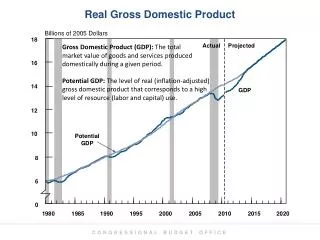

Download

1 / 44

440 likes | 555 Views

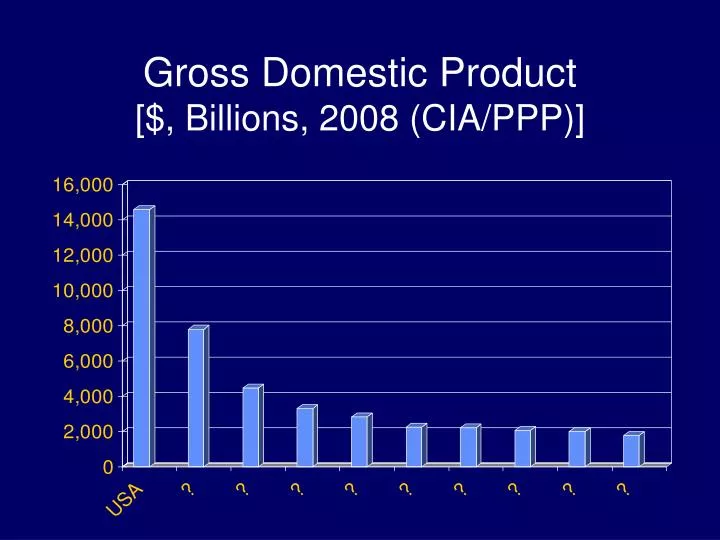

Gross Domestic Product [$, Billions, 2008 (CIA/PPP)]. Gross Domestic Product [$, Billions, 2008 (CIA/PPP)]. Gross Domestic Product [$, Billions, 2008 (CIA/PPP)]. Shapiro: Chapter 4 – The Law of One Price. Chapter 4 Problems. Problem 4.7. The Law of One Price. “Exchange-adjusted prices …

E N D

Chapter 4 Problems • Problem 4.7

The Law of One Price • “Exchange-adjusted prices … • of identical, tradable goods and financial assets … • must be within transaction costs of equality worldwide.”

The Law of One Price • Enforced by arbitrageurs - ??? • Enforced by arbitrageurs - buy in one market and sell in another

“Students Find $100 Textbooks Cost $50, Purchased Overseas”New York Times, 10-21-03

The Law of One Price • Enforced by arbitrageurs - buy in one market and sell in another • Risk-adjusted expected returns on financial assets in different markets should be equal

5 Key Economic Relationships • Purchasing Power Parity (PPP) • Fisher Effect (FE) • International Fisher Effect (IFE) • Interest Rate Parity (IRP) • Forward Rates as unbiased predictors of future spot rates (UFR)

Exhibit 4.1 Five Key Theoretical Relationships Among Spot Rates, Forward Rates, Inflation Rates, and Interest Rates

Purchasing Power Parity (PPP) • “The ratio between domestic and foreign price levels should equal the equilibrium exchange rate between domestic and foreign currencies.” • $1 = loaf of bread • $1 = £0.6475 • £0.6475 = loaf of bread

Purchasing Power Parity (PPP) • Relative Version: “Exchange rate between the home currency and any foreign currency will adjust to reflect changes in the price levels of the two countries.”

Purchasing Power Parity (PPP) • Inflation = 5% (USA)Inflation = 3% (Switzerland)$ value of SFr must rise by 2% • et (1 + ih)t--- = ------------e0 (1 + if)t 2%

Purchasing Power Parity (PPP) • Inflation = 5% (USA) • Inflation = 3% (Switzerland) • SFr 1 = $0.75 (spot) • What is e3?

Purchasing Power Parity (PPP) • The exchange rate change during a period should equal the inflation differential for that same period. • “Currencies with high rates of inflation should devalue relative to currencies with lower rates of inflation.”

Purchasing Power Parity (PPP) Shapiro: Exhibit 4.4

Fisher Effect • Nominal interest rate (r) consists of: • real required rate of return, a • an inflation premium, i • 1 + r = (1 + a)(1 + i) • Real returns are equalized across countries through arbitrage.

Fisher Effect • ah = af • rh - rf = ih - if • Currencies with high rates of inflation should bear higher interest rates than currencies with lower rates of inflation

Exhibit 4.7 Fisher Effect: Empirical Data, May 2007

International Fisher Effect • “Currencies with low interest rates are expected to appreciate relative to currencies with high interest rates.”

International Fisher Effect • The expected home country (HC) returns from investing at home and abroad should be equal. • 1 + rh = (1 + rf)(e1/e0)

Interest Rate Parity (IRP)[Covered Interest Arbitrage] • “A condition where the interest rate differential is approximately equal to the forward differential between two currencies.”

Interest Rate Parity (IRP)[Covered Interest Arbitrage] • Interest rate (London) = 12% • Interest rate (New York) = 7% • £ spot rate: £1 = $1.95 • 1-year forward rate: £1 = $1.88 • Forward differential: • ($1.88 - $1.95) / $1.95 = -3.6% • Rate differential: 12% - 4% = 8%

Forward Rates as Unbiased Predictors of Future Spot Rates (UFR) • “The forward rate should reflect the expected future spot rate on the date of settlement.” • f1 = e1

Forward Rates as Unbiased Predictors of Future Spot Rates (UFR) • Example: • 90-day forward rate: SFr1 = $0.75 • future spot rate: SFr1 = $0.75 • Empirical evidence: • forward rate appears biased • bias caused by risk premium • premium appears to average out

Currency Forecasting • Forecasting requirements: • superior models • superior, consistent information • small, temporary deviations • predict government intervention

Currency Forecasting • Market-based forecasts: • forward rates • interest rate differentials • Model-based forecasts • fundamental analysis • technical analysis

Shapiro: Problem 4-7a • iUSA = 10% • iGDR = 4% • 1€ = $0.95 • Exchange rates for next five years? • €t = $0.95(1.10/1.04)t

Shapiro: Problem 4-7b • iUSA = 3.2% • iGDR = 1.5% • e5 = $0.99/€ • Real value of the €? • €5 = .95(1.032/1.015)5 = 1.0323 • (.99 – 1.0323) / 1.0323 = -4.1%