Download

1 / 38

380 likes | 481 Views

Payroll Compliance Issues For Stock Compensation Presented by : Marlene Zobayan, Rutlen Associates LLC Date : October 13, 2017. Disclaimer.

E N D

Payroll Compliance Issues For Stock Compensation Presented by: Marlene Zobayan, Rutlen Associates LLC Date: October 13, 2017

Disclaimer This presentation contains general information only and the respective speakers and represented firms are not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. The respective speakers and firms shall not be responsible for any loss sustained by any person who relies on this presentation. This presentation focuses only on the payroll tax aspects, other compliance areas including other areas of tax, securities law, labor law, data privacy etc. are not addressed.

Agenda What do I have to report? Stock Options Basic Concepts Recent Developments Restricted Stock (RSAs & RSUs) Employee Stock Purchase Plans (ESPP) What do I have to withhold?

Supplemental Wages • Supplemental wages are payments to an employee that are not regular wages. They can include bonuses, commissions, overtime pay, severance pay, awards, back pay, and stock compensation • Supplemental wages can be subject to income tax withholding: • If paid with regular wages, as a regular income • If paid separately, subject to supplemental income tax rates • W4 ignored for withholding at supplemental income tax rates • Supplemental rate is not available for former employees who receive payments in the second calendar year after termination • Must withhold at the former employee’s W-4 rate

Withholding Rates • Federal: • 25% on supplemental income paid in the year up to $1,000,000 • 39.6% on supplemental income paid in the year over $1,000,000 • State: • California – 10.23% (bonuses and stock compensation), 6.6% other supplemental income • New York – 9.62% • Some states do not have supplemental withholding rate. Employers should withhold at W4 (or state equivalent) withholding rate • Social and payroll taxes: • Withhold as for regular wages • Local: • Varies

Deposit Rules • In general the Federal tax deposit rules for stock compensation follows the company’s regular deposit schedule; BUT if the cumulative Federal tax deposit for all employees exceeds $100,000, the amounts withheld must be deposited with the IRS by the next business day • Federal tax deposit generally includes: Some states have similar rules; e.g. • California: Next day deposit required if subject to the Federal next day deposit plus $500 in California PIT

Deposit Rules For Stock • Tax event date requiring Federal deposit: • Incentive stock options: none • Non-qualifying stock options: settlement (if no later than the third business day after exercise) • 2003 IRS Field Directive* • For this purpose business day = day stock exchange is open • RSAs: vest date unless s83b election made • RSUs: release date • Employee stock purchase plan: none *Assertion of the Penalty for Failure to Deposit Employment Taxes Field Directive March 14, 2003

Tax Withholding Methods • Same day sale: The options are exercised and all the shares immediately sold to deliver cash proceeds which are deposited in the employee’s brokerage account • Share withholding: shares are withheld in lieu of taxes. Company remits the taxes in cash • Employees may have a choice on tax withholding method • Sell to cover: The options are exercised and enough shares are sold to provide cash proceeds to cover the exercise price and withholding taxes due. The shares are deposited in the employee’s brokerage account • Cash: The employee pays cash for the price and taxes. The shares are deposited into the employee’s brokerage account

What are Stock Options? • A stock option gives an employee the right to purchase stock at a specific price (exercise price) at a future date • There are five main dates with regard to stock options • Grant – when the option is granted to the employee • There are no U.S. tax consequences • Vest – when the option is vested and the employee can exercise (assuming they are not in a blackout period) • There are no U.S. tax consequences • Exercise – when the employee exercises the option • There may be U.S. tax consequences • Sale – when the employee sells the shares acquired from the exercise of the option • There may be U.S. tax consequences • Forfeit – when the employee does not exercise within the time required • There are no U.S. tax consequences

Nonqualified Stock Options • At exercise: the difference between the exercise price and the fair market value (FMV) of the shares is taxed as compensation • The company must: • Withhold Federal, state, FICA, Medicare, local taxes as appropriate • Report the income on Form W-2 for the year of exercise • Box 12 Code V • At sale: • Increase in the FMV on stock held after exercise is taxed as a capital gain • Decrease in the FMV on stock held after exercise is taxed as a capital loss • The broker must • Report the proceeds from sale of shares on Form 1099-B

Nonqualified Stock Options The company may need to report income and withhold taxes in a year the individual was not employed by the company Post termination exercise period

