Download

1 / 37

370 likes | 517 Views

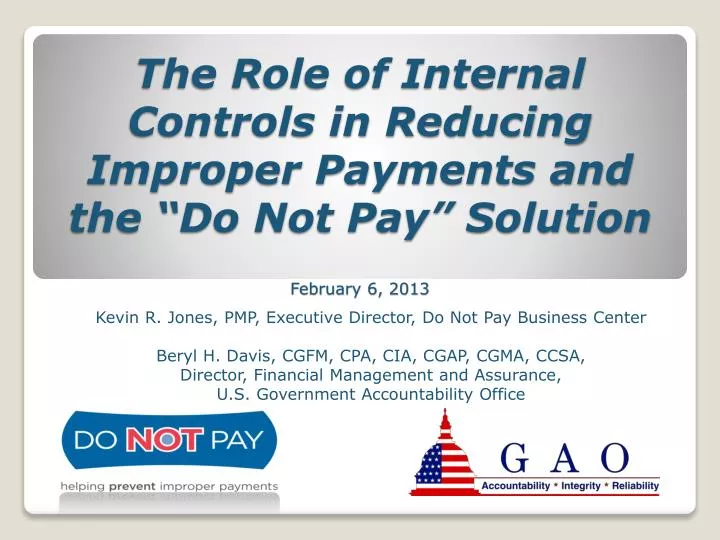

The Role of Internal Controls in Reducing Improper Payments and the “Do Not Pay” Solution February 6, 2013. Kevin R. Jones, PMP, Executive Director, Do Not Pay Business Center Beryl H. Davis, CGFM, CPA, CIA, CGAP, CGMA, CCSA, Director, Financial Management and Assurance,

E N D

The Role of Internal Controls in Reducing Improper Payments and the “Do Not Pay” SolutionFebruary 6, 2013 Kevin R. Jones, PMP, Executive Director, Do Not Pay Business Center Beryl H. Davis, CGFM, CPA, CIA, CGAP, CGMA, CCSA, Director, Financial Management and Assurance, U.S. Government Accountability Office

Improper payments definition and causes • Laws and authoritative guidance • Fiscal Year 2012 improper payment estimates • Using Internal Controls to Reduce Improper Payments • The “Do Not Pay” Solution Discussion Points

An improper payment is any payment that should not have been made or was made in an incorrect amount (including overpayments and underpayments). • For example, improper payments include: • duplicate payments to a contractor; • payment to an ineligible recipient; and • incorrect payment amount paid to a beneficiary. • OMB guidance also instructs agencies to report as improper payments any payments for which insufficient or no documentation was found. What Are Improper Payments?

The entire amount of a duplicate or unsupported payment is considered an improper payment. • Only the difference between the correct payment amount and the amount paid is considered an improper payment when the payment amount was incorrect. • Improper payment estimates reported by federal agencies are not intended to be an estimate of fraud in federal agencies’ programs and activities. What Are Improper Payments?

There are many root causes for improper payments. The Office of Management and Budget has grouped the causes into 3 error categories: • Documentation and administrative: • Inputting, classifying, or processing errors • Lack of supporting documentation • Authentication and medical necessity: • Inability to authenticate eligibility criteria • Providing a service not medically necessary given patient’s condition • Verification: • Failure or inability to verify information such as earnings, income, assets, or work status • Beneficiaries’ failure to report correct information Causes of Improper Payments

The latest in a series of laws addressing federal improper payments, following the Improper Payments Information Act of 2002 (IPIA) and Improper Payments Elimination and Recovery Act of 2010 (IPERA) • Signed into law on January 10, 2013 Improper Payments Elimination and Recovery Improvement Act of 2012 (IPERIA)

Improper Payments Elimination and Recovery Improvement Act of 2012 (IPERIA) • Among other things, this law: • Amends IPIA to require OMB to annually designate a list of “high-priority programs,” which will be subject to additional reporting requirements and oversight by agency Inspectors General; • Gives statutory authority for the Do Not Pay Initiative; • Clarifies that payments to federal employees are subject to IPIA risk assessment and, where appropriate, improper payment estimation; • Requires agencies to include all identified improper payments in the reported estimate, regardless of whether the improper payment in question has been or is being recovered; and • Requires OMB to determine current and historical rates of recovery of improper payments, as well as targets for improper payment recovery.

