Download

1 / 18

180 likes | 268 Views

Dynamic Decision Making when Risk Perception depends on Past Experience. Michèle COHEN, CES, Université de Paris 1 Johanna ETNER, GAINS, Univ. du Maine et CES, Paris 1 Meglena JELEVA, GAINS, Univ. du Maine et CES, Paris 1. Introduction Behavior at a point of time Dynamic choice

E N D

Dynamic Decision Making when Risk Perception depends on Past Experience Michèle COHEN, CES, Université de Paris 1 Johanna ETNER, GAINS, Univ. du Maine et CES, Paris 1 Meglena JELEVA, GAINS, Univ. du Maine et CES, Paris 1

Introduction • Behavior at a point of time • Dynamic choice • An illustrative example: past experience and insurance demand FUR XII, Rome 2006

1. Introduction (1/3) • Risk and wealth perception may be influenced by the agent context when he takes his decisions • Context = framing, past experience, feelings etc. • In this paper: focus on past experience • Some empirical evidence: • Relation between insurance decisions and individual prior-experience related to risk: • Kunreuther (1996), Brown, Hoyt (2000); • Weather conditions influence investment decisions: • Hirshleifer, Shumway (2003) FUR XII, Rome 2006

1. Introduction (2/3) • Past experience can concern different events: • Past realizations on the decision-relevant events (accidents); • Realizations of events, independant on the relevant decision problem (weather). • To better capture the long term impact of past experience, we model intertemporal decisions. • A first step consists in considering a one period decision problem where preferences are defined on pairs (decision, past experience); FUR XII, Rome 2006

1. Introduction (3/3) • We adapt RDU axiomatic system of Chateauneuf (1999); • The obtained criterion is used in the construction of a dynamic choice model under risk; • We model intertemporal decisions by a recursive model à la Kreps, Porteus (1978). FUR XII, Rome 2006

2. Behavior at a point of time (1/4) • Decision problem characterized by: • L: set of lotteries over Z R; • S: set of past (realized) states; • (s , L): « past experience dependent lottery »; • : preference relation on S L. FUR XII, Rome 2006

2. Behavior at a point of time (2/4) • Preferences representation on S L in 3 steps: • for any fixed s, s on s L, from Chateauneuf (1999): • S Z on S Z, axioms to guarantee the existence of a utility function on S Z. • Additional axioms to guarantee the consistency of the conditional preference relations. FUR XII, Rome 2006

2. Behavior at a point of time (3/4) • Theorem on S L is representable by a function V: FUR XII, Rome 2006

2. Behavior at a point of time (4/4) • Some particular cases: • Realized states influence only the probability transformation function: • Realized states influence only the utility function: FUR XII, Rome 2006

3. Dynamic choice (1/5) • In the spirit of Kreps, Porteus modelling • Some notations and assumptions: • T periods; • Zt = Z R; • Past experience at time t: st = (e0, e1,…,et) with et Et; • St : set of possible past experiences up to time t such that: S0 = E0 and St = St-1 Et; • M(Et): set of distributions on Et. FUR XII, Rome 2006

3. Dynamic choice (2/5) • At period T, • LT: set of distributions on ZT ; • XT: set of closed non empty subsets of LT. • Recursively, • Lt: set of probability distributions on Ct = Zt Xt+1M(Et+1), with Xt+1 the set of closed non empty subsets of Lt+1. FUR XII, Rome 2006

3. Dynamic choice (3/5) • For the same period, assumption of compound lotteries reduction (ROCL) is made between distributions of wealth and events. • Between two consecutive periods, ROCL remains relaxed. FUR XII, Rome 2006

3. Dynamic choice (4/5) • For each period t, t on st Lt, for a given st represented by: • Temporal consistency axiom For any t, s t, et+1,zt, xt+1, x’t+1, FUR XII, Rome 2006

3. Dynamic choice (5/5) • Representation theorem There exist 2 sequences of utilities ut and vt and a sequence of t such that: FUR XII, Rome 2006

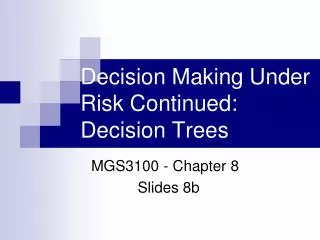

4. An illustrative exemple (1/4) • Insurance demand • An individual faces a risk of loss and has to choose an amount of insurance coverage, ; • Insurance contracts are subscribed for one period (year) • Risk characteristics: • loss of an amount L with probability p; • P(loss in period t/ loss in period t-1) = p FUR XII, Rome 2006

4. An illustrative exemple (2/4) • Optimal insurance strategy of an individual for 3 periods of time? • Insurance contracts: subscibed for 1 year, fair premium • Past experience at t: sequence of loss realizations before t et= e if « loss at period t », et= e’ if « no loss at period t » st = (st-1, et) FUR XII, Rome 2006

L3 z3 a3 z2 p 1-p z3 z1 L2 a2 s2=(e0,e1,e2) p z’3 z2 L’3 a’3 p s1=(e0,e1) 1-p 1-p z’3 s’2=(e0,e1,e’2) L1 z0 a1 p z’’3 z’2 L’’3 s0=e0 a’’3 p 1-p L’2 s’’2=(e0,e’1,e2) 1-p z’’3 z1 a’2 z’’’3 p z’2 L’’’3 s’1=(e0,e’1) a’’’3 1-p s’’’2=(e0,e’1,e’2) z’’’3 1-p 4. An illustrative exemple (3/4) p FUR XII, Rome 2006

4. An illustrative exemple (4/4) • Let • Results: • 1 = 0; • 2 = 0 if no loss at period 1; 2 [0, 1] if loss at period 1; • 3 = 0 if no loss at periods 1 and 2; 3 = 1 if loss at periods 1 and 2; 3 [0, 1] else. FUR XII, Rome 2006