Download

1 / 43

510 likes | 962 Views

Chapter 4. Present and Future Value. Future Value Present Value Applications IRR Coupon bonds Real vs. nominal interest rates. Present & Future Value. time value of money $100 today vs. $100 in 1 year not indifferent! money earns interest over time, and we prefer consuming today.

E N D

Chapter 4. Present and Future Value • Future Value • Present Value • Applications • IRR • Coupon bonds • Real vs. nominal interest rates

Present & Future Value • time value of money • $100 today vs. $100 in 1 year • not indifferent! • money earns interest over time, • and we prefer consuming today

example: future value (FV) • $100 today • interest rate 5% annually • at end of 1 year: 100 + (100 x .05) = 100(1.05) = $105 • at end of 2 years: 100 + (1.05)2 = $110.25

future value • of $100 in n years if annual interest rate is i: = $100(1 + i)n • with FV, we compound cash flow today to the future

Rule of 72 • how long for $100 to double to $200? • approx. 72/i • at 5%, $100 will double in • 72/5 = 14.4 • $100(1+i)14.4 = $201.9

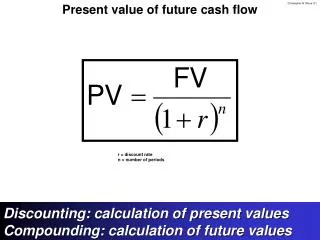

present value (PV) • work backwards • if get $100 in n years, what is that worth today? $100 PV = (1+ i)n

example • receive $100 in 3 years • i = 5% • what is PV? $100 PV = = $86.36 (1+ .05)3

With PV, we discount future cash flows • Payment we wait for are worth LESS

About i • i = interest rate • = discount rate • = yield • annual basis

n PV PV i

PV, FV and i • given PV, FV, calculate I example: • CD • initial investment $1000 • end of 5 years $1400 • what is i?

is it 40%? • is 40%/5 = 8%? • No…. • i solves i = 6.96%

Applications • Internal rate of return (IRR) • Coupon Bond

Application 1: IRR • Interest rate • Where PV of cash flows = cost • Used to evaluate investments • Compare IRR to cost of capital

Example • Computer course • $1800 cost • Bonus over the next 5 years of $500/yr. • We want to know i where PV bonus = $1800

Solve for i? Trial & error Spreadsheet Online calc. Answer? 12.05% Solve the following:

Example • Bonus: 700, 600, 500, 400, 300 • Solve i = 14.16%

Example • Bonus: 300, 400, 500, 600, 700 • Solve i = 10.44%

Example: annuity vs. lump sum • choice: • $10,000 today • $4,000/yr. for 3 years • which one? • implied discount rate?

Application 2: Coupon Bond • purchase price, P • promised of a series of payments until maturity • face value at maturity, F (principal, par value) • coupon payments (6 months)

size of coupon payment • annual coupon rate • face value • 6 mo. pmt. = (coupon rate x F)/2

what determines the price? • size, timing & certainty of promised payments • assume certainty P = PV of payments

i where P = PV(pmts.) is known as the yield to maturity (YTM)

example: coupon bond • 2 year Tnote, F = $10,000 • coupon rate 6% • price of $9750 • what are interest payments? (.06)($10,000)(.5) = $300 • every 6 mos.

what are the payments? • 6 mos. $300 • 1 year $300 • 1.5 yrs. $300 ….. • 2 yrs. $300 + $10,000 • a total of 4 semi-annual pmts.

YTM solves the equation • i/2 is 6-month discount rate • i is yield to maturity

how to solve for i? • trial-and-error • bond table* • financial calculator • spreadsheet

price between $9816 & $9726 • YTM is between 7% and 7.5% (7.37%)

P, F and YTM • P = F then YTM = coupon rate • P < F then YTM > coupon rate • bond sells at a discount • P > F then YTM < coupon rate • bond sells at a premium

P and YTM move in opposite directions • interest rates and value of debt securities move in opposite directions • if rates rise, bond prices fall • if rates fall, bond prices rise

YTM rises from 6 to 8% • bond prices fall • but 10-year bond price falls the most • Prices are more volatile for longer maturities • long-term bonds have greater interest rate risk

Why? • long-term bonds “lock in” a coupon rate for a longer time • if interest rates rise -- stuck with a below-market coupon rate • if interest rates fall -- receiving an above-market coupon rate

Real vs. Nominal Interest Rates • thusfar we have calculated nominal interest rates • ignores effects of rising inflation • inflation affects purchasing power of future payments

example • $100,000 mortgage • 6% fixed, 30 years • $600 monthly pmt. • at 2% annual inflation, by 2037 • $600 would buy about half as much as it does today $600/(1.02)30 = $331

so interest charged by a lender reflects the loss due to inflation over the life of the loan

real interest rate, ir nominal interest rate = i expected inflation rate = πe approximately: i = ir + πe • The Fisher equation or ir = i – πe [exactly: (1+i) = (1+ir)(1+ πe )]

real interest rates measure true cost of borrowing • why? • as inflation rises, real value of loan payments falls, • so real cost of borrowing falls

inflation and i • if inflation is high… • lenders demand higher nominal rate, especially for long term loans • long-term i depends A LOT on inflation expectations