Download

1 / 35

440 likes | 757 Views

Inventories: IAS 2. JOIN KHALID AZIZ ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM. FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MBA & PIPFA. COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA. CONTACT: 0322-3385752

E N D

JOIN KHALID AZIZ • ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM. • FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MBA & PIPFA. • COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA. • CONTACT: • 0322-3385752 • R-1173,ALNOOR SOCIETY, BLOCK 19,F.B.AREA, KARACHI, PAKISTAN.

Inventories Related standards IAS 2 Current GAAP comparisons IFRS financial statement disclosures Looking ahead End-of-chapter practice

Related Standards HB 3031 Inventories

Related Standards FAS 151 Inventory costs—an amendment of ARB 43 ARB 43 Inventories

Related Standards IAS 11 Construction contracts IAS 32 Financial instruments: presentation IAS 39 Financial instruments: recognition and measurement IAS 41 Agriculture

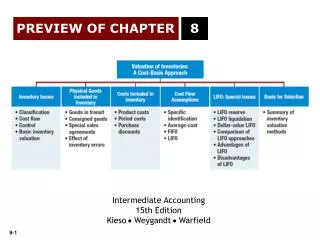

IAS 2 - Overview Objective and scope Measurement Expense recognition Disclosure

IAS 2 - Objective and Scope Standards for what costs are recognized as inventory costs and when these costs are transferred to the income statement as expense IAS 2 excludes construction work-in-progress, inventories of financial instruments, and biological inventory assets related to agricultural activity and agricultural products at the point of harvest

IAS 2 - Objective and Scope Inventories are assets: held for sale in the ordinary course of business in the process of production for such sale, or in the form of materials or supplies to be consumed in the production process or in the rendering of services

IAS 2 - Measurement Inventories are measured at the lower of cost and net realizable value (LC and NRV) Need to know: - what costs are included - what cost formulas are permitted - how net realizable value is determined

IAS 2 - Measurement Costs included: Purchase costs Conversion costs Other inventoriable costs

IAS 2 - Measurement Purchase costs - purchase price and all costs directly attributable to their acquisition such as non-refundable taxes, transportation and handling, reduced by volume discounts and rebates

IAS 2 - Measurement Conversion costs - direct labour, indirect variable and fixed production overhead costs - variable production overhead: allocate to inventory based on actual usage - fixed production overhead: allocate to production based on normal operating capacity (except when abnormally high production)

IAS 2 - Measurement Joint products Allocate between products on a rational basis such as relative sales value of products when they become separable If minor in value, do not allocate: measure by-product at net realizable value and deduct this amount from main product costs

IAS 2 - Measurement Other inventoriable costs - limited to costs to bring the inventories to their present location and condition - example: amortization of capitalized development costs related to inventory - borrowing costs included if for a qualifying inventory item (if measured at FV or produced in large volumes on a repetitive basis, borrowing costs may, but are not required to be capitalized)

IAS 2 - Measurement Do not add to inventory cost: Costs of abnormal waste Storage or warehousing costs unless necessary for next stage of production Administrative overheads not associated with production Selling costs Financing charges above purchase price for normal credit terms

IAS 2 - Measurement Cost formulas permitted should: Assign recent costs to ending inventory Correspond closely with the actual physical flow of the goods and services Three permitted: Specific identification, First-in, first-out, and weighted average

IAS 2 - Measurement Specific identification: For inventory items that are not ordinarily interchangeable For goods and services produced and segregated for specific projects

IAS 2 - Measurement FIFO and weighted average: FIFO – cost of latest purchases ends up in cost of ending inventory, cost of earliest purchases are in cost of goods sold Weighted average – weighted average cost of all goods available for sale ends up in both ending inventory and cost of goods sold

IAS 2 - Measurement KPMG : The Application of IFRS: Choices in Practice – International Financial Reporting Standards, December 2006 Results indicate that the usage of the FIFO and weighted average methods are fairly evenly split by companies reporting under IFRS

JOIN KHALID AZIZ • ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM. • FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MBA & PIPFA. • COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA. • CONTACT: • 0322-3385752 • R-1173,ALNOOR SOCIETY, BLOCK 19,F.B.AREA, KARACHI, PAKISTAN.

IAS 2 - Measurement Inventories reported at the LC and NRV Why? So not reported at more than the future cash flows into the company from their sale NRV = the estimated selling price in the ordinary course of business less the estimated costs of completion and the estimated costs to make the sale

IAS 2 - Measurement LC and NRV example: Cost Rs 80 Selling price Rs 84 Cost to complete Rs 5 Cost to sell 10% of SP NRV: Rs84 - Rs5 - Rs8.40 = Rs70.60 LC and NRV = Rs70.60

IAS 2 - Measurement Write-downs are recognized in profit or loss. Subsequent write-ups permitted to maximum of prior write-downs if: - changed economic circumstances and NRV has increased, prior situation no longer exists Reversals also taken to profit or loss

IAS 2 – Expense Recognition Carrying amount of inventory sold is expense in same period as the related revenue Inventory adjustments (losses, write-downs to lower of cost and NRV, write-down reversals, etc.) are recognized as an adjustment to the expense recognized in the period

IAS 2 - Disclosure Disclosures needed for: Accounting policies applied Inventory remaining on statement of financial position Inventory costs recognized in profit or loss

IAS 2 - Disclosure Balance-sheet related disclosures: Carrying amount in each category of inventory (materials, WIP, finished goods, production supplies, merchandise) and in total Carrying amount of any inventory measured at fair value less costs to sell Carrying amount of inventory pledged as collateral for liabilities

IAS 2 - Disclosure Income statement-related disclosures: Amount of inventory recognized as an expense (usually cost of sales/cost of goods sold) Amount of write-downs to NRV or other losses Amount of any write-down reversals Circumstances that resulted in reversals

Looking Ahead There is nothing on the IASB’s current agenda that directly involves potential changes to IAS 2 Inventories

JOIN KHALID AZIZ • ECONOMICS OF ICMAP, ICAP, MA-ECONOMICS, B.COM. • FINANCIAL ACCOUNTING OF ICMAP STAGE 1,3,4 ICAP MODULE B, B.COM, BBA, MBA & PIPFA. • COST ACCOUNTING OF ICMAP STAGE 2,3 ICAP MODULE D, BBA, MBA & PIPFA. • CONTACT: • 0322-3385752 • R-1173,ALNOOR SOCIETY, BLOCK 19,F.B.AREA, KARACHI, PAKISTAN.