Incentive Stock Options • At exercise: • No income tax consequences to the employee • However, the difference between the fair market value at exercise and exercise price is a preference item for Alternative Minimum Taxable (AMT) unless the subsequent sale of stock is in the same tax year as the ISO exercise. AMT is payable by the employee and not subject to tax withholding by the employer • At sale: • The sale is a “Qualified Disposition” and the income is taxed as a capital gain when the employee sells the shares under both these conditions: • > 2 years from the date of the option grant • > 1 year from the date of exercise • The sale is a “Disqualifying Disposition” when it does not meet the definition of a "Qualified Disposition" and the gain is taxed at income tax rates, up to 39.6% in 2017

Incentive Stock Options Qualifying Disposition

Incentive Stock Options Qualifying Disposition

Incentive Stock Options Remember: Company must report exercise on form 3921 Company must report on W-2 for disqualifying disposition only Ohio requires withholding on disqualifying dispositions Pennsylvania does not recognize the qualifying nature of ISOs and ESPP

What Are RSAs • A restricted stock award (RSA) gives an employee shares at grant but the shares cannot be transferred and are subject to forfeiture prior to vest • There are three main dates with regard to RSAs • Grant – when the RSA is granted to the employee • There are no U.S. tax consequences unless the employee makes a s83b election • Vest – when the RSA vests to the employee • There are U.S. tax consequences if s83b election not made • Sale – when the employee sells the shares acquired from the grant of the RSA • There may be U.S. tax consequences • At termination the employee forfeits any unvested RSAs

Restricted Stock Award • At grant: if the employee makes a s83b election, the fair market value (FMV) of the shares is taxed as compensation • Must be made within 30 days of grant • Irrevocable election even if the employee later forfeits the shares • At vest/release: if no s 83b election is made, the fair market value (FMV) of the shares is taxed as compensation income • At sale: • Increase in the FMV on stock held after taxing point is taxed as a capital gain • Decrease in the FMV on stock held after taxing point is taxed as a capital loss

What are RSUs? • A restricted stock unit (RSU) gives an employee the right to acquire stock at a future date at no cost • There are four main dates with regard to RSUs • Grant – when the RSU is granted to the employee • There are no U.S. tax consequences. S83b election cannot be made on RSUs • Vest – when the RSU vests to the employee • There are U.S. social tax consequences * • Release – when the shares are released to the employee • There are U.S. income tax consequences * • Sale – when the employee sells the shares • There may be U.S. tax consequences • Typically vest and release are on the same day • At termination the employee forfeits any unvested RSUs *Rule of Administrative Convenience allows FICA to be collected after the vesting date but within the same tax year. See TD 8814

RSUs – Tax Basics • At vest/release: the fair market value (FMV) of the shares is taxed as compensation income • At sale: • Increase in the FMV on stock held after release is taxed as a capital gain • Decrease in the FMV on stock held after release is taxed as a capital loss

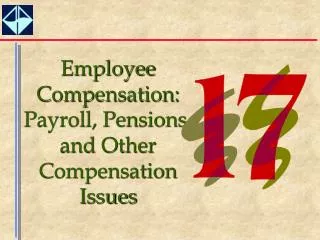

What Is The ESPP? • The ESPP allows employees who enroll to contribute post-tax payroll deductions towards the purchase of shares at a discount at the end of the six-month period • There are four main dates with regard to ESPP • Offering – the first day of the offering period during which the employee is making payroll contributions towards ESPP • There are no U.S. tax consequences • Purchase – the end of the offering period when the ESPP shares are purchased • There are no U.S. tax consequences except Pennsylvania • Sale – when the employee sells the shares acquired from the ESPP • There may be U.S. tax consequences • Termination - the employee is refunded their contributions. No purchase is made

Employee Stock Purchase Plan Example: • Fair market value on first day of offering period: $15 • Fair market value on purchase date: $20 • Purchase price: $12.75 (85% of $15) Discount $12.75 • The employee’s purchase price is the lower of • 85% of the stock price on the offering date • 85% of the stock price on the purchase date First day of offering period Purchase date

