Download

1 / 38

E N D

Pricing Your Food Product Module designed by Tera Sandvik, LRD, Program Coordinator; Julie Garden-Robinson, PhD, LRD, Food and Nutrition Specialist;and Kathleen Tweeten, MBA, Director, Center for Community Vitality, Community Economic Development Extension Specialist; Module updated in 2014 by Kimberly Beauchamp, Food Safety/Food Entrepreneur Extension Specialist. 2014

The following tips will help you navigate through each module. • Click the left mouse button or the down arrow to continue on to the next bullet or slide. • Before you begin, you’ll take a presurvey. • The presurvey will open in a new window. • When you are finished with the presurvey, close the window to return to the module. • A symbolizes a question slide. You’ll need to click your mouse once to see the answer.

A means you’ll need to go to the site listed to answer the question. • After visiting the site, close the Internet browser to return to the module. • Click your mouse once to see the answer. • When you are finished with the module, you will take a post-survey. • The post-survey will open in a new window. • When you are finished with the post-survey, close the window to return to the module.

Presurvey • Before we begin let’s take a presurvey to see how much you already know. • Click here to begin the presurvey.

I have my product, but how much is it worth? $20 $100 $30 $10 $5 $75 $15 $35 $40

Costs • When selling a product, make sure you make enough profit to cover your: • Fixed costs • Variable costs

Fixed Costs • Fixed costs are expenses that must be paid no matter how many goods or services are offered for sale. • Some examples are: • Rent • Utilities • Insurance • Internet service

Variable Costs • Variable costs are expenses that change with the number of products offered for sale. • Some examples are: • Raw materials (jars, sugar, etc.) • The more products you sell, the more raw materials you need to produce the extra products. • Electric power to run machines • Cost of maintaining inventory

You have ways to reduce fixed costs per unit sold. • If you sell more units, the percentage of fixed costs is reduced. For example: • Variable cost = $1.50 • Fixed cost = $50 • Units sold = 100 • Price per unit = $4 • %Fixed cost = 25% • If units sold increased to 200: • %Fixed cost = 14% $1.50 x 100 units = $150 $150 + $50 = $200 (total cost) $50/$200 = 25% $1.50 x 200 units = $300 $300 + $50 = $350 $50/$350 = 14%

Which of the following is a fixed cost? • Sugar • Rent • Jars Click to see the answer.

Which of the following is a variable cost? • Insurance • Rent • Sugar Click to see the answer.

Now that you know what fixed and variable costs are, let’s move on to break even analysis. • The break even point is how many products you must sell to cover your costs. • We’ll go through an example on the next slide, followed by a link that will give you your break even point.

Example • Variable cost (VC) = $2.50 • Fixed cost (FC) = $500 • Price per unit (PPU) = $5 • How many units (A) must you sell to break even? • (VC x A) + FC = PPU x A • (2.50 x A) + 500 = 5 x A • 500 = 5A – 2.5A • 500 = 2.5A • 500/2.5 = A • A = 200 units must be sold to break even

Go to the following link using the same numbers as the previous example and you should get the same answer of 200 units. • http://www.dinkytown.net/java/BreakEven.html • In case you forgot: • Variable cost = 2.50 • Fixed cost = 500 • Price per unit = $5 • Hint: Expected unit sales is anything greater than 1.

In the previous examples, the break even point was 200 units. • If more than 200 units are sold, you will have a profit; if less than 200 units are sold you will have a loss

Go to: http://www.dinkytown.net/java/BreakEven.html • Plug the following numbers into the break even calculator. Is there a profit or a loss? • Variable cost = $2 • Fixed cost = $300 • Expected unit sales = $200 • Price per unit = $4 Click to see the answer. Profit

Go to: http://www.dinkytown.net/java/BreakEven.html • Plug the following numbers into the break even calculator. What is the break even point? • Variable cost = $3 • Fixed cost = $400 • Expected unit sales = $200 • Price per unit = $6 Click to see the answer. 133 Units

Marginal cost • Marginal cost by definition is the change in cost that results from changing the output by one unit. • Basically it’s the difference in variable costs based on units sold. • For example: • Variable cost = $200 for 15 units sold • Variable cost = $215 for 16 units sold • Marginal cost difference = $15 • The difference between variable costs

Marginal cost • Go to: http://hspm.sph.sc.edu/Cost.html for a more in-depth, interactive explanation about marginal costs. • Remember to come back after exploring the Web site.

What is marginal cost? • The change in cost that results from changing the output by one unit • The cost of overhead • The charge for permanent part-time labor • None of the above Click to see the answer.

