Download

1 / 26

280 likes | 436 Views

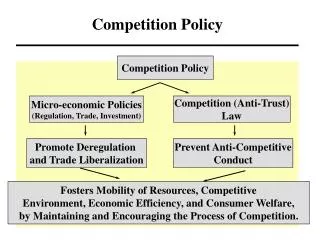

Competition policy in the food industry. Lectures 33 and 34. Economics of Food Markets Alan Matthews. Seller power. Buyer power. Buyer power. Seller power. Market power in the food chain. Input suppliers. Farmers. Price squeeze. Processors. Retailers. Consumers. Lecture objectives.

E N D

Competition policy in the food industry Lectures 33 and 34. Economics of Food Markets Alan Matthews

Seller power Buyer power Buyer power Seller power Market power in the food chain Input suppliers Farmers Price squeeze Processors Retailers Consumers

Lecture objectives • How can market power in the food industry be addressed? • Countervailing power • Government regulation • Competition policy

Reading • UK Competition Commission Report 2000 • + Emerging Thinking 2006 • Groceries Order reports

Countervailing power • Farmers can attempt to countervail through collective action and cooperative marketing • Cooperative action designed to improve farmers’ share of value added through • vertical integration (dairy coops, horticultural producer groups) • Improved bargaining position (liquid milk suppliers) Concept due to Galbraith (1968) • Requires special exemption in the US from anti-trust action under the Capper-Volstead Act • More extreme voices see collective action as a way of enforcing supply control • Vertical integration as an individual farmer strategy

Government regulation • Many European countries have regulations designed to try to protect small retailers from competition from large multiples (loi Galland in France, Groceries Order in Ireland until end-2005) • We examine the Groceries Order debate

Competition policy • Curtailing restrictive practices (collusive and cartel and price-fixing behaviour) • Preventing abuse of a dominant position (Irish Sugar) • Merger control – preventing a dominant position from arising • State aids (Enterprise Ireland proposal to reduce number of beef processors) • Encouragement to new entrants and reducing barriers to entry (planning)

UK Competition Commission report into food retailing 2000 • Perception that grocery prices in the UK tended to be higher than comparable EU countries • Apparent disparity between farmgate and retail prices • Continuing concern that out of town supermarkets were contributing to the decay of the high street in many towns. • Barriers to entry limiting competition • The level of supermarket operators’ profitability • Concerns about the intensity of competition between supermarket operators • Relationship between supermarket operators and their suppliers

UK Competition Commission report into food retailing 2000 • UK food prices declined in real terms from 1989 to 1998… • …but international comparison of grocery prices, allowing for quality and tax differences, showed that in late 1999 UK prices were on average 12 to 16 per cent higher than those in France, Germany and the Netherlands. • However, comparison was very influenced by value of sterling which could distort the comparison by between 7 and 17 per cent. • Overall profitability of the industry could not be considered excessive over period 1996 to 1999.

UK supermarkets profitability Higher gross margins reflect higher share of own-label products where various costs usually borne by food manufacturer are borne by the retailer The very similar operating margin despite higher gross margin indicates that cost base of UK supermarkets is higher (higher land and building costs) Overall Commission concluded that profitability of UK retailing was not excessive Source: Competition Commission 2000

Potential anti-competitive practices identified by the Commission a) adopting pricing structures and regimes that, by focusing competition on a relatively small number of frequently purchased product lines, restrict active competition on the majority of product lines; (b) selling, on a persistent basis, certain frequently purchased products either below cost (ie at a negative gross margin) or at retail prices that do not cover all direct costs; (c) setting retail prices across different stores in different geographical areas in the light of local competitive conditions, such variation not being related to costs; (d) setting the prices of some own-brand products in relation to their branded equivalents rather than to their underlying costs; and (e) making changes to retail prices for some products that do not sufficiently rapidly reflect changes in their corresponding wholesale prices.

