Download

1 / 31

310 likes | 421 Views

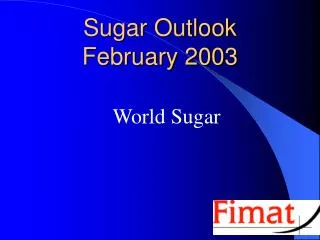

2009 Int. Sweetener Colloquium 8-11 February 2009 Orlando. World Sugar Market Outlook. Stefan Uhlenbrock F.O. Licht Commodity Analysts Ratzeburg, Germany. World Raw Sugar Prices: NY #11 Cents/lb. 15.07. 9.52. Key factors of price formation Speculative activity

E N D

2009 Int. Sweetener Colloquium 8-11 February 2009 Orlando World Sugar Market Outlook Stefan Uhlenbrock F.O. Licht Commodity Analysts Ratzeburg, Germany

World Raw Sugar Prices: NY #11 Cents/lb 15.07 9.52 International Sweetener Colloquium, 8-11 February 2009, Orlando

Key factors of price formation • Speculative activity • Crude oil and commodity prices in general • Energy policy • Sugar policy • Freight rates • Exchange rates • Interest rates • International Trade Policy and Agreements • Inflation • Political reform International Sweetener Colloquium, 8-11 February 2009, Orlando

ICE Non-Commercial Futures Position and Total Open Interest (1,000 contracts) Open interest long/short long short International Sweetener Colloquium, 8-11 February 2009, Orlando

2007/08 Another year of surplus What about 2008/09? International Sweetener Colloquium, 8-11 February 2009, Orlando

World Raw Sugar Prices: NY #11 Cents/lb 11.81 11.75 10.82 International Sweetener Colloquium, 8-11 February 2009, Orlando

World Sugar Production mln tonnes, raw value Feb 2, 2009 International Sweetener Colloquium, 8-11 February 2009, Orlando

World Sugar Balance mln tonnes, raw value Feb 2, 2009 International Sweetener Colloquium, 8-11 February 2009, Orlando

Key market drivers International Sweetener Colloquium, 8-11 February 2009, Orlando

Ethanol: The wild card in the game International Sweetener Colloquium, 8-11 February 2009, Orlando

Crude vs. Corn vs. Sugar indexes Brent Oil +217% CBOT corn As at early June 2008 +201% +14% ICE Raw sugar International Sweetener Colloquium, 8-11 February 2009, Orlando

Why has corn moved up (and down) in line with crude oil but sugar not? International Sweetener Colloquium, 8-11 February 2009, Orlando

Tight global grain markets due to several years of poor crops Stocks-to-use ratios: Corn 15.7% 2008/09 Wheat 22.7% Sugar 46.0% • Corn use for ethanol rises faster than cane use for ethanol International Sweetener Colloquium, 8-11 February 2009, Orlando

US cropland is scarce Corn area increased by 20% in 2007, but total plantings by just 1.3% • Brazilian (non-Amazon) cropland is not scarce • Brazil‘s gasoline prices are government-controlled and do not fluctuate in line with global oil prices International Sweetener Colloquium, 8-11 February 2009, Orlando

Can ethanol eat away the sugar glut? International Sweetener Colloquium, 8-11 February 2009, Orlando

Except for Brazil, ethanol production directly from cane juice is not (yet) a reality on a large scale • Ethanol is often produced from the the sugar by-product molasses (no rival use of cane) • Surplus cane sugar will continue to pressure sugar prices International Sweetener Colloquium, 8-11 February 2009, Orlando

Crude vs. Corn vs. Sugar indexes As at February 3, 2009 CBOT corn +77% Raw sugar +41% +7% Brent Oil International Sweetener Colloquium, 8-11 February 2009, Orlando

World population increase International Sweetener Colloquium, 8-11 February 2009, Orlando

World Sugar Consumption (mln tonnes, raw value) +27 International Sweetener Colloquium, 8-11 February 2009, Orlando

The world needs more sugar (at least in the long term) International Sweetener Colloquium, 8-11 February 2009, Orlando

Who can fill the gap? International Sweetener Colloquium, 8-11 February 2009, Orlando

India: Sugar production (mln tonnes, raw value) +123% International Sweetener Colloquium, 8-11 February 2009, Orlando

Inconsistent government policy on cane and sugar prices leads to sharp cyclical swings • Huge cane arrears lead to sharp downturn in sugar production in 2008/09 • India is not a reliable = consistent sugar exporter but a swing producer who changes back and forth in its net trade position International Sweetener Colloquium, 8-11 February 2009, Orlando

Brazil: Sugarcane production (mln tonnes) +120% International Sweetener Colloquium, 8-11 February 2009, Orlando

Brazil: Sugar vs. Ethanol (in % of the cane crop) International Sweetener Colloquium, 8-11 February 2009, Orlando

Brazil: Car Sales By Engine (units per month) International Sweetener Colloquium, 8-11 February 2009, Orlando

Brazil: Sugar production and exports (mln tonnes, raw value) International Sweetener Colloquium, 8-11 February 2009, Orlando

Brazil‘s sugar output more than doubled since 2000/01 despite its ethanol boom • 2008/09 cane crop growth: 15% • 2009/10 projection: 6 % • Sugar output to rise much stronger in 09/10: • ethanol export prospects fade (1% change in sugar/ethanol mix means 750,000 t sugar) • less global competiton (India!) • Depreciation of Real increases returns in local currency International Sweetener Colloquium, 8-11 February 2009, Orlando

Conclusions • 2007/08 saw another global surplus with an addition to stocks of about 14 mln t over a period of just two years, elevating the stocks-to-use ratio to 49.1% (179 days of consumption). • Current predictions for 2008/09 are for a significant deficit, but surplus stocks will have to be worked off before a return to a healthier fundamental picture. • A price boom as in the 1970s and the beginning of the 1980s is unlikely, given the vast amounts of cane available in Brazil. International Sweetener Colloquium, 8-11 February 2009, Orlando

The key question in the years to come will be how much Brazilian cane will be diverted into producing fuel ethanol and sugar (A 1% change in the sugar/ethanol mix means 750,000 tonnes of sugar). • Outside influences have become almost as important as the sugar market‘s own fundamentals and will continue to do so in the future. International Sweetener Colloquium, 8-11 February 2009, Orlando