Download

1 / 6

60 likes | 220 Views

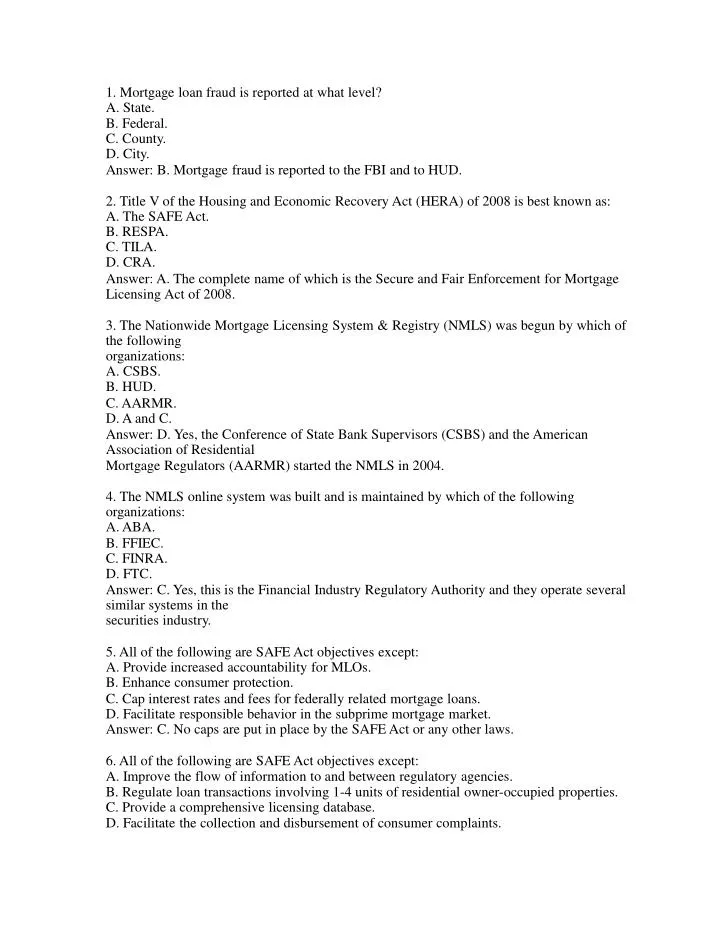

1. Mortgage loan fraud is reported at what level? A. State. B. Federal. C. County. D. City. Answer: B. Mortgage fraud is reported to the FBI and to HUD. 2. Title V of the Housing and Economic Recovery Act (HERA) of 2008 is best known as: A. The SAFE Act. B. RESPA. C. TILA. D. CRA.

E N D

1. Mortgage loan fraud is reported at what level? A. State. B. Federal. C. County. D. City. Answer: B. Mortgage fraud is reported to the FBI and to HUD. 2. Title V of the Housing and Economic Recovery Act (HERA) of 2008 is best known as: A. The SAFE Act. B. RESPA. C. TILA. D. CRA. Answer: A. The complete name of which is the Secure and Fair Enforcement for Mortgage Licensing Act of 2008. 3. The Nationwide Mortgage Licensing System & Registry (NMLS) was begun by which of the following organizations: A. CSBS. B. HUD. C. AARMR. D. A and C. Answer: D. Yes, the Conference of State Bank Supervisors (CSBS) and the American Association of Residential Mortgage Regulators (AARMR) started the NMLS in 2004. 4. The NMLS online system was built and is maintained by which of the following organizations: A. ABA. B. FFIEC. C. FINRA. D. FTC. Answer: C. Yes, this is the Financial Industry Regulatory Authority and they operate several similar systems in the securities industry. 5. All of the following are SAFE Act objectives except: A. Provide increased accountability for MLOs. B. Enhance consumer protection. C. Cap interest rates and fees for federally related mortgage loans. D. Facilitate responsible behavior in the subprime mortgage market. Answer: C. No caps are put in place by the SAFE Act or any other laws. 6. All of the following are SAFE Act objectives except: A. Improve the flow of information to and between regulatory agencies. B. Regulate loan transactions involving 1-4 units of residential owner-occupied properties. C. Provide a comprehensive licensing database. D. Facilitate the collection and disbursement of consumer complaints.

Answer: B. The SAFE Act never mentions 1-4 units of residential owner-occupied properties. It does mention any residential mortgage loan that is primarily for personal, family, or household use. 7. Which of the following agencies reviewed and approved the model state law written by CSBS and AARMR: A. HUD. B. USDA. C. Dept of Veterans Affairs. D. OTS. Answer: A. Yes, the Department of Housing and Urban Development reviewed the model legislation for definitions, education and testing requirements, financial responsibility, and criminal background standards for MLOs and found that it met the minimum requirements for the SAFE Act. 8. According to the SAFE Act, a mortgage loan originator must have the MLO designation to perform all of the following duties except: A. Take a residential mortgage loan application. B. Perform work related to extensions of credit for timeshare plans. C. Negotiate terms of a residential mortgage loan. D. Advise a consumer on rates, fees, and other costs. Answer: B. An individual would not need the MLO designation to perform work related to extensions of credit for timeshare plans. 9. All of the following MLOs are required to be state-licensed except: A. An MLO working under the authority of the Bureau of Real Estate. B. An MLO working as a Consumer Finance Lender (CFL). C. An MLO working for a federally insured depository institution. D. An MLO working as a mortgage banker through the DBO. Answer: C. This would include banks, credit unions, and subsidiaries owned and controlled by a depository institution and regulated by a federal banking agency. 10. According to the SAFE Act, which of the following do not need to have a unique identifier number to work as an MLO: A. An employee of an insured depository institution. B. An MLO working under the authority of the BRE. C. An MLO working under the authority of the DBO. D. None of the above. Answer: D. All MLOs need a unique identifier number. The employee of the insured depository institution, however, is registered with NMLS, not licensed. 11. Clerical and support duties that do not require the MLO designation under the SAFE Act include all of the

