Download

1 / 16

170 likes | 407 Views

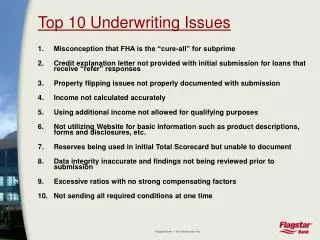

Texas Wide Underwriting Conference Current Issues in Underwriting. Bob Cicchi Scott Marquis Pete Morris April 5, 2011. Industry Underwriting Topics. Simplified Issue Decision Engines Rx Database Database Mining Younger Markets Measuring Underwriter Performance Remote Underwriting

E N D

Texas Wide Underwriting ConferenceCurrent Issues in Underwriting Bob Cicchi Scott Marquis Pete Morris April 5, 2011

Industry Underwriting Topics • Simplified Issue • Decision Engines • Rx Database • Database Mining • Younger Markets • Measuring Underwriter Performance • Remote Underwriting • Future Prospects

Industry Trends • Simplified Issue • AHOU in San Antonio last year just about every vendor pitching a SI platform. • Face amounts are getting larger: up to $500,000 • Ages are getting older: up to age 65 • Technology is getting better: web based platforms

Industry Trends • Decision Engines • AHOU meeting multiple decision engines • Sophistication is getting better; engines incorporate data from several sources • Rx data, MIB, MVR, and other data run through decision algorithm to render an underwriting decision. • Reinsurers appear to have bought into these engines

Industry Trends • Rx Database • More and more companies adapting • Some carriers using Rx in segments of their business; others run all their business through it • Rx vendors now offering more sophisticated solutions that assist underwriters in identifying high risk Rx patterns • Rx is at core of many of the decision engines now hitting the market • Legislation is a concern

Industry Trends Database Mining Is it possible to move away from fluids and the APS? Database mining may offer the first glimpse into our future without fluids and doctor reports What you eat, what you buy, how you spend your leisure time, which websites you visit, how often you go to the doctor, etc, is ALL available in databases The challenge is tying all that data into a product that will sell, minimize anti-selection and be profitable for the insurance companies I wouldn’t bet against it!

Industry Trends • Move away from the mature market to younger Middle Market applicants • Speed and ease of purchase are key to successfully penetrating this market segment • Educational tools and online resources help tap into younger buyers • Companies rapidly embracing online community as fertile ground to build brand loyalty with Gen X and Gen Y market segments

Remote Underwriting • Economic downturn resulted in the loss of many underwriting positions, including some remote underwriters • This seems to have stabilized. • Future will see an expansion remote positions

The Verdict on Remote Underwriting • Helps companies reduce turnover rates. • Companies are able to attract experienced, quality underwriters • Most studies have reported increased production in remote underwriters and increased job satisfaction. • Senior Management has seen the benefit of remote underwriting and has developed a good level of comfort with the concept. • Bottom line: Remote underwriting has been successful and is here to stay.

Future Prospects for the Underwriting Profession • In the short term (2-5 years), we should see a more stable market with fewer large scale layoffs. • In long term, the demand for high quality, experienced underwriters will increase dramatically due to retirement of our industry’s seasoned veterans (there’s a lot of grey hair at industry meetings!) • Concern should not be that there will be too many people trying to fill just a few positions, but whether or not we will have enough qualified talent available 10+ years from now. • This fact should make underwriting education a top priority for every company.

Measuring Underwriting Performance • How should we measure underwriting performance? • Increased emphasis on time-service • Increased emphasis on quality communication skills • Continued emphasis on quality underwriting. • What’s most important?

Quality vs. Productivity • Which blade in a pair of scissors is most important? • An underwriter who makes very high quality underwriting decisions and fails to keep up with minimal production requirements can’t be considered acceptable in our “I need it yesterday” world. • An underwriter who is top in production, but makes poor decisions also isn’t acceptable in our “bottom line” world. • Both Quality and Productivity must be taken into account, with a bit more emphasis placed on quality. • Don’t forget the 3rd measurement of underwriting performance: Communication.

Impact of Underwriting Engines on the Future of Underwriting • Think of these systems as “Screeners” • Bottom line impact on our profession is that underwriters will be expected to do what they are trained to do: Handle the more complex cases. • This is another case for the importance of quality continued underwriting education.

Underwriting Engines and New Underwriters • With an engine making decisions on clean cases, how will new underwriters gain experience? • In the past, Junior Underwriters handled many of these clean cases and then progressed on to more complicated cases. • Classroom-type training is important, but nothing beats tying learning to the real world. • This will require more one-on-one mentor training.

What does all this mean to us? • Underwriting has been focused on disease • The best underwriters were the ones who could pull together all facts on a disease or condition and correctly assess that individual’s mortality • The new underwriting paradigm will focus on speed and database mining for smaller and younger applicants. Underwriters will increasingly focus on underwriting complex medical and financial cases and handling cases disqualified by decision engines. • Understanding which individuals are likely to live longer lives by looking at all available data is the next great underwriting opportunity • Hang on, the ride is going to be wild!