Download

1 / 65

660 likes | 786 Views

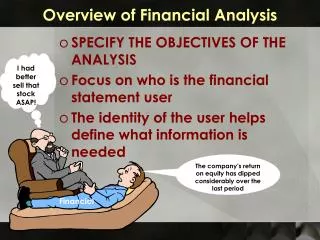

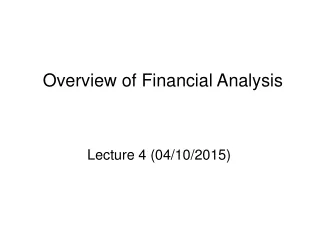

Overview of Financial Analysis. Rodney K. Rogers, Ph.D., CPA School of Business Administration Portland State University. Analyzing a Firm. Operations/Investing. $. Goods. Vendor. Customer. $. Goods. $. $. $. $. Information Intermediaries. Financial Intermediaries. Creditors.

E N D

Overview of Financial Analysis Rodney K. Rogers, Ph.D., CPA School of Business Administration Portland State University

Analyzing a Firm Operations/Investing $ Goods Vendor Customer $ Goods $ $ $ $ Information Intermediaries Financial Intermediaries Creditors Investors

External Parties Customers Employees Shareholders Firm Competitors Government Management Creditors Vendors

How does it get communicated? • Tell Them • Annual Report • Financial Statements, Footnotes, Management Disclosures (M.D.&A.) • Public Announcements, SEC Filings • Show Them • Financial Structure, Results • Problem:

Communication Issues • Managers have better information • “Information asymmetry” • Managers and external users have different interests – “Principal – Agent” • Management’s interests • Smooth earnings • Meeting expectations • Bonus issues

From Business Activities to Financial Statements Business Environment Business Strategy Business Activities Accounting Environment Accounting Strategy Accounting System Financial Statements

Analysis of a Company • Business Environment – “Context” • Macroeconomic, governmental, legal considerations, • Business Strategy Analysis – “Expectations” • Key profit drivers, business risks and profit potential • Accounting Analysis • Evaluate the “quality” of the accounting numbers • Financial Analysis • Evaluate performance using financial and non-financial information – (past and current results) • Prospective Analysis • Forecasts and valuation

SWOT Analysis • Internal • Strengths • Weaknesses • External • Opportunities • Threats

Business Environment • Interest Rates • US and foreign GNP Growth • Unemployment Levels • Trends in Consumer savings/borrowing • Others

Business Strategy Analysis • Specific Industry Structure • Rivalry among existing firms • Industry Growth, Concentration, Switching Costs, Fixed/Variable Costs, Excess Capacity • Threat of new entrants • Scale Economies, First mover, Relationships • Threat of substitute products • Price/Performance trade-off • Bargaining power of buyers and suppliers • Switching cots, number and volume of buyers/suppliers • Competitive Strategy • Cost Leadership • Differentiation

Competitive Strategy • Cost Leadership • Same product or service at lower cost • Economies of scale, efficient production, design • Differentiation • Unique product or service at a premium price • Product design, variety, customer service, brand, R&D, innovation • How to maintain competitive status?

Business Strategy Analysis • Quality of Management • Regulatory Developments • Social Issues • Technology

Review of Basic Financial Statements • Balance Sheet • Income Statement • Statement of Cash Flows • Retained Earnings Statement • Statement of Comprehensive Income

Analyzing a Firm Operations/Investing $ Goods Vendor Customer $ Goods $ $ $ $ Information Intermediaries Financial Intermediaries Creditors Investors

Accounting Analysis • Quality of Disclosures • Quality of Numbers

Quality of Numbers • Sales • Price vs. volume Charges • Real vs. nominal growth • Cost of Goods Sold • Cost-flow assumptions • LIFO liquidation • Loss/Reserves on write-down of inventory

Quality of Numbers • Operating Expenses • Discretionary expenses • R&D • Repair and Maintenance • Advertising and Marketing • Depreciation • Methods • Estimates • Pension Accounting

Quality of Numbers • Nonoperating Revenue and Expenses • Gains/Losses from Sales of Assets • Interest Income • Equity Income • Loss recognition on write-down of assets • Accounting changes • Extraordinary items • Reserves on restructuring charges

Financial Analysis:Levers for Value Creation Return on Equity = Net Income Shareholder’s Equity

Interrelationships of Ratios Return on = Profit Margin x Asset Turnover x Financial Equity Leverage • Change revenues • higher prices • greater volume • Change costs • product/process design • supply relationships net income = net income x sales x assets owner’s equity sales assets owner’s equity Advantageous financing (external) Reduce need for investment (capital intensity) Rev/Exp Assets Liabilities/Equity Managing

Managing Sales and Expenses • Gross Profit • Operating Profit • Issues to Consider • Price vs. Volume Changes • Real vs. Nominal Growth • Inventory Issues

Profitability Ratios Gross Profit Margin = Gross Profit Net Sales Operating Profit Margin = Operating Profit Net Sales Net Profit Margin = Net Earnings Net Sales

Profitability Ratios SGA % = Selling, General and Admin. Expenses Net Sales Return on Investment (ROI) = Net Earnings Total Assets Cash Flow Margin = Cash flow from operations Net Sales