ESPP – Tax Basics • At purchase: • No income tax consequences to the employee • ESPP is not an Alternative Minimum Taxable (AMT) preference item • At sale: • The sale is a “Qualified Disposition” where the income is taxed partly as income and partly as a capital gain. The sale will be a Qualified Disposition if the employee sells the shares and meets these two conditions: • > 2 years from the offering date* • > 1 year from the date of purchase • The amount subject to income tax is the amount of the discount as calculated at the time of offering (or the actual discount if less) • If an employee does NOT hold the stock for the required periods, the disposition is referred to as a “Disqualifying Disposition” and the discount is taxed at income tax rates, up to 39.6% in 2017

ESPP – Tax Basics • At purchase, the company must • Report the ESPP purchase on Form 3922 for the year legal title transferred (usually purchase) • At sale, the company must • Report the ESPP income on Form W-2 for the year of sale • At sale, the broker must • Report the proceeds from sale of shares on Form 1099-B Note: Pennsylvania does not recognize the qualifying nature of ISOs and ESPP

ESPP – Tax Basics The company may need to report income in a year the individual was not employed by the company

Reporting And Withholding *Withholding and reporting required for PA ** Disqualifying disposition withholding required for OH

ASU 2016-09 • FASB simplification initiative • Changes include: • Share withholding flexibility} our focus today • APIC pool elimination • Changes to forfeiture rate determination • Effective for accounting periods starting on or after December 15, 2016 (public companies) • Most – but not all companies should have adopted by now • Companies can early adopt but must early adopt all aspects

ASU2016-09 Share Withholding 718-10-25-18 Similarly, a provision for either direct or indirect (through a net settlement feature) repurchase of shares issued upon exercise of options (or the vesting of nonvestedshares), with any payment due employees withheld to meet the employer’s minimum statutory withholding requirements resulting from the exercise, does not, by itself, result in liability classification of instruments that otherwise would be classified as equity. However, if anthe amount that is withheld, or may be withheld at the employee’s discretion, is in excess of the maximum statutory tax rates in the employees’ applicable jurisdictions, minimum statutory requirement is withheld, or may be withheld at the employee’s discretion, the entire award shall be classified and accounted for as a liability. That is, to qualify for equity classification, the employer must have a statutory obligation to withhold taxes on the employee’s behalf, and the amount withheld cannot exceed the maximum statutory tax rates in the employees’ applicable jurisdictions. The maximum statutory tax rates are based on the applicable rates of the relevant tax authorities (for example, federal, state, and local), including the employee’s share of payroll or similar taxes, as provided in tax law, regulations, or the authority’s administrative practices, not to exceed the highest statutory rate in that jurisdiction, even if that rate exceeds the highest rate that may be applicable to the specific award grantee.

IRS Withholding Guidance • IRS (and most state authorities) dictate the required payroll withholding rates • For stock compensation employers have two choices: • Supplemental tax rate • W-4 rate • IRS confirmed position in information letter INFO 2012-0063 • To implement share withholding at W-4 rate would be a manual process requiring separate input for each employee

NASPP Quick Survey May 2017 292 Participating Companies

T+2 Stock Settlement • SEC has changed the requirement to settle stock transactions from T+3 to T+2 from September 5 • Reduces amount of time company has to calculate tax withholding and communicate to broker by one day; impacts: • Companies who rely on payroll system to prepare a tax withholding calculation • Impact on Federal tax deposits for stock option exercises

Mobile Workforce Simplification • H.R.1393 Mobile Workforce State Income Tax Simplification Act of 2017 • Exempts employee from income tax in any state except: • The state of residence, and • The state within which the employee works more than 30 days during the calendar year • Exempts employer compliance in such circumstances • Allows employers to rely on an employee's annual determination of time expected to be working in a state • Passed by Congress June 20, 2017 • Preceded by: • H.R. 2315 (114th Congress), H.R. 1129 (113thCongress), H.R. 1864 (112thCongress), H.R. 2110 (111thCongress), H.R. 3359 (110thCongress), and H.R. 6167 (109thCongress)

Allen v. Commissioner • Allen was chief executive of Premcor and president of Tosco • Resident in and worked exclusively in Connecticut • He moved to Nevada in 2002, returning to Connecticut in 2005 for eight months • He received: • Tosco options from 1990 to 2001, and exercised them in 2002 • Premcor options in 2005 and exercised them in 2006 and 2007 • Connecticut Supreme Court ruled that the state could tax all of the income from the exercise of non-qualified stock options by a non-resident because they were granted as compensation for working in Connecticut

Contact Marlene Zobayan Rutlen Associates LLC mzobayan@rutlen.com 650-868-9282