Download

1 / 14

140 likes | 538 Views

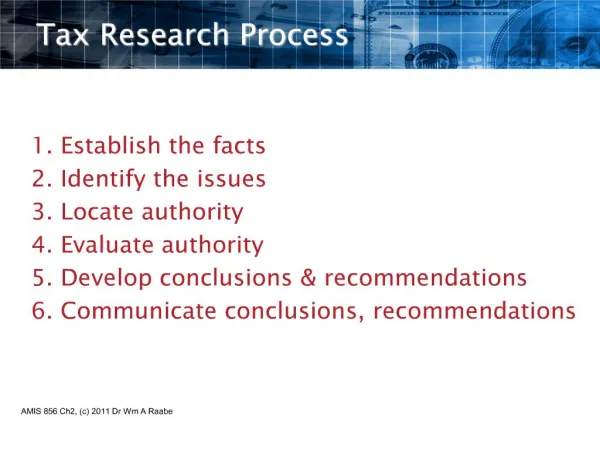

California Tax Research. Cameron L. Hess, CPA Esq. Wagner Kirkman Blaine Klomparens & Youmans LLP Sacramento Walnut Creek chess@wkblaw.com (916) 920-5286. Unique California Issues. Unitary Taxation; Business/Nonbusiness “Doing Business” LLC Fees Combined Reporting Apportionment

E N D

California Tax Research Cameron L. Hess, CPA Esq. Wagner Kirkman Blaine Klomparens & Youmans LLP Sacramento Walnut Creek chess@wkblaw.com (916) 920-5286 CSEA 1082171.pptx C. Hess WKBK&Y

Unique California Issues • Unitary Taxation; Business/Nonbusiness • “Doing Business” • LLC Fees • Combined Reporting • Apportionment • Administrative Appeals • Residency CSEA 1082171.pptx C. Hess WKBK&Y

Why California Can’t Conform • Historical • Budget! • Multi-state issues • Political issues CSEA 1082171.pptx C. Hess WKBK&Y

Understanding FTB Research • Federal Layer • California R&T Code incorporates as of stated dates portions of federal law, but s/t exceptions. • Lots of areas the same – 83(a), 1031, etc. etc. • Note: If California conforms, the FTB will not issue opinions on a particular transaction CSEA 1082171.pptx C. Hess WKBK&Y

Principal One • Understanding state authority is critical; results may differ. California tax law is based on the California Constitution, state laws and state regulations (except where federal law supersedes) CSEA 1082171.pptx C. Hess WKBK&Y

Principal Two • An i) active FTB, ii) independent BOE, iii) California courts means state policy/decisions are critical, especially if: • The issue is controlled by state law • Interpretation of the facts will affect outcome. (Most decisions.) CSEA 1082171.pptx C. Hess WKBK&Y

Principal Three • Question: In practice, the FTB will often conclude differently from the IRS, because: • A. FTB succeeds at a higher % than IRS • B. FTB is more aggressive • C. Taxpayers are less likely to go to court • D. All of the above. CSEA 1082171.pptx C. Hess WKBK&Y

Research – Basic Authorities • California Constitution – Article XIII • Revenue & Taxation Code • Regulations (18 Cal Admin Code) • Cases/Administrative CSEA 1082171.pptx C. Hess WKBK&Y

Where Do I Find These • Free on-line: • www.ftb.ca.gov • www.leginfo.legislature.ca.gov/faces/codes.xhtml • www.law.onecle.com/california/taxation/index.html • www.boe.ca.gov • Pay: • CCH State Tax Reporter – California • Prentice Hall State and Local Tax – California (?) CSEA 1082171.pptx C. Hess WKBK&Y

FTB Guidance • Binding • FTB Notices • FTB Legal Rulings • BOE Decisions (formal opinions) – Rule 40 • Case Law (Unless stated otherwise) CSEA 1082171.pptx C. Hess WKBK&Y

Doing FTB Research • Self-research • FTB Contacts • Divisions. E.g., Withholding at Source Unit • FTB administrative staff, legal staff, etc. • Taxpayer Advocate (Susan Maples) • Public Records Act Request CSEA 1082171.pptx C. Hess WKBK&Y

Doing FTB Research DescriptionIRS Equivalent • FTB Notices IRS Notice • FTB Legal Rulings IRS Rev Rul • Gen’l Counsel Announc’t GCM • Chief Counsel Ruling Private Letter Ruling • TAM TAM • FTB Law Summaries None (white paper?) CSEA 1082171.pptx C. Hess WKBK&Y

BOE Decisions • Formal Decision • R&T Code §40. • Eg. 2015 – Rago Development Corp (§1031) • Summary Decision • Letter Decision CSEA 1082171.pptx C. Hess WKBK&Y

Other Resources • Publications (examples) • Pub 1031 - Residency • Pub 1040 – Nexus; doing business • Pub 81 (BOE) - Appeals • Forms • Form 3705 – Small Penalty/Interest Relief • Form 3520 – Power of Attorney CSEA 1082171.pptx C. Hess WKBK&Y