Download

1 / 52

E N D

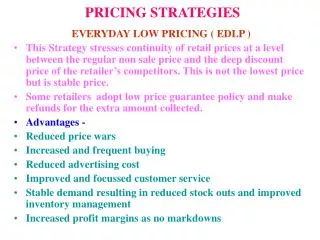

Pricing strategies • Pricing strategies for products or services encompass three main ways to improve profits. These are that the business owner can cut costs or sell more, or find more profit with a better pricing strategy. When costs are already at their lowest and sales are hard to find, adopting a better pricing strategy is a key option to stay viable. • Merely raising prices is not always the answer, especially in a poor economy. Too many businesses have been lost because they priced themselves out of the marketplace. On the other hand, too many business and sales staff leave "money on the table". One strategy does not fit all, so adopting a pricing strategy is a learning curve when studying the needs and behaviors of customers and clients

Penetration pricing is designed to achieve sale-based objectives. It is the strategy of entering the market with a low initial price so that a greater share of the market can be captured. • The penetration strategy is resorted to when demand seems to be elastic over the entire demand curve. • High price elasticity of demand is probably the most important reason for adopting the penetration strategy. • The penetration strategy is also used to discourage competitors from entering the market.

Among situations suggesting a strategy of penetration pricing are: • Preparations, to which the consumer/payer reacts very susceptibly to the price (high price elasticity). • Achieving the fast growth sales volume. • Achieving the high market share and, thus, a strong market position by the time of the competitors' entry. • Utilization of experience curves ("learning curves") and the magnitude advantages in production ("economies of scale"). Low introductory prices reduce risk of a flop. • Hindering potential competitors to enter the market.

Skimming pricing • Skimming pricing is the strategy of establishing a high initial price for a product to "skim the cream" off the upper end of the demand curve. It is aimed at achieving profit-based objectives. It is usually accompanied by heavy promotion expenditures.

Skimming pricing • A skimming strategy may be recommended when the nature of the demand is uncertain, when a company has expended large sums of money on research and development of a new product, when the competition is expected to develop and market a similar product in the near future, or when the product is so innovative that the market is expected to mature very slowly.

Other situations, in which skimming pricing may be considered are: • Preparations, to which the consumer does not react very susceptibly to the price (low price elasticity). • Achieving short-term profits. • Quick amortization of research and development. • Making profits in the early phases of the products' lifecycle (reducing the risk that new, better preparations contribute to loss of profit). • Avoiding the necessity of price increases. • Margin for price reductions. • High prices signalize high quality.

The decision on how high a skimming price should be will depend on two factors: • (1) chances of competitors entering the market, and • (2) the price elasticity at the upper layer of the demand curve. • If competitors are expected to bring out their own brands quickly, it may be safe to price rather high.

Value Pricing Price set in accordance with customer perceptions about the value of the product/service Examples include status products/exclusive products Companies may be able to set prices according to perceived value.

Loss Leader Goods/services deliberately sold below cost to encourage sales elsewhere Typical in supermarkets, e.g. at Christmas, selling bottles of gin at £3 in the hope that people will be attracted to the store and buy other things Purchases of other items more than covers ‘loss’ on item sold e.g. ‘Free’ mobile phone when taking on contract package

Psychological Pricing Used to play on consumer perceptions Classic example - £9.99 instead of £10.99! Links with value pricing – high value goods priced according to what consumers THINK should be the price

Going Rate (Price Leadership) In case of price leader, rivals have difficulty in competing on price – too high and they lose market share, too low and the price leader would match price and force smaller rival out of market May follow pricing leads of rivals especially where those rivals have a clear dominance of market share Where competition is limited, ‘going rate’ pricing may be applicable – banks, petrol, supermarkets, electrical goods – find very similar prices in all outlets

Tender Pricing Many contracts awarded on a tender basis Firm (or firms) submit their price for carrying out the work Purchaser then chooses which represents best value Mostly done in secret

Price Discrimination Charging a different price for the same good/service in different markets Requires each market to be impenetrable Requires different price elasticity of demand in each market Prices for rail travel differ for the same journey at different times of the day

Destroyer/Predatory Pricing Deliberate price cutting or offer of ‘free gifts/products’ to force rivals (normally smaller and weaker) out of business or prevent new entrants Anti-competitive and illegal if it can be proved

Absorption/Full Cost Pricing Full Cost Pricing – attempting to set price to cover both fixed and variable costs Absorption Cost Pricing – Price set to ‘absorb’ some of the fixed costs of production

Marginal Cost Pricing Marginal cost – the cost of producing ONE extra or ONE fewer item of production MC pricing – allows flexibility Particularly relevant in transport where fixed costs may be relatively high Allows variable pricing structure – e.g. on a flight from London to New York – providing the cost of the extra passenger is covered, the price could be varied a good deal to attract customers and fill the aircraft