following except: A. Communicating with a consumer to obtain information necessary for processing a loan application. B. Collecting information on behalf of a consumer regarding a residential mortgage loan. C. Analysis of information common for processing or underwriting a residential mortgage loan. D. The collection and receipt of information necessary for processing or underwriting a residential mortgage loan. Answer: B. These other tasks are considered clerical and supportive in nature and do not require one’s own MLO designation. 12. Which of the following best defines appraisal: A. Same as price. B. An estimate of value. C. Same as cost. D. An estimate of market value. Answer: D. There is nothing wrong with “B” as an answer, but in the context of residential mortgages, “D” is the best answer and will contribute to your point total. 13. According to the SAFE Act, administrative and clerical tasks that do not require an MLO designation include all of the following except: A. The receipt and collection of information common for the processing or underwriting of a residential mortgage loan. B. Collecting information on behalf of the consumer with regard to a residential mortgage loan. C. The distribution of information common for the processing or underwriting of a residential mortgage loan. D. Communication with a consumer to obtain information necessary for the processing and underwriting of a residential mortgage loan. Answer: B. The correct answer involves obtaining information for the consumer from various industry sources. This is part of MLO activities and requires the MLO designation. The other answer choices involve receiving, collecting, distributing, and communicating with the consumer to obtain information from the consumer for the purpose of putting together the loan application package. This is clerical in nature. 14. Federal Banking Agencies include all of the following except: A. Comptroller of the Currency. B. Director of the Office of Thrift Supervision. C. Department of Housing and Urban Development. D. Federal Deposit Insurance Corporation. Answer: C. Other Federal Banking Agencies include the Board of Governors of the Federal Reserve System, and the

National Credit Union Administration. The Department of HUD is not a federal banking agency. 15. Which of the following parties in the residential mortgage industry would not have to have the MLO designation to perform their duties legally: A. A loan processor performing clerical duties under the direction of a state licensed MLO. B. A contract processor serving more than one MLO. C. A mortgage loan originator working for Wells Fargo Bank. D. A mortgage loan originator working for a credit union. Answer: A. This kind of processor, working for a single company and generally paid with a W-2 form, is doing clerical and support work and does not have to have an MLO designation. 16. According to the SAFE Act, which of the following is the best definition of a non- traditional mortgage product: A. An adjustable rate mortgage. B. A mortgage with a term of less than 30 years. C. An open-end mortgage. D. Any mortgage other than 30-year fixed. Answer: D. This is a statement of fact according to the SAFE Act. 17. According to the SAFE Act, which of the following would not have to hold an MLO designation to operate legally: A. A loan originator who does not have to be licensed. B. A real estate broker performing brokerage activity. C. A contract mortgage processor. D. A person who takes a loan application and negotiates terms on a residential loan. Answer: B. A broker performing real estate brokerage activity does not have to have an MLO designation. 18. A registered MLO is an individual who works under the authority of any of the following except: A. A mortgage brokerage company under the authority of the BRE. B. A depository institution. C. An institution regulated by the Farm Credit Administration. D. A subsidiary of a depository institution regulated by a Federal banking agency. Answer: A. MLOs operating under the authority of the BRE must be licensed. 19. The SAFE Act refers to a residential mortgage loan as any loan primarily for the following purpose except: A. Personal use. B. Family use. C. 1-4 owner-occupied use. D. Household use. Answer: C. The SAFE Act does not mention 1-4, owner-occupied. It does refer to these other terms, which would include a trailer that was not even real property.

20. Which of the following statements is most true regarding a state’s use of the unique identifier number: A. Regarded as equally reliable is the individual’s social security number, and the states may use these in lieu of the unique identifier number. B. The social security number is the preferred identifying number and the states are encouraged to use it. C. States must use the unique identifier number in lieu of social security numbers to the greatest extent possible. D. States may use either the social security number or the unique identifier number as assigned by NMLS, whichever in the states’ estimation best accomplishes the purpose of the SAFE Act. Answer: C. This is the mandate of the SAFE Act. 21. What one word best expresses the purpose for having a unique identifier number? A. Liability. B. Accountability. C. Responsibility. D. Compatibility. Answer: B. Yes, the purpose of the unique identifier number is to hold MLOs accountable for the work they do. 22. Which of the following would prevent an individual from being granted an MLO designation: A. Felony assault conviction eight years ago. B. Felony conviction for money laundering 15 years ago. C. Loss of broker’s license with right to restricted salesperson’s license. D. A pardoned felony conviction for fraud. Answer: B. Of this list, only “B” would positively prevent an individual from receiving the MLO designation. 23. According to the SAFE Act, all of the following demonstrate a lack of financial responsibility on the part of an MLO candidate except: A. Outstanding government liens and filings. B. Foreclosures within the past three years. C. Current outstanding judgments. D. The candidate has participated in a short sale as a principal within the past three years. Answer: D. Short sales are more a function of the economy than an individual’s personal behavior and are not mentioned in the SAFE Act. 24. Pre-licensing education requirements for MLO candidates are best expressed as which of the following: A. Eight hours every year. B. Twenty hours to include Federal topics only. C. Twenty hours to include Federal and State-specific topics. D. Eight hours of revolving Federal and State-specific topics.

Thank you for evaluating Wondershare PDF Converter. You can only convert 5 pages with the trial version. To get all the pages converted, you need to purchase the software from: http://cbs.wondershare.com/go.php?pid=755&m=db