Download

1 / 49

490 likes | 574 Views

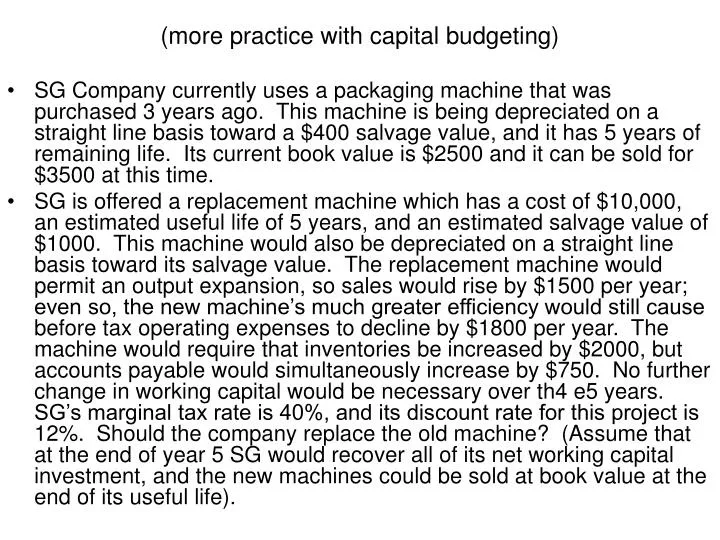

(more practice with capital budgeting).

E N D

(more practice with capital budgeting) • SG Company currently uses a packaging machine that was purchased 3 years ago. This machine is being depreciated on a straight line basis toward a $400 salvage value, and it has 5 years of remaining life. Its current book value is $2500 and it can be sold for $3500 at this time. • SG is offered a replacement machine which has a cost of $10,000, an estimated useful life of 5 years, and an estimated salvage value of $1000. This machine would also be depreciated on a straight line basis toward its salvage value. The replacement machine would permit an output expansion, so sales would rise by $1500 per year; even so, the new machine’s much greater efficiency would still cause before tax operating expenses to decline by $1800 per year. The machine would require that inventories be increased by $2000, but accounts payable would simultaneously increase by $750. No further change in working capital would be necessary over th4 e5 years. SG’s marginal tax rate is 40%, and its discount rate for this project is 12%. Should the company replace the old machine? (Assume that at the end of year 5 SG would recover all of its net working capital investment, and the new machines could be sold at book value at the end of its useful life).

Risk & Return • Chapter 9: 3,12,13,17 • Chapter 10: 3,5,13,17,22,27,34,38 • Note - In chapter 10, skip the following sections: • Efficient set (section 10.4) • Efficient set for many securities: skip the first part of section 10.5, page 270 to middle of 271 • The optimal portfolio, p. 278-280.

Measuring historical returns Total return = dividend income + capital gains % total return = Rt+1 = (Divt+1+ Pt+1- Pt)/Pt Geometric mean returns (1+ R)T = (1+R1)(1+R2)…(1+Rt)…(1+RT) RA = [(1.15)(1.00)(1.05)(1.20)](1/4)-1 .0972 = 9.72% RB = [(1.30)(0.80)(1.20)(1.50)](1/4)-1 .1697 = 16.97% Arithmetic mean returns: R = (R1 + R2 + …+ RT)/T RA = [.15 + .00 + .05 + .20]/4 = .10 = 10% RB = [.30 + -.20 + .20 + .50]/4 = .20 = 20%

Measuring total risk Return volatility: the usual measure of volatility is the standard deviation, which is the square root of the variance.

Calculating historical risk & return: example • The variance, ² or Var(R) = .0954/(T-1) = .0954/3 = .0318 • The standard deviation, or SD(R) =.0318 = .1783 or 17.83%

Capital Market History: Risk Return Tradeoff (Ibbotson, 1926-2003) Risk premium = difference between risky investment's return and riskless return.

EXPECTED (vs. Historical) RETURNS & VARIANCES Calculating the Expected Return: Expected return = (-1.25 + 7.50 + 8.75) = 15%

EXPECTED (vs. Historical) RETURNS & VARIANCES Calculating the variance:

PORTFOLIO EXPECTED RETURNS & VARIANCES Portfolioweights: 50% in Asset A and 50% in Asset B E(RP) = 0.40 x (.125) + 0.60 x (.075) = .095 = 9.5% Var(RP) = 0.40 x (.125-.095)² + 0.60 x (.075-.095)² = .0006 SD(RP) =.0006 = .0245 = 2.45% Note: E(RP) = .50 x E(RA) + .50 x E(RB) = 9.5% BUT: Var(RP) ≠ .50 x Var(RA) + .50 x Var(RB) !!!!

PORTFOLIO EXPECTED RETURNS & VARIANCES New Portfolio weights: put 3/7 in A and 4/7 in B: E(RP) = 10% SD(RP) = 0 !!!!

