Download

1 / 29

• 300 likes • 445 Views

Commodity storage valuation: a linear optimization based on traded instruments. Joe W. Byers, Ph.D. Financial Systems & Economic Analytics, LTD. and The University of Tulsa. Introduction.

E N D

Commodity storage valuation: a linear optimization based on traded instruments Joe W. Byers, Ph.D. Financial Systems & Economic Analytics, LTD. and The University of Tulsa

Introduction • Commodity storage enable market participants to “buy” during low price and “sell” during high price periods. • Commodity storage also enable market participants to extract gains during events that disrupt where prices spike or plummet. • Risks associated with commodity market require management of capital at risk. • Monetizing the capital investment in storage is essential, and is accomplished using energy derivative and physical markets.

Why is managing Capital at Risk Important? • Monetizing the physical asset becomes more important as supply and demand relationships change. • The Energy Information Administration even remarks that monetizing commodity storage assets is increasing. Managing commodity storage assets is becoming increasingly more important for companies that invest in these types of assets and utilize these types of asset to serve demand or manage supply.

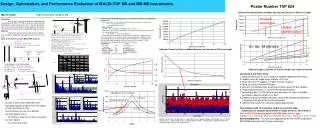

Figure 1.The forward curve exhibits a 155% increase in the short term contract prices from and 100% increases in long term contract price from 1999 to 2004.

Figure 2. The variation of weekly storage inventories is increasing around the five year moving average.

Model Capabilities and Requirements The Model • Is a framework for monetizing the capital investment in a commodity storage facility. • Represents a payoff function for the storage option similar to valuing a vanilla option with Monte Carlo methods under transaction costs. • Is a linear optimization of the fundamental derivative components of a storage facility that can utilize Monte Carlo methods. • Is applicable to many commodities and different types of storage by relaxing assumptions of the model. • Requires a market for energy derivatives and the physical commodity. The primary focus will be on natural gas storage valuation with references to other commodities where applicable.

Types of Storage • Pressurized - Commodity is stored under pressure in a gaseous state like natural gas and gas liquids • Salt cavern, depleted gas reservoirs, and aquifers - abandoned mines and hard rock caverns are under consideration for future development • Pressure vessels like pipelines, liquefied natural gas, and compressed natural gas • Un-pressurized - Commodity is stored at atmospheric pressure like crude oil and refined products • Above ground tanks

Highlights of the domestic natural gas market • Natural gas spot (cash) markets trade across the U. S • Active and liquid exchange is the New York Mercantile Exchange • Storage periods are seasonal with contract periods • A storage year is from 4/1 to 3/31 each year composed of the injection season (4/1 – 10/31) and the withdrawal season (11/1 – 3/31) • Contract periods are for spot (next day ratable delivery), swing swap (balance of month, financial), forwards (ratably delivered over the contract period, normally monthly)

Physical Storage Characteristics • Determine the upper/lower bounds and constraints for the commodity flows • Variables • Maximum (Total) storage capacity • Current Inventory level • Delivered Inventory quantities • Gas available for delivery during current tenor or period • Gas available for delivery during next period arising from contracts expiring prior to the last day of the tenor • Ratchets • Injection and withdrawal rates • Constant: Specified over time interval • Volumetric: Function of current inventory and maximum storage capacity • Schedules • Maintenance • Volume levels

Physical Cost factors are a function of the storage technology Commodity transfer fees (per commodity unit) Tariffs or commodity fee Fuel costs Financial Derivative transactions Forwards, balance of month (BOM), balance of week, and weekend. Determine the future flow of commodity Cash transactions Physical market Financial Storage Characteristics • Storage period: A storage year

“The Storage Option” – Intrinsic Value • The “Calendar Spread” resulting from optimizing a forward position around the storage facility. • Buying the low priced commodity and selling higher priced commodity in the forward markets. • Generates a credit to the cash account enabling or “locking in” certain cash flows thereby reducing capital at risk.

0 K1 0 K1 K2 “The Storage Option” – Extrinsic Value • Extrinsic value is derived from owning physical commodity storage capacity and the ability to transact in the physical product. • This is similar to being long both Gas Daily call and put options, a “Straddle” (see Figure 1), where the call and put have the same strike price. • The storage option differs with the strike prices of the call and put are the forward prices from the intrinsic value calendar spreads making the storage option a strangle, Figure 2. • Extrinsic value is the uncertain or “at risk” component of a storage facility’s value. Figure 3. Figure 4.