UK Competition Commission – findings on limited price competition • Issue is whether supermarkets just compete on a limited number of KVI’s, thus allowing them to charge higher (excessive?) margins on other products (‘price focusing’) • Consumer surveys highlight the importance of prices on limited number of frequently bought products; price focusing exacerbated by promotional activity • Evidence that margins vary greatly (20-50%) across products. Supermarkets price in relation to demand rather than cost • Supermarkets claim they regularly monitor prices on wide range (>1,000 products) • Commission found that price focusing does distort competition but, in view of overall low profitability of supermarkets, does not act against the public interest

UK Competition Commission – findings on below cost selling • Found that all the main supermarkets (with exception of M&S and Lidl) engaged in below-cost selling. • Commission held that, despite its benefits to low income consumers, it damaged smaller supermarkets and independent outlets, and when practiced by supermarkets with market power was against the public interest. • Did not find evidence that below cost selling was motivated by predatory concerns. • Noted administrative difficulties in defining below cost selling and legitimate exceptions (end of stock products, close to sell by date)

UK Competition Commission – findings on below cost selling • Quoted the 1991 Irish Fair Trade Commission report that the ban on below cost selling had resulted in higher prices overall, a decrease in price competition and an increase in margins • Considered a rule requiring below cost sellers to sell without quantity limits to anyone who wished to buy • Argued that remedies would be disproportionately costly in relation to the adverse effects involved.

UK Competition Commission report into food retailing 2000 • They found that prices varied in different geographical locations in the light of local competitive conditions (‘price flexing’). when practiced by supermarkets with market power was against the public interest. • They found that competition focused on KVI’s and that this distorted competition in the retail supply of groceries because not all products are fully exposed to competitive pressure. However, concluded that practice did not contribute to excessive profits or lead to consumers paying higher prices overall. • They dismissed claim that own label products were priced in relation to branded products (‘umbrella pricing’) rather than cost and were thus excessively profitable.

Groceries Order • Long history of regulating competition in the retail grocery trade. Selective dates: • 1956 Order prohibited resale price maintenance, collective price fixing by suppliers and wholesalers, withholding supplies from a retailer • 1973 advertising price of goods below cost was prohibited • 1987 Order represented a fundamental shift by introducing a ban on below invoice price selling

Groceries Order • Ink was no sooner dry than Order was reviewed • 1991 Fair Trade Commission recommended by 2-1 majority to abolish the Order • 2000 Competition and Mergers Review Group • 2004 National Competitiveness Council • 2005 Department of Enterprise Trade and Employment Public Consultation Process • 2005 Joint Oireachtas Committee on Enterprise and Small Business • 2005 Consumer Strategy Group

Groceries Order • Key questions • What was impact of the Order on competition? • What was impact of the Order on slowing structural change and defending position of the independent retailer? • What was impact of the Order on prices?

Groceries Order – effect on competition • Order intended to prevent below-cost selling seen as a predatory device which would ultimately limit competition • Order makes it illegal to sell particular grocery products below the net invoice price • Predatory pricing anyway illegal and very unlikely in the retail trade

Groceries Order – effect on competition • Predatory pricing should be distinguished from practice of loss leading • Loss leading not necessarily welfare-reducing (Walsh and Whelan) • But GO did not prevent below cost selling, it prevented selling below net invoice price • Effectively reintroduced resale price maintenance by allowing manufacturers to set retail price • Off invoice discounts could not be passed on to consumers

Groceries Order – effect on retail structure • Ireland has more concentrated retail structure than UK which does not have GO • Supermarkets not competing directly with the independent sector which is now concentrating on convenience • Retail development can be partly controlled through planning guidelines

Groceries Order – effect on prices • Hard to disentangle effect of GO from other influences on food prices • Food prices have risen less than general inflation… • .. But GO prices have risen faster than non-GO prices… • .. And Irish prices higher than elsewhere • Collins and Oustapssidis (C&O) show impact of Order econometrically

Groceries Order – effect on prices • C&O hypothesis was that the GO increased retailer gross margins in the affected product categories • Tested hypothesis in the ‘processed and preserved fruit and vegetables’ sector • Average weighted retail prices for 13 items were compared to wholesale price index for NACE 414 sector to construct a ‘processor-retail price spread’

Groceries Order – effect on prices • Model to be estimated Retmar = Const+Cr4+Advgval88+ GDPCP+Sterl+Legis +Dum414 • Retmar = retail margin • Cr4 = concentration measure • Advgval = measure of retailer advertising intensity – the more advertising, the smaller the margin • GDPCP = control for changing demand conditions • Sterl = dummy for exit of sterling from EMS • Legis = dummy for period when GO was in effect

Groceries Order – effect on prices • Model was estimated using quarterly data from 1984 to 1994 • Positive sign on LEGIS variable suggesting that the GO increased retailer margins by 4.6 percentage points

Impact of repeal of the Groceries Order Source: Bord Bia, Export Review and Outlook 2006/07