Managing Assets Days in Receivables = Accounts Receivable Avg.Daily Sales A.R. Turnover = Net Sales Accounts Receivables Inventory Turnover = Cost of Goods Sold Inventory Fixed Asset Turnover = Net Sales Net Prop.Plant&Equip. Total Asset Turnover = Net Sales Total Assets

Managing Liabilities and Equity Current Ratio = Current Assets Current Liabilities Quick Ratio = Current Assets-Inventory Current Liabilities

Managing Liabilities and Equity Debt Ratio = Total Liabilities Total Assets L.T. Debt to Total Capital = LT Debt LT Debt + S.E. Debt to Equity = Total Liabilities Shareholders’ Equity Times Interest Earned = Operating Profit Interest Expense

Interrelationships of Ratios Return on = Profit Margin x Asset Turnover x Financial Equity Leverage • Change revenues • higher prices • greater volume • Change costs • product/process design • supply relationships net income = net income x sales x assets owner’s equity sales assets owner’s equity Advantageous financing (external) Reduce need for investment (capital intensity) Rev/Exp Assets Liabilities/Equity Managing

Market Ratios Earnings Per Share = Net Earnings Avg. Shares Outstanding Price to Earnings Ratio = Market Price of Common Stock Earnings Per Share Dividend Payout Ratio = Dividends Per Share Earnings Per Share Dividend Yield = Dividends Per Share Market Price of Common Stock

How Does a Firm Create “Value” for Its Investors? If a firm makes a profit has it created “value?” An investment creates value for its owners only when its expected return exceeds its cost of capital.

When is Value Created? By providing a return to investors that exceeds the cost of capital: Return on invested capital (ROIC): Return to Investors Invested Capital = ROIC (%) The value created for shareholders is: Return to Investors – Capital Charge = Value Added where Capital charge = Invested Capital × WAAC

How to estimate capital Capital can be estimated from the balance sheet (net assets): Net assets = Assets – Accounts payable (free financing) Assets = Left Hand Side of Balance Sheet = Cash + Accounts receivables + Inventory + Fixed assets + . . .

Value Added = Return to investors – Capital charge where... Return to investors = EBIT × (1 – tax rate) (EBIT stands for earnings before interest and taxes.) Capital charge = Capital × WACC Note: Return to investors is the same concept as Net Operating Profit after Taxes (NOPAT) Value added > 0 is equivalent to ROIC > WACC

The real point of the capital charge What can managers do to increase the CACC, and thus increase shareholder value? Value Added = EBIT(1-tax) - Capital Charge (Sales - COGS+SGA+Other) X (1-tax) Net Assets X WACC

Prospective Analysis • Forecast future results of firm’s transactions • Mean reverting, Business Environment, Business Strategy • Valuing a Firm • Discounted abnormal earnings • Price Multiples • Discounted cash flows • Weighted Average Cost of Capital (WACC)

Discounted abnormal earnings • Equity Value = Book Value + PV of expected future abnormal earnings • Future abnormal earnings = net income adjusted for a capital charge • Capital charge = Beginning book value X WACC

Price Multiples • Step 1 – select a measure of performance or value (ie. Earnings, book equity, etc) • Step 2 – Estimate price multiples for comparable firms • Step 3 – Apply the comparable firm multiple of the performance/value measure of firm being analyzed

Discounted cash flows • Equity value = PV of free cash flows to equity claim holders • Free cash flows to equity claim holders = operating cash flow – capital outlays + net cash flows from debt owners • Discounted at WACC

EVA and MVA • EVA = Net operating profit after taxes - cost of capital • Earnings above the cost of paying the investors (profit to the shareholders) • MVA = Market value - total capital invested • MVA is the present value of all expected future EVA

Net Sales • - Operating expenses • Operating profit • -Taxes • Net Operating Profit • -Capital Charges • EVA

Gains in shareholder wealth are driven by gains in EVA • Maximizing the MVA should be the primary objective for any company that is concerned about its shareholder’s wealth

EVA does not incorporate growth into its computation • more appropriate to mature industries • not a true cash basis • basically a version of residual income • RI=ROI - (cost of capital X total assets) • EVA may be cumbersome and difficult to explain • MVA is an estimate of market’s evaluation of growth potential

Ways to raise EVA • Raise profit without raising amount o f capital • cost cutting • increased revenues • etc. • Reduce capital • eliminate WIP • etc. • Invest in high return projects

Managerial implication • EVA should move managers to invest in activities that improve return on investment • Moves resources to most useful applications • Tie EVA to incentives • Use EVA for all employees • Objective • Simple • Significant • Definitive

No caps on plan • Retain some of the compensation, and tie to future results • Include a cancellation clause

Various Terms • RI = Operating income – CofC • RI = Residual Income • EVA = NOPAT – CofC • EVA = Economic Value Added • CFROI = Operating cash flow / Capital • CFROI = Cash Flow Return on Investment • RCF = Operating cash flow – CofC • RCF = Residual Cash Flow

Are financial measures adequate? Should they be scrapped? Lagging or leading indicators? Management’s discretion

BalancedScorecard A multi-dimensional measurement system that translates an organization’s mission and strategy into goals/objectives and performance measures (with target levels)(Leading and lagging indicators)