Valuation Model - Overview • Commodity storage has two value components: intrinsic and extrinsic. • Commodity storage valuation is a portfolio of fundamental securities (forwards and options) with different strikes and maturities. • This specification, based on fundamental components, replicates derivatives that are actually traded using the payoff function.

Valuation Model - Algorithm • Calculate intrinsic value for day 1, initialize the calendar spreads. • Stage 1: For each trading day until contract expiration. • Calculate optimal forward positions and cash transactions each day given previous days position. • Stage 2: For each trading day until contract expiration. • Calculate the marginal change in value each day and discount to mark date.

Definitions of model parameters and variables • Estimated parameters: wsand is where s is a tenor or contract period. • Variables: • Price: Pslwhere l is a bid or ask price comprised in a price curve. • Cost: costsl where l is injection or withdrawal cost. • Inventory: • Withdrawal capacity is the sum of GIG, GAD current and GAD next period. • Injection capacity is the MSQ less the withdrawal capacity. • Interest rate: exogenous, r. • Tenors: N, contract periods. • Years: storage years. • Numberofperiodsinyuear: and number of contract periods in a storage year. • Constraints: • Master: ensures optimal positions over lifetime. • Storage Year: ensures optimal position during each storage year. • Sales: no short sales restriction • Purchases: no borrowing restriction • Last Period Injection: ensures no injections in last period. • Boundary Conditions: • Withdrawal is between zero and the maximum quantity for the period. • Injection is between the minimum and zero for the period

Valuation Model Stage 2 • Post optimization processing • Calculates the discounted marginal profit for each trading. Where marginal profit is • Post optimization processing tests for the sign of the volume changes, w and i, ensure that the proper bid/ask price is used.

Comments on Implementation • The model was implemented in Visual Basic as a custom dynamic link library. • The development platform of this model utilized Open Software License software from lpSolve and Quantlib.org. • The main graphical user interface and input database were implemented in Excel. • The speed of this implementation improved over alternative implementations in SAS and Matlab. • Modeling the forward prices, P, is not performed here because implementing a forward and spot price simulation process is subjective with respect to the desired complexity of the model. Common price generation process are the log normal models of Heath, Jarrow, and Morton (1990) and Clewlow and Strickland (2000). Fundamental economic models and multi-commodity are alternatives.

Model Inputs • Class parameters • Static Inputs: do not change over the life of the facility • Dynamic Inputs: market driven and facility inventory parameters • Subcategory parameters • Financial: impact revenue and cost components; and include all time dependent variables • Engineering: inputs related to physical volume used to calculate the constraints and boundary conditions of the optimization; and include the daily ratchets.

Valuation Examples: • The two examples are valued using the historical prices from 2/5/2004-3/31/2003 for a price series of 420 days. • One example is a HIGH turn and the other example is a LOW turn. • Historical prices allow benchmarking the model and determining the theoretical value of the facility based on actual events.

Figure 5. Forward prices for 2/4/2002 showing the INTRINSIC value optimal purchase periods (diamonds) and sell periods (squares).

Table 5. Intrinsic optimal positions for mark to market date 2/4/2002.

Summary and Conclusions • The development of this storage model using traded instruments replicates the actual markets that exist because risk neutral valuation is not possible. This methodology also incorporates the path dependencies that are part of the storage option. Path dependencies arise because the level of storage today determines the available set of options the next day. • The paper has presented a simple approach to value commodity storage assets based on linear optimization techniques with Monte Carlo Methods. A benefit of this model is that traded instruments are used in the valuation enabling the model to replicate non-traded components of the storage option. Model values are additive meaning that on a per unit basis 10bcf is equivalent to 100bcf. This additive feature allows a developer to determine a baseline value of storage for determining tariffs for new facilities. This methodology will assist potential storage investors in determining the relative value of storage based on the facility’s characteristics.

Extensions • The model is easily modified to handle overlapping instruments because the linear optimization will optimize over the marginal contribution of each instrument. • The addition of probabilistic injection and withdrawal volumes would enable the model to value exotic options that require a storage asset as a hedge. • Examples of these exotic options for the U. S. natural gas markets are peaking options, swing options, and firm service contracts.