Download

1 / 35

350 likes | 421 Views

VA Loans for Vets NMLS#184169<br>5050 North 40th Street, Ste 260<br>Phoenix, AZ 85018<br>602-908-5849<br><br>Jimmy Vercellino is one of the nationu2019s top VA Home Loan mortgage originators. A Marine veteran, he and his team work hard to help veterans take advantage of their VA loan benefit and become homeowners. From start to finish, they guide their clients through the process and make it as smooth and stress-free as possible. Visit the site at https://www.valoansforvets.com

E N D

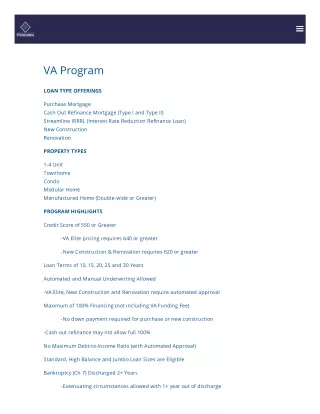

WHEN DO I NEED A JUMBO VA LOAN?

As a veteran, you may be eligible for certain housing benefits that are administered by the United States Department of Veterans Affairs (VA).

In 1930, the VA was established in order to aggregate all of the military home loan programs into one.

Learn about when you may need a special mortgage called the “Jumbo VA Loan.”

VETERANS ADMINISTRATION BENEFITS

The “Serviceman’s Readjustment Act” of 1944 (the G.I. Bill) was passed by the United States Congress to help returning soldiers acclimate into civilian life.

The normal VA mortgages will vary by term, interest rate type and focus (i.e. Energy Efficiency).

Veterans can use Energy Efficiency mortgages to pay for caulking, water heaters and solar panels.

Generally, the VA guarantees a certain percentage of the price of your home purchase.

First you find a property and then you visit a VA office to see what percentage of the price will be backed by the government.

Many VA mortgages will also allow you to purchase a home without the normal 20% down payment.

Usually, the government will not provide the actual money but acts as an insurance agency guaranteeing a portion of your loan.

The VA sets an eligibility entitlement based on the average cost for an American house.

Of course, you might want to purchase a home that is more expensive than this average. Homes above this average require Jumbo VA Loans.

In many ways, the primary mission for this housing benefit is to ensure that you have a roof over your head.

The more expensive houses are primarily luxury goods and are a separate category.

Unlike the normal loan package, you will be responsible for paying a higher percentage of the Jumbo housing cost above the base. The government may offer fewer guarantees for these types of loans.

There are three primary VA Jumbo loans, which all have a 30 Year Fixed Interest Rate: Normal Energy Efficient Investor Specific

Here are some of the eligibility requirements: Owner occupied only. Minimum service time. Honorable discharge.

No bankruptcy in previous seven years. Manufactured (mobile) homes are not eligible.

There are different minimum lengths of service based on war or peacetime.

There are restrictions on certain geographical areas where the VA mortgage cannot be used. So, does the county where your home is located matter? Yes.

The VA will establish an entitlement amount for each eligible veteran. Then, lenders will loan up to 4 times that entitlement amount.

The VA has designated approximately 146 x High Cost Counties in the United States where the maximum limit exceeds the guarantee.

These High Cost or High End Counties require a Jumbo Loan.

The VA Jumbo Loan works as follows: Borrower does not place any money down on VA county limit. Borrower pays a 25% down payment for amount above VA county limit.

Borrower pays funding fee in cash for any loan between VA county limit and $1,000,000. For loan amounts greater than $417,000, the homeowner maintains all program benefits.

Mortgage Originator Jimmy Vercellino, specializing in VA loans, helps veterans use their VA loan benefit to their greatest advantage.

For more details call 480-351-5904. Visit the site at https://www.valoansforvets.com/va-loan-eligibility/

VA LOANS FOR VETS 7702 E. Doubletree Ranch Road, Suite 220 Scottsdale, AZ 85258 Phone: (480) 351-5904 Email: jimmyv@fcbmtg.com