Download

1 / 12

120 likes | 532 Views

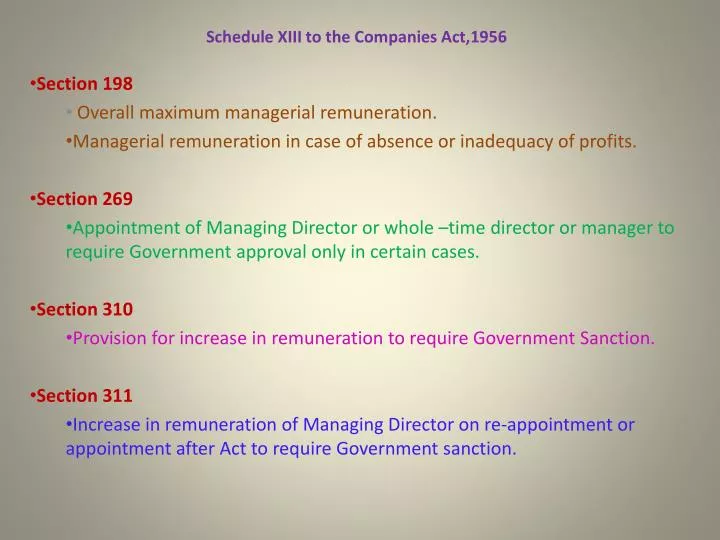

Schedule XIII to the Companies Act,1956. Section 198 Overall maximum managerial remuneration. Managerial remuneration in case of absence or inadequacy of profits. Section 269

E N D

Schedule XIII to the Companies Act,1956 Section 198 Overall maximum managerial remuneration. Managerial remuneration in case of absence or inadequacy of profits. Section 269 Appointment of Managing Director or whole –time director or manager to require Government approval only in certain cases. Section 310 Provision for increase in remuneration to require Government Sanction. Section 311 Increase in remuneration of Managing Director on re-appointment or appointment after Act to require Government sanction.

Overall Managerial Remuneration- Section 198 & Section 309 Situation 1: 11% ( Over all Maximum u/s 198) Where the Board has at least One Whole -Time Director & At least one Non-Executive Director Plus A Managing Director 10% Plus 1% u/s 309 u/s 309 Situation 2: 10% (Over all Maximum u/s 309) Where the Board does not have any Non-Executive Director and has at least Two whole-time directors Plus A Managing Director 10% Plus 0% Situation 3: 6%(Over all Maximum u/s 309) { Where one whole –time director Or a Managing Director } and at least Two Non-Executive director s 5% Plus 1%

Overall Managerial Remuneration –Section 198 & Section 309 Situation IV 3%( Overall maximum U/S 309) No whole Time Director At least Three Non –Executive Directors 0% Plus 3% “There does not exist any other possible combination of Whole-Time and Non –Executive directorship on the Board of a Public Company that may yield a different %age of Overall Managerial Remuneration .” Can a Company breach the above ‘Overall Managerial Remuneration” % age ??? Why Not ? Form 25A !!

Situation where there is no or inadequate Profits or adequate profits What is Schedule XIII to the Companies Act ,1956 ? Which are the companies to which Schedule XIII is applicable ? When has a company to refer to schedule XIII ? : Is it at the Time of Appointment of a director ,or, Is it at the time of fixing of remuneration of a director, or, Is it when the company incurs losses or has inadequate profit ,or, Is it at the time of appointment of directors upon incorporation of a Company ,or, Is it applicable to even companies making profits ? What happens if the appointment is made in violation of Schedule XIII ? What happens if the appointment is made in accordance with Schedule XIII and an approval is sought from the Central Government on managerial remuneration in excess of the limits prescribed in the aforesaid schedule, if : The approval is granted The approval is denied. Recent amendments to Schedule XIII – An audacious step by MCA

Schedule XIII is divided into three Parts Schedule XIII Appointment Remuneration Anatomy of Schedule XIII: is not further divided into sections Part - I Section I – Companies having Profits is further divided into three sections Section II- Companies with no or inadequate Section I , Section II & Section III profits Section III - Remuneration from Part-II Two companies Part III Secretarial compliance

Part I to Schedule XIII to the Companies Act,1956 Part I prescribes host of Acts under which the appointee as a Managing or Whole –Time director or as a manager should not be convicted of an offence and sentenced to imprisonment for any period or with a fine exceeding Rupees One Thousand : The Indian Stamp Act, 1899, The Central Excise and Salt Act,1944, The Industries (development & Regulation )Act,1951, The Prevention of Food Adulteration Act,1954, The Essential Commodities Act ,1955, The Companies Act,1956, The Securities contracts (Regulation Act) ,1956, The wealth Tax Act,1957, The Income Tax Act,1961, The Customs Act,1962, The MRTP Act,1969, The FERA,1973, The Sick Industrial Companies ( Special Provisions ) Act, 1985, The SEBI Act, 1992, The Foreign Trade (development and regulation ) Act,1992 He should not be detained for any period under the COFEPOSA ACT , 1974