Covariance and correlation: measuring how two variables are related Covariance is defined: AB = Cov(RA,RB) = Expected value of [(RA-RA) x (RB-RB)] Correlation is defined (-1< AB<1): AB = Corr(RA,RB) = Cov(RA,RB) / (A x B) = AB / (A x B)

Portfolio risk & return If XA and XB the portfolio weights, The expected return on a portfolio is a weighted average of the expected returns on the individual securities: Portfolio variance is measured:

Portfolio Risk & Return: Example RA = (-0.20 + 0.10 + 0.30 + 0.50)/4 = 0.175 Var(RA) = ²A = .2675/4 = .066875 SD(RA) = A = .066875 = .2586 RB = (0.05 + 0.20 - 0.12 + 0.09)/4 = 0.055 Var(RB) = ²B = .0529/4 = .013225 SD(RB) = B = .013225 = .1150 AB = Cov(RA,RB) = -0.0195/4 = -0.004875 AB = Corr(RA,RB) = AB / AB = -0.004875/(.2586x.1150) = -.1369

Benefits of diversification Consider two companies A & B, and portfolio weights XA = .5, XB = .5 Stock AStock B E(RA)=10% E(RB)=15% A=10% B=30% Case 1: AB = 1 (AB = AB/AB)

Benefits of diversification Stock AStock B E(RA)=10% E(RB)=15% A=10% B=30% Case 2: AB = 0.2 (AB = AB/AB)

Benefits of diversification Stock AStock B E(RA)=10% E(RB)=15% A=10% B=30% Case 3: AB = 0 (AB = AB/AB)

Intuition of CAPM Components of returns: Total return = Expected return + Unexpected return R = E(R) + U The unanticipated part of the return is the true risk of any investment. The risk of any individual stock can be separated into two components. 1. Systematic or market risks (nondiversifiable). 2. Unsystematic, unique, or asset-specific (diversifiable risks). R = E(R) + U = E(R) + systematic portion + unsystematic portion

Measuring systematic risk: beta Rm =proxy for the "market" return Portfolio beta =weighted ave of individual asset’s betas

Portfolio risk (beta) vs. return Consider portfolios of: Risky asset A, ßA = 1.2, E(RA) = 18% Risk free asset, Rf = 7%

Market equilibrium Reward/risk ratio = E(Ri) - Rf = constant! ßi The line that describes the relationship between systematic risk and expected return is called the security market line.

Market equilibrium The market as a whole has a beta of 1. It also plots on the SML, so:

Using the CAPM: estimating beta Regression output Data providers Bloomberg, Datastream, Value Line

Estimating beta • How much historical data should we use? • What return interval should we use? • What data source should we use?

DETERMINANTS OF BETA: Operating vs. financial leverage Sales - costs - depr EBIT - interest - taxes Net income

Determinants of beta: financial leverage With no taxes, beta of a portfolio of debt & equity = beta of assets, or If Debt is not too risky, assume D = 0 , so or In most cases, it is more useful to include corporate taxes:

Example: equity betas vs. leverage McDonnell Douglas(pre merger) equity (levered) beta 0.59 D/E .875% Tax rate = 34% risk premium = 8.5% T-Bill = 5.24% Unlevered beta = current beta/(1 + (1-tax rate)(D/E) = .59/(1+(1-.34)(.875) = .374

Estimating betas using betas of comparable companies Continental Airlines, 1992 restructuring

Example: estimating beta Novell, which had a market value of equity of $2 billion and a beta of 1.50, announced that it was acquiring WordPerfect, which had a market value of equity of $1 billion, and a beta of 1.30. Neither firm had any debt in its financial structure at the time of the acquisition, and the corporate tax rate was 40%. Estimate the beta for Novell after the acquisition, assuming that the entire acquisition was financed with equity. Assume that Novell had to borrow the $1 billion to acquire WordPerfect. Estimate the beta after the acquisition.

Example: estimating beta Southwestern Bell, a phone company, is considering expanding its operations into the media business. The beta for the company at the end of 1995 was 0.90, and the debt/equity ratio was 1. The media business is expected to be 30% of the overall firm value in 1999, and the average beta of comparable media firms is 1.20; the average debt/equity ratio for these firms is 50%. The marginal corporate tax rate is 36%. a. Estimate the beta for Southwestern Bell in 1999, assuming that it maintains its current debt/equity ratio. b. Estimate the beta for Southwestern Bell in 1999, assuming that it decides to finance its media operations with a debt/equity ratio of 50%.

WACC • The key is that the rate will depend on the risk of the cash flows • The cost of capital is an opportunity cost - it depends on where the money goes, not where it comes from. WACC = (E/V) x Re + (D/V) x RD x (1 - T)

Northwestern Corporation 8/04 - WACC WACC = (E/V) x Re + (D/V) x RD x (1 - T) Historical beta? Sources for beta?

Northwestern Corporation - peers Sources?

Northwestern Corporation – Cost of equity re = rf + βe(rm – rf) Levered beta = .41*(1+(1-.385)*1.381) = 0.75 Ibbotson ’03*, (rm – rf) = 7% 20 year bond 4/02 = 5.9% Re = 5.9% + 0.75*(7%) = 9.85% Adding a 1.48% size risk premia (Ibbottson), and 2% company specific risk premia, cost of equity = 13.33% *Arithmetic mean, large stocks – long term treasury bonds, time period not specified

Northwestern Corporation - WACC WACC = (E/V) x re + (D/V) x rD x (1 - T)