than a dollar tomorrow. Would you rather have $1 today or $1 in a year? Would you rather have $1,000 today or $1,000 in 20 years? What’s the difference?. A dollar today is worth more than a dollar tomorrow.

E N D

A dollar today is worth more than a dollar tomorrow. • Would you rather have $1 today or $1 in a year? • Would you rather have $1,000 today or $1,000 in 20 years? • What’s the difference?

A dollar today is worth more than a dollar tomorrow. • You might not need the money in the future. You may not be able to use it. • You want to buy something NOW! • Like a calculator for the next exam. • Like rent, food or medicine, so you don’t end up dead. • Like flowers for the girl who won’t wait for you any longer. • You might not get that money in the future. • The person who promised it to you could end up broke , gone or just decide to not pay you. • Prices could increase. • You could take that money now, invest it, and have more money in the future.

A dollar today is worth more than a dollar tomorrow How much is $1 in a year worth today? • Clearly it is less than $1. • If someone said they would give you $1000 in one year, how much is that worth today? • Would you pay $900? • Would you pay $950? • If someone said they would give you $1000 in 10 years, how much is that worth today? • Does it matter who is promising to pay you?

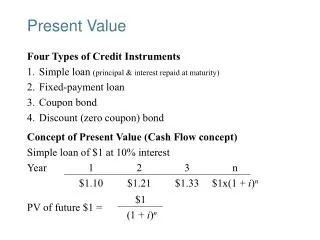

Bonds • A bond is a contract that promises to pay the bondholder a specific amount of money at one or more specific points in the future. • The simplest type of bond is a zero coupon bond. • A zero coupon bond is a promise to pay a specific amount (usually $1,000) on a specific date. • The two examples… “$1,000 in a year, $1,000 in 10 years”, are examples of zero coupon bonds. • The cost or price of a zero coupon bond is the same as the present value of the zero coupon bond.

Present Value • In the equation b = p (1+r)t, “b” tells us the future value of money invested or borrowed, while “p” tells us the current value of that money. • By isolating “p”, we have the present value equation. • Rearrange b = p (1+r)t by dividing both sides of the equation by (1+r) t • We now have p = b / [(1+r) t]. • This is the equation for present value. • In present value equations we use “C” for cash instead of “b” for balance. • p = C / [(1+r) t].

Price of Zero Coupon Bonds • The price of a zero coupon bond depends on the rate and the time to maturity. • Imagine that interest rates are 5%. • Our $1,000 in one year should cost… • P = $1,000 / (1+.05)1 • P =$952.38 • Our $1,000 in 10 years should cost • P = $1,000 / (1+.05)10 • P =$613.91

Pricing Zero Coupon Bonds • $1000/(1.00883)2.98 = $1000/1.0265 = $974.18 • $1000/(1.00527)2.72 = $1000/1.0144 = $985.80 • $1000/(1.02667)9.96 = $1000/1.2997 = $769.41 • $1000/(1.037)19.67 = $1000/2.043 = $489.48 • Bond quotes are listed as a percentage of the maturity value. • These are different than the quoted prices by very small amounts • I did not take leap years into consideration.

Coupon Bonds • The most common type of bond is a “coupon bond”. • A coupon bond not only pays the face value ($1,000 usually) at maturity but it also pays a specified $ amount on a regular basis. • Most bonds pay interest twice a year. • For example, a 4% coupon bond maturing in Jan 2013 will pay $1000 in January 2013, but it will also pay $20 twice a year until then. • $20 = ($1,000 x 4%/2 times per year) • So the owner of this bond would get $20 in Jan 2012, $20 in July 2012, and $1020 in Jan 2013. • The term “coupon” refers to paper coupons that, in the past, bondholders would submit to receive payment. • Everything is electronic now. • The term “coupon” still refers to the 4% rate and the semi-annual payment.

Pricing Coupon Bonds • If the yield is 6%, what is the value of an 8% coupon bond that matures in 5 years? • Assume annual coupon payments • Notice the coupon rate and yield are different. • Treat this bond as two separate cash flows. • Calculate the value of $1,000 in 5 years. • PV1 = C1/(1+r)t • PV1 = $1000 / (1.06)^5 = $747.38 • Calculate the value of the coupon payments over 5 years. • PV2 = [$80 / (1.06)^1] + [$80 / (1.06)^2] ….. + [$80 / (1.06)^5] • This is an alternate method PV2 = C2 [(1/r) – (1/[r(1+r)t])] PV2 = $336.99 • The value of the bond is $747.38 + $336.99 = $1084.37

Treasury Bills, Notes and Bonds • The world’s largest issuer of bonds, and biggest borrower, is the United States Federal Government. • Treasury Bills … • Mature in less than one year after issuance • Are zero coupon bonds. They pay no coupons. • Are often considered the safest investment one can make. • Treasury Notes • Mature in one – ten years after issuance • Pay semi annual coupons • Treasury Bonds • Mature in 20-30 years after issuance • Pay semi annual coupons • Treasuries and many government bonds have some additional tax benefits.

Bond Ratings • “Risk” in the bond market describes the likelihood that a bond issuer will default on its bond payments. • A high risk bond has a high likelihood of not making payments. • A low risk bond will almost certainly pay its bondholders in full. • US Government Bonds are considered the safest in the world. • This attitude is likely the change. • There are 3 main companies that evaluate the riskiness of bonds, Moody’s, S&P and Fitch. • These companies give ratings to bonds that represent the likelihood of default. • The less likely a bond is to default, the more people will be willing to pay for it and the lower the yield will be.

Bond Price Changes • A bond with a maturity in 5 years and a yield of 10% is worth $621.12 today. • $1000/(1.1)5 • What would cause the bond’s price to change? • How does the bond’s price change as time goes by? • What has happened to the bonds of Greece recently? • What happens if better opportunities exist?

Bond Price Changes • P = C/(1+r)t • As a bond nears maturity, its price increases. • t decreases, P increases • If interest rates change, the bond yield changes. • Interest rates up, bond prices down. • Interest rates down, bond prices up. • Interest rates tell the cost of borrowing money in the market. • The higher the coupon rate the higher the bond price. • If the coupon > yield, the price will be > $1000 • If the coupon < yield, the price will be < $1000 • If the company’s risk increases, bond prices decrease. • If we think a company is in financial trouble we will demand higher interest to lend to it. • If we are sure they will go bankrupt we can assume we will only get part of the Face Value at maturity

Greek Bonds • As Greece’s economy shrank and its government spending increased, investors decided that Greek bonds had a high risk of default. • If you held a 10 year Greek bond in January 2010, it would be worth $613.87. • That same bond one year later would be worth $94.34 • Due to default risk yields went from 5% to 30% in less than one year.

Review Bonds and Present Value • Present Value – The current value of a future cash payment. • Bond - a contract that promises to pay the bondholder a specific amount of money at one or more specific points in the future. • Coupon – A regularly occurring payment associated with a bond. • T-Bonds and T-Bills – Bonds issued by the US Federal Government. • Discount Rate = 1/(1+r)t • Present Value of Future Cash Flow, PV = C / [(1+r) t]. • Present Value of a Series of Future Cash Flows PV2 = C2 [(1/r) – (1/[r(1+r)t])] • Interest rates increase, bond prices decrease • Risk increases, bond prices decrease