Age should not be 70 or more Age should be 25 or more At the time of appointment or re-appointment : AND or a Younger or an Older appointee acceptable ?? Section 280 –Age limit Section 281- Age limit not to apply if company so resolves Section 282- director to disclose age Already a managerial personnel in one or more companies at the time of appointment or re-appointment – he draws remuneration from one or more companies subject to the ceiling provided in Section III or Part II. He is resident in India… What if the appointee is an Expat ?? ( A foreigner visiting India on an E-Visa – Can his appointment be covered in Schedule XIII as a Valid appointment for a whole-time director or a Managing Director) Does appointment of Non-Executive foreign directors get covered in Schedule XIII ??? Does appointment of Non-Executive directors who are resident in India get covered in Schedule XIII ??

Section 267-Certain persons not to be appointed Managing Directors ! Section 274- Disqualification of directors- A person shall not be capable of being appointed director of a Company ! Provisions of sub-section (2) of Section 269 which refers to Schedule XIII and conditions imposed under Part I of that Schedule….Are these additional conditions for eligibility for appointment ?? Some interesting facts on eligibility for appointment

Part II Section I Net Profit Remuneration Payable by Companies As per Section 349 having profits As per section 350 Maximum 5% of its Net Profit for one such Managerial Personnel Maximum 10% of its Net Profit for all of them where there is more than one Managerial Personnel Section II Section III Remuneration Payable by Companies Remuneration Payable to a managerial Personnel in Two having no profits or inadequate profits Companies.------The total remuneration shall not exceed the higher maximum limit admissible from any one of the of which he is a managerial personnel. Effective Capital of the Company Ceiling Limit Under Sub-Paragraph (A) – “Conditions Apply” Ceiling Limit Under Sub-Paragraph (B) - “ Conditions Apply” Effective Capital of the Company Exceeding the Ceiling Limit Under Sub-Paragraph ( C ) –”Conditions Apply” Definition of “Effective Capital” Definition of “ Managerial remuneration”

A. Managerial Remuneration : It includes : Base Salary + Dearness Allowance + Other Allowances + Perquisites + Commission It excludes { For both Indian nationals and Foreign nationals} Employer’s contribution to PF + Superannuation Fund Or Annuity Fund which in total should not exceed 27% of Base salary. Gratuity payable at a rate not exceeding ½ month’s Base Salary for each completed year of service. Encashment of Leave at the end of the tenure. It excludes { Only for Foreign nationals } Children’s Education Allowance- Maximum INR 5K per child up to a maximum of two children. Holiday passage for children studying outside India / Family staying abroad. Leave Travel Concession –return passage for self and family . B. Effective Capital : It includes : 1.{ Paid up Share Capital + Share Premium Account + Reserves and Surplus+ Long Term Loans + Deposits repayable after One year} – { Investments + Preliminary Expenses + Accumulated Losses } It excludes: Working Capital Loans + Over-Drafts + Interest due on loans unless funded+ Bank Guarantee + Other Short Term arrangement } Note: Reserves & Surplus should not include “Capital reserve’.

Scale under Sub-Paragraph (A): Where the effective capital of Company is : Monthly Remuneration Payable (INR) Shall not Exceed ( INR) Not exceeding the Ceiling Limit of Rs. 2.4MM p.a. or Rs. 200K p.m. as per the following scale: < INR 1 crore 75K > or = 1 Crore < 5 Crore 100K > or = 5 Crore < 25 Crore 125K > or = 25 Crore < 50 Crore 150K > Or = 50 Crore < 100 Crore 175K > Or = 100 Crore 200K 2. Scale under Sub-Paragraph (B) : Where the effective capital of Company is : Monthly Remuneration Payable (INR) Shall not Exceed ( INR) Not exceeding the Ceiling Limit of Rs. 4.8 MM p.a. or Rs. 400K p.m. as per the following scale: < INR 1 crore 150K > or = 1 Crore < 5 Crore 200K > or = 5 Crore < 25 Crore 250K > or = 25 Crore < 50 Crore 300K > Or = 50 Crore < 100 Crore 350K > Or = 100 Crore 400K Exceeding the Scale as per Sub –Paragraph ( C )

“Conditions Apply “ Sub-Paragraph ( B): Apart from the first two conditions of Sub-Paragraph (A) 3. Special Resolution for payment of remuneration for a period not exceeding three years. 4.Notice to contain a detailed statement of particulars of the Appointee / Industry / Disclosure of remuneration Sub-Paragraph ( A) : Remuneration Committee Has not made default in repayment of any of its debts ( including Public deposits ) or debentures of interest payable thereon for a continuous period of thirty days in the preceding financial year before the DOA. Sub-Paragraph ( C) : 5. Effective Capital Negative 6. Prior approval of Central Government is obtained.