The Office of Management and Budget (OMB) plays a key role in the oversight of the governmentwide improper payments problem. • OMB has established guidance for federal agencies on reporting, reducing, and recovering improper payments. • OMB issued its implementing IPERA guidance on April 14, 2011 – Parts I and II, Appendix C of OMB Circular A-123. • OMB listed reducing improper payments as one of 14 cross-cutting goals under the GPRA Modernization Act. Office of Management and Budget’s Role in Managing Improper Payments

As part of the Accountable Government Initiative, the President set a goal of reducing improper payments by a minimum of $50 billion and recovering $2 billion in overpayments to contractors and vendors between fiscal years 2010 and 2012. • Per OMB, agencies reported recapturing $2.4 billion in improper payments to contractors and vendors in FY2012, almost twice as much as was captured in FY2011. Administration’s Goals for Reducing and Recovering Improper Payments

OMB and the federal agencies reported improper payment estimates totaling $107.7 billion in fiscal year 2012, a decrease of $8.0 billion from the prior year revised estimate of $115.7 billion. • The $107.7 billion in estimated federal improper payments reported for fiscal year 2012 was attributable to 75 programs across 18 agencies. • The 5 programs with the highest dollar estimates accounted for about $84.8 billion, or 79% of the total estimated improper payments agencies reported for fiscal year 2012. • The 5 highest error rates reported for fiscal year 2012 ranged from 12.0% to 25.2%. Fiscal Year 2012 Improper Payment Estimates

All Other Programs 21% Medicare Fee-for-Service, 27% Unemployment Insurance 10% Medicaid 18% Earned Income Tax Credit 12% Percentage Distribution of Improper Payments FY 2012 Medicare Advantage (Part C) 12%

The estimated decrease in fiscal year 2012 is attributed primarily to 4 major programs: • Decreases in program outlays for Labor’s Unemployment Insurance program and Treasury’s Earned Income Tax Credit Program, and • Decreases in error rates for Health and Human Services’ Medicaid and SSA’s Old-Age, Survivors, and Disability Insurance programs. • The fiscal year 2012 governmentwide error rate decreased to 4.4% of outlays from 4.7% percent in fiscal year 2011. Fiscal Year 2012 Improper Payment Estimates

Fiscal Year 2012 Top 5 Improper Payment Estimates by Dollar Amount

Medicare Fee-for-Service –Insufficient documentation, medically unnecessary services, and incorrect coding. • Medicaid – Eligibility and pricing errors, non-covered services, insufficient documentation, policy violation, and diagnosis and procedure coding errors. • Medicare Advantage – Insufficient documentation, transfer of data, and interpretation of data and payment calculations. • Earned Income Tax Credit – Inability to authenticate qualifying child eligibility requirements and under/overreporting of income. • Unemployment Insurance – Individuals claim benefits after returning to work, verification errors not detectable by agency procedures, and agency failing to resolve issues properly. Fiscal Year 2012 Reported Improper Payment Root Causes – Top 5 by Amount

Fiscal Year 2012 Top 5 Improper Payment Estimates by Error Rate

School Breakfast – School misclassification of meal eligibility status of participating students and improper meal counting and claiming by schools. • Earned Income Tax Credit – Inability to authenticate qualifying child eligibility requirements and under/overreporting of income. • Disaster Assistance Loans – Processing and disbursement staff not following guidance provided in SOP and policy memos. • National School Lunch – School misclassification of meal eligibility status of participating students and improper meal counting and claiming by schools. • Non-VA Care Fee – Incorrect application of payment methodologies and use of an incorrect payment schedule, incomplete or missing clinical authorization documentation, and data entry, invoicing, and coding errors. Fiscal Year 2012 Reported Improper Payment Root Causes – Top 5 by Rate

10 risk-susceptible programs/activities did not report improper payment estimates for FY2012: • GSA’s Building Operations – Utilities • GSA’s Integrated Technology Services – WAN • GSA’s Other Sensitive Payments • GSA’s Purchase Cards • GSA’s Rental of Space • HHS’s Temporary Assistance to Needy Families (TANF) • USDA’s Loan Deficiency • USDA’s Milk Income Loss • VA’s Other Contractual Services • VA’s Prosthetics Not All Susceptible Programs Report Improper Payment Estimates

