Download

1 / 4

40 likes | 142 Views

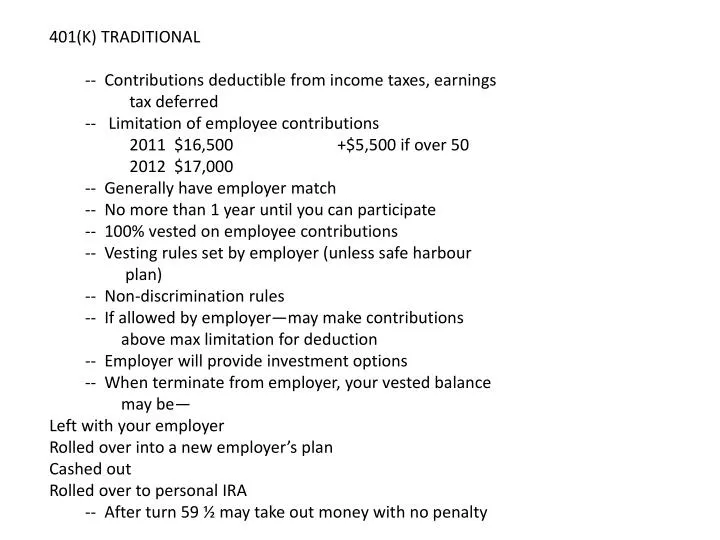

401(K) TRADITIONAL -- Contributions deductible from income taxes, earnings tax deferred -- Limitation of employee contributions 2011 $16,500 +$5,500 if over 50 2012 $17,000 -- Generally have employer match -- No more than 1 year until you can participate

E N D

401(K) TRADITIONAL • -- Contributions deductible from income taxes, earnings • tax deferred • -- Limitation of employee contributions • 2011 $16,500 +$5,500 if over 50 • 2012 $17,000 • -- Generally have employer match • -- No more than 1 year until you can participate • -- 100% vested on employee contributions • -- Vesting rules set by employer (unless safe harbour • plan) • -- Non-discrimination rules • -- If allowed by employer—may make contributions • above max limitation for deduction • -- Employer will provide investment options • -- When terminate from employer, your vested balance • may be— • Left with your employer • Rolled over into a new employer’s plan • Cashed out • Rolled over to personal IRA • -- After turn 59 ½ may take out money with no penalty

DEFINED BENEFIT PLANS – -- Very common for governmental agencies and some large older companies -- Plans vary from company to company -- Common Plan Provisions (Participants) -- Retirement eligibility based on either age or combination of age and years service -- Monthly benefit based on final salary level, years service, remains constant for life -- Options based on whether for employees life or continuation of pay- ments to spouse (actuarial equivalent call) -- Max allowed comp for calc. $250,000 -- Usually 5 year vesting -- Non-portable until reach retirement age (employer may or may not allow cash distribution)

FUNDING RULES FOR EMPLOYERS -- Actuarial Calculation of Funding Required -- Calculation Uses -- Ages -- Salaries -- Est. Salary Increase Rates -- Mortality Tables -- Est. Future Earning Capability -- Turn-over Rate -- Fund Balance -- Amortization of Prior Shortfall

MISCELLANEOUS RETIREMENT POINTS -- ROTH IRA -- Maximum contribution -- $6,000 -- Not tax deductible at time of contribution -- Withdrawals after age 59 ½ tax free (both contributions and earnings) -- No requirement to start withdrawal after age 70 ½ (traditional 401(k) or IRA require that distributions must start at this age -- Decision between Roth or Traditional IRA dependent upon estimated future tax rates v. current marginal tax rates -- 401(k) PLANS -- Employers may use individual 401(k) accounts for a defined contribution retirement plan with maximum contributions (including 401(k) match) of $50,000