Marginal Cost Pricing Example: Aircraft flying from Bristol to Edinburgh – Total Cost (including normal profit) = £15,000 of which £13,000 is fixed cost* Number of seats = 160, average price = £93.75 MC of each passenger = 2000/160 = £12.50 If flight not full, better to offer passengers chance of flying at £12.50 and fill the seat than not fill it at all! *All figures are estimates only

Contribution Pricing Contribution = Selling Price – Variable (direct costs) Prices set to ensure coverage of variable costs and a ‘contribution’ to the fixed costs Similar in principle to marginal cost pricing Break-even analysis might be useful in such circumstances

Target Pricing Setting price to ‘target’ a specified profit level Estimates of the cost and potential revenue at different prices, and thus the break-even have to be made, to determine the mark-up Mark-up = Profit/Cost x 100

Cost-Plus Pricing Cost-plus pricing is where prices are determined by adding a predetermined profit to costs. It is the simplest form of cost-based pricing. In general, the steps for computing cost-pricing are to estimate the number of units to be produced, calculate fixed and variable costs, and add a predetermined profit to costs. The formula for cost-plus pricing is as follows: P = Total fixed costs + Total variable costs + Projected profit

Although the cost-plus method is easy to compute, it has several shortcomings. Profit is not expressed as a percent of sales, but as a percent of cost, and price is not tied to demand. • Adjustments for rising costs are poorly conceived, and there are no plans for using the excess capacity. There is little incentive for the firm to improve efficiency to hold down costs, and marginal costs are rarely analyzed.

Influence of Elasticity Any pricing decision must be mindful of the impact of price elasticity The degree of price elasticity impacts on the level of sales and hence revenue Elasticity focuses on proportionate (percentage) changes PED = % Change in Quantity demanded/% Change in Price

Influence of Elasticity Price Elastic: % change in quantity demanded > % change in price e.g. A 4% rise in price would lead to sales falling by something more than 4% Revenue would fall A 9% fall in price would lead to a rise in sales of something more than 9% Revenue would rise

In competition-based pricing, the firm uses competitors' prices rather than demand or cost considerations as its primary guideposts. • With this approach, the company may not respond to changes in demand or costs unless they have an effect on competitors' prices. • A company may set prices below the market, at the market, or above the market, depending on its customers, image, the overall marketing mix, the consumer loyalty and other factors.

The competition-based pricing is popular for several reasons. It is simple, with no calculations of demand curves, the price elasticity, or costs per unit. The ongoing market price level is assumed to be fair for both consumers and companies

Price Quotations List prices: Established prices normally quoted to potential buyers Market price: Price that an intermediary or final consumer pays for a product after subtracting any discounts, rebates, or allowances from the list price 19-43

Discounts and Allowances Quantity discount: The more you buy, the cheaper it becomes-- cumulative and non-cumulative. Trade discounts: Reductions from list for functions performed-- storage, promotion. Cash discount: A deduction granted to buyers for paying their bills within a specified period of time, (after first deducting trade and quantity discounts from the base price) 14 - 44

Reductions from List Price Cash discount: price reduction offered to a consumer, industrial user, or marketing intermediary in return for prompt payment of a bill 2/10 net 30, a common cash discount notation, allows consumers to subtract 2 percent from the amount due if payment is made within 10 days 19-45

Calculating a Cash Discount 3/10, NET 30 Percentage to be deducted if bill is paid within specified time Number of days from date of invoice in which bill must be paid to receive cash discount Number of days from date of invoice after which bill is overdue 1/7, NET 30 14 - 46

Trade Discounts: payment to a channel member or buyer for performing marketing functions; also known as a functional discount 19-47

Quantity discount: price reduction granted for a large-volume purchase Justified on the grounds that large orders reduce selling expenses, storage, and transportation costs Cumulative quantity discounts reduce prices in amounts determined by purchases over stated time periods Non-cumulative quantity discounts provide one-time reductions in the list price 19-48

Allowances Trade-in: credit allowance given for a used item when a new item is purchased Promotional allowance: advertising or promotional funds provided by a manufacturer to other channel members in an attempt to integrate the promotional strategy within the channel Rebates: refund for a portion of the purchase price, usually granted by the product’s manufacturer 19-49

Break-even analysis • One way to use the market demand in price determination, and still consider costs, is to conduct the break-even analysis and determine break-even points. • A break-even point is that quantity of output, at which the sales revenue equals the total costs, assuming ascertain selling price. Thus, there is a different break-even point for each different selling price. • Sales of quantities above the break-even output result in a profit on each additional unit. The further the sales are above the break-even point, the higher the total and unit profits. Sales below the break-even point result in a loss to the seller.