Download

1 / 7

70 likes | 213 Views

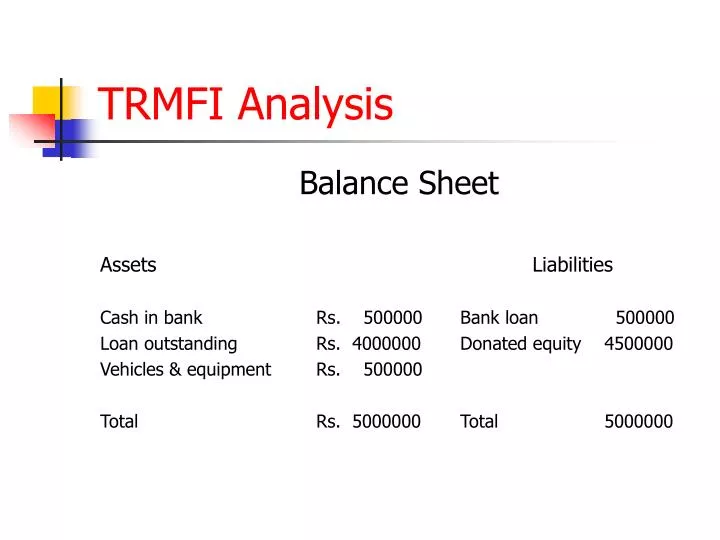

TRMFI Analysis. Balance Sheet Assets Liabilities Cash in bank Rs. 500000 Bank loan 500000 Loan outstanding Rs. 4000000 Donated equity 4500000 Vehicles & equipment Rs. 500000 Total Rs. 5000000 Total 5000000. TRMFI Analysis. Profit and Loss Account

E N D

TRMFI Analysis Balance Sheet Assets Liabilities Cash in bank Rs. 500000 Bank loan 500000 Loan outstanding Rs. 4000000 Donated equity 4500000 Vehicles & equipment Rs. 500000 Total Rs. 5000000 Total 5000000

TRMFI Analysis Profit and Loss Account Income Expenditure Interest on loans 1000000 Field staff 1000000 Operating grant 1000000 Head office 400000 Travel 300000 Depreciation 100000 Bank interest 100000 Bed debt 100000 Total 2000000 2000000

Options before TRMFI • Increase interest rate • Increase turnover (lend more money) • Get cheap funds from other concessional sources • Eliminate defaults • Lend to fewer clients, and reduce the field staff • Lend out the money which is in bank • Replace bank loan with members’ savings • Increase group size to reduce staff requirement • Reduce head office costs and traveling

Options before TRMFI • Double the interest rate (50 %) - increase the gross income by 1000000 - at one stroke eliminate the loss - will such interest rate acceptable? - may possibly increase the default?

Options before TRMFI • Double the portfolio to Rs. 80,000,00 - Additional interest income: 10,00000 - Additional cost of funds: 8,00000 - Provision for bad debts: 1,00000 - Net additional income: 1,00000 - staff numbers will have to be increased to manage the higher portfolio - bad debt may increase because of reduced supervision

Breakeven model • Maintain average loan size of Rs. 4000 • Increase interest rate to 30 % • Increase group size to 30, and increase staff load to 2 groups a day or 10 per week, making a total of 100 groups and 3000 clients • Induce a Rs. 100 per client annual service charge

Breakeven model • Loan portfolio, 3000 clients @ Rs. 4000 = Rs. 1,20,00000 • Interest @ 30 % = Rs. 36,00000 • Annual service charge, 3000 clients @ Rs. 100 = Rs. 3,00000 • Total income = Rs. 39,00000 • Cost of additional funds borrowed from banks 80,00000 @ 20% = Rs. 16,00000 • Bad debts, 2.5 % = Rs. 3,00000 • Other cost unchanged = Rs. 19,00000 • Total costs = Rs. 38,00000 • Annual Profit = Rs. 1,00000