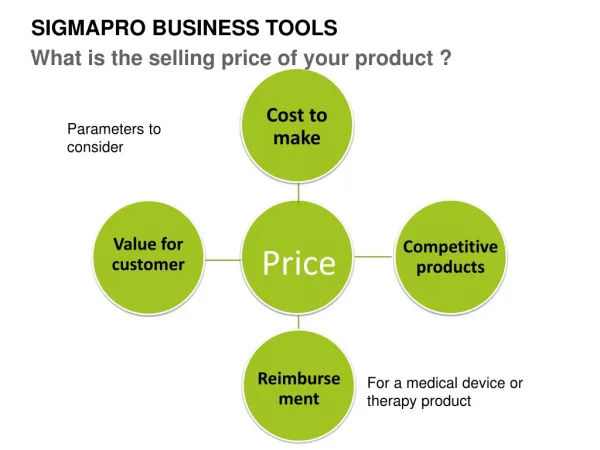

Pricing your product • You have a few ways to price your product: • Cost-plus pricing • Cost-based pricing • Percent food cost pricing • Contribution pricing • Working-back method (expected return)

Before moving on to pricing methods, let’s review a couple of terms and go over a couple of new ones. • Fixed costs are expenses that must be paid no matter how many goods or services are offered for sale. • Variable cost are expenses that change with the number of products offered for sale. • Direct costs are directly related to the production of a product. • Cost of sugar to make jelly is a direct cost. • Indirect costs are not directly related to the product, but have to do with overall production. • Rent would be an indirect cost.

Cost-plus pricing • This is a simple and popular way to price a product/service. • You buy 100 products for $1,000. • $1,000/100 = $10 • This is the basis for which you sell each product. • If you want a 20% profit, you should sell the product for $12 (120% x $10). • This method allows you to cover all direct costs and generate a profit. • The downside is you have not considered the needs of the market or compensated for any indirect costs.

Use the cost-plus pricing method in the following example. • You buy 50 products for $1,000 and want to make a profit of 30%. • What’s the selling price? Click to see the answer. $1,000/50 = $20 $20 x 130% = $26 The selling price should be $26.

Cost-based pricing • Cost-based pricing uses unit costs of ingredients, expenses and labor to determine the price. • Costs will fall under fixed or variable costs. • You need to know your total costs before you can find your break even point. • Once you know your total costs, figure out how much you must sell your product for to cover them. • Then add your profit.

Cost-based pricing example • Fixed costs = $200 • Variable costs = $5 • Units = 100 • You want a profit of 20% • $200 + (100 x $5) =$700 • Total costs = $700 • $700/100=$7 (If you sold them for $7 you would break even) • $7 x 120% = $8.40 • The selling price should be $8.40 to cover costs and make a 20% profit.

Use the cost-based pricing method in the following example. • Fixed costs = $100 • Variable costs = $3 • Units = 50 • You want a profit of 20%. What’s the selling price? Click to see the answer. • $100 + (50 x $3) = $250 • Total costs = $250 • $250/50 = $5 (If you sold them for $5.00 you would break even) • $5 x 120% = $6 • The selling price should be $6 to cover costs and make a 20% profit.

Percent food cost pricing • Percent food cost pricing is based on the theory that food cost makes up about 40 percent of the price. • To establish a price, multiply the food cost by 2.5 (40 percent times 2.5 = 100 percent). • This method commonly is used for catering businesses, but only if a product does not require a great deal of labor or if ingredients are not very expensive.

Use the percent food cost pricing method in the following example. • It costs you $2 to make a club sandwich. • What should the selling price be? Click to see the answer. $2 x 2.5 = $5 You should sell the sandwich for $5.

What information do you need to figure out percent food cost pricing? • Cost of labor • Kitchen remodeling cost • Insurance cost • Food cost Click to see the answer.

Contribution pricing • Contribution pricing allows you to cover all direct costs (per product), but also allows a contribution toward indirect costs and profit. • The next slide will walk you through an example.

Use the contribution pricing method in the following example. • Your product has a direct cost of $50 and you want to make a contribution of $20 to indirect cost and profit. • If indirect costs are $1,000 and you want to make a profit of $300, how many products do you have to sell? Click to see the answer. $1,000 + $300 = $1300 (indirect cost + profit) $1,300/$20 = 65 You need to sell 65 products to cover indirect cost and make a $300 profit.

Working-back method • This method is most useful for smaller businesses. • If a business sells 100 products each month and the total costs (fixed, direct, indirect, etc.) for the month are $1,000 and the business owner expects to cover all his costs and make a profit of 50%, he must sell $1,500 worth of products. • Therefore, the business owner sells his products at: • $1,500 / 100 units = $15 per product

Working-back method cont. • If your price is higher than the competitor using this method, offer something more to compensate for the higher price. • For example: • A competitor charges $100 for a cake. As a result of using this pricing method you charge $120. To prevent losing customers to the cheaper business, upgrade your service to include delivering the cake. • The extra quality in the service may require slightly longer hours, but it will compensate for the higher price.

Use the working-back pricing method in the following example. • You sell 200 products each month. • Total cost = $500 • You want a 50% profit • What should your selling price be? Click to see the answer. 500 x 150% = 750 750/200 = $3.75 You should sell your product at $3.75 to make a 50% profit.

We hope this module has helped you determine what your product is worth. Use this module, along with the other modules, to get you on your way.

Post-survey • Let’s see what you’ve learned. • Click here to begin the post-survey. • The last slide shows additional resources. • After the slideshow is done go to “File” and click on “Print.” • A box will open up. • Click on “Slides” under “Print Range.” • Type in “38” and click on “okay.”

Additional Resources • University of Omaha • http://ecedweb.unomaha.edu/lessons/euse2.htm • Interactive Tutorial • http://hspm.sph.sc.edu/COURSES/ECON/Cost/Cost.html