Not All Improper Payment Estimates Are Reported • Estimates reported for 6 programs were not included in OMB’s FY2012 governmentwide estimate because the estimation methodologies were not OMB-approved: • DOD’s U.S. Army Corps of Engineers Commercial Pay • DOT’s Federal Railroad Administration’s High-Speed Intercity Passenger Rail • Education’s Direct Loan • Education’s Federal Family Education Loan • RRB’s Railroad Unemployment Insurance Program • VA’s Beneficiary Travel • Additionally, DOD’s DFAS Commercial Pay was not included in the governmentwide estimate for the sake of comparison to FY2009-2011 figures.

Current actions under way across government and future initiatives will be needed to effectively reduce improper payments in the federal government. Strategies include: • Identifying the root causes of improper payments. • Developing effective preventive controls to avoid improper payments in the first place. Moving Forward with Improper Payment Reduction Strategies

Identifying the Root Cause to Implement Internal Controls • Information on the root causes of improper payments is necessary for agencies to target effective corrective actions and implement preventive measures. • Of the 75 programs reporting fiscal year 2012 improper payment estimates, 58 reported the root cause information required by OMB. • These 58 programs represented about $105.7 billion, or 98%, of the total reported $107.7 billion in improper payment estimates for fiscal year 2012.

Increased focus on identifying and analyzing root causes will be key to moving to the next phase of reducing and eliminating improper payments at a governmentwide level. • Because the 3 categories established by OMB are general, additional analysis is critical to understanding the root causes. • Estimates and measurements could be refined to more discreetly identify the nature of the problem so that specific corrective actions can be designed to address specific causes. Identifying the Root Causes of Improper Payments

Many agencies and programs are in the process of implementing preventive controls to eliminate improper payments, including overpayments and underpayments. • Effective preventive controls also help avoid the difficulties of the “pay and chase” aspects of recovering overpayments by preventing the improper payment in the first place. Using Preventive Controls to Eliminate Improper Payments

Examples of preventive controls include: • Upfront eligibility validation through data sharing – When effectively implemented, data sharing can be particularly useful in confirming initial or continuing eligibility of participants in benefit programs and identifying improper payments already made. • Predictive analytic technologies – CMS is using predictive analytic technologies to analyze and identify Medicare provider networks, billing patterns, and beneficiary utilization patterns and detect those that represent a high risk of fraudulent activity. Using Preventive Controls to Eliminate Improper Payments

Training programs for providers, staff, and beneficiaries – Training can include both training staff on how to prevent and detect improper payments and training providers or beneficiaries on program requirements. • Timely resolution of audit findings – According to Standards for Internal Control in the Federal Government, managers are to evaluate audit findings, determine proper action in response to findings and recommendations, and complete all actions that correct or resolve the issues within established time frames. • Program design review and refinement – Exploring whether certain complex or inconsistent program requirements contribute to improper payments would lend insight to developing effective strategies for enhancing compliance and may identify opportunities for streamlining or changing eligibility or other program requirements. Using Preventive Controls to Eliminate Improper Payments

Internal Revenue Service: • According to IRS, it has increasingly prevented identity theft-based refund claims by identifying fraudulent returns, resulting in the following savings: • FY2010: 40,000 returns, $470M savings • FY2011: 1,100,000 returns, $8B savings • FY2012 (first 9 months): 1,400,000 returns, $9.3B savings • IRS has also enhanced its Questionable Refund Program, which screens tax returns for suspicious activity. Examples of Preventive Controls to Prevent Improper Payments

HHS’ CMS: • Reported $1.76 billion of savings in FY2010 from the use of prepayment edits. • Increased savings could have been reported had prepayment edits been more widely used. • Additionally, GAO identified $14.7 million of payments from FY2010 that appeared to be inconsistent with select Medicare policies and could have been at least partially prevented by prepayment edits. Examples of Preventive Controls to Prevent Improper Payments

More needs to be done to safeguard taxpayer dollars against improper payments. • Effective “preventive” internal controls are needed to prevent improper payments in the first place. Keep Pushing Forward

Do Not Pay Portal Data Analytics Services • Provides users with an internet-based single entry point for multiple data sources. Users can search via: • Online • Batch Matching • Continuous Monitoring • Provides agencies with additional customized analysis to combat improper payments • General Statistics • Trending –Observing how data changes over time. • Deep Dive Analysis – Performing further research on specific groups, individuals, or entities. • Agency Specific Analysis • Payment File Analysis Do Not Pay Components Agency Support Center Supports users for both services in all aspects of the process. Also, provides personalized training and portal demonstrations.

User submits data for entities receiving payments or being monitored & receives matching results. Online, batch matching, and continuous monitoring are supported within the Portal. User submits data for entities under consideration & receives matching results. Online, batch matching, and continuous monitoring are supported within the Portal. Use within Agency’s Business Process Data Analytics Services staff analyze the data and trends and provide reports to support agency investigation and recovery efforts.

Data Sources of Potential Interest • DMF Private* [SSA] • Credit Alert Verification Reporting System (CAIVRS) maintained by the U.S. Department of Housing & Urban Development • National Directory of New Hires maintained by HHS Prisoner data maintained by SSA and the Department of Justice’s Federal Bureau of Prisons • GSA’s System for Award Management (SAM) • Potential sources for death data: • legacy.com, The Last One • Potential sources for income/employment/debt data: • HHS’s Public Assistance Reporting Information System (PARIS, also has criminal data), State Information Data Exchange System (SIDES), Verify Direct, Verify Job, HHS’s Federal Case Registry (child support enforcement), IRS’s Dependent Database (DDb) • Potential source for government contract data: • GSA’s Federal Awardee Performance and Integrity Information System (FAPIIS) • Potential source for prisoner data: • Prisoner Update Processing Systems (PUPS) • Potential source for excluded parties data: • Traveler Enforcement Compliance System (TECS) • Data Sources Currently Available • Excluded Party List System (EPLS) Public and Private* with an Office of Foreign Asset Controls (OFAC) feed [GSA] • individuals and firms excluded from receiving new federal contracts; and individuals and companies owned or controlled by targeted countries, and individuals, groups, and entities, such as terrorists and narcotics traffickers • Central Contractor Registration (CCR) [GSA] • primary vendor database of both current and potential government vendors • List of Excluded Individuals/Entities Public (LEIE) [HHS] • individuals and entities currently excluded from participation in federal healthcare programs, such as Medicare and Medicaid • Death Master File Public (DMF) Public [SSA] • a listing of deaths that have been reported by the Social Security Administration • Debt Check* [FMS] • delinquent child support and non-tax debt owed to the federal government • The Work Number [commercial source] • employment and income information for individuals Data Sources * Privacy Act restricted

Analysis on the DNP file completed with conclusive, probable and possible matches Based on information learned, determine if payment should be paid. 1 8 Ensure alignment with existing process and mission of the organization Notification email sent to log in and view results in the DNP Portal 7 2 Uncertainty about how to proceed begins 6 3 Investigate further, confirm matches & document decision Prioritize the critical matches for your agency 5 4 Review and TAKE ACTION on your DNP “hits” Research the internal business rules that apply to your data Apply the rules that are applicable to each of the data sources

IPERIA assigns all requirements to OMB and Executive Agencies • OMB has asked Treasury to persist the DNP program • OMB will issue guidance • Key provisions/implications: • Review all payments and awards through Do Not Pay • Speed up Computer Matching Agreement processes (no change to Privacy Act) • OMB likely to request agency input for reporting Improper Payment Elimination and Recovery Improvement Act of 2012 Note: these bullets pertain only to Section 5 (the DNP section) of IPERIA

Oct. 2011 • Aug. 2011 2011 Timeline Received Direction to Establish DAS by October 2011 and Commenced Portal Development Portal Project Kick-Off Initial Portal Release DAS Operational We’ve come a long way, fast

in planning: • insertion of DNP into Treasury payment stream • long-term infrastructure • function, function, function • analytics, analytics, analytics Where we’re headed

1-855-837-4391 Get More Information Want to Learn More? Reach out to the Agency Support Center to find the services that best fit your agency’s needs. Sign up for our mailing list to receive updates on new functionality and data sources or to schedule a demo. Contact the Agency Support Center or visit us at www.donotpay.treas.gov donotpay@stls.frb.org