Download

1 / 14

140 likes | 278 Views

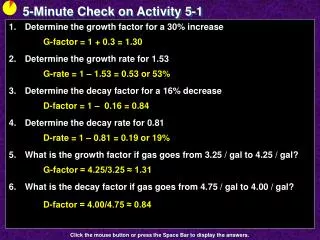

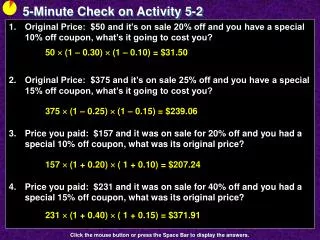

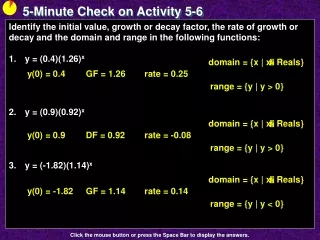

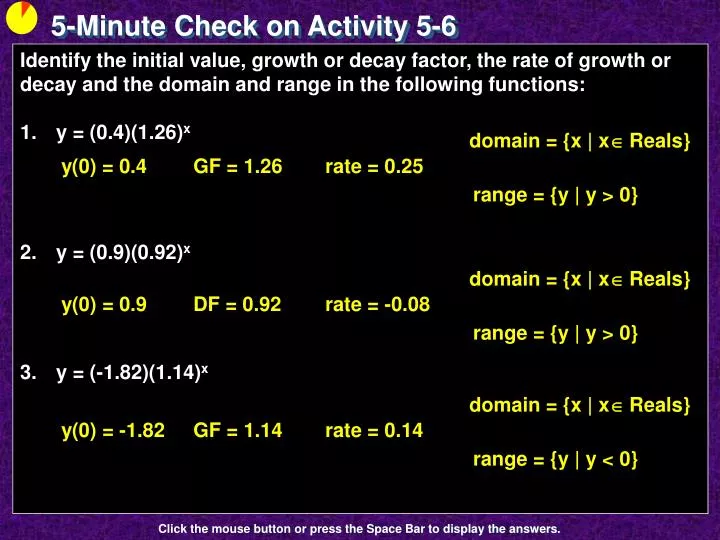

5-Minute Check on Activity 5-6. Identify the initial value, growth or decay factor, the rate of growth or decay and the domain and range in the following functions: y = (0.4)(1.26) x y = (0.9)(0.92) x y = (-1.82)(1.14) x. domain = {x | x Reals}. y(0) = 0.4. GF = 1.26. rate = 0.25.

E N D

5-Minute Check on Activity 5-6 • Identify the initial value, growth or decay factor, the rate of growth or decay and the domain and range in the following functions: • y = (0.4)(1.26)x • y = (0.9)(0.92)x • y = (-1.82)(1.14)x domain = {x | x Reals} y(0) = 0.4 GF = 1.26 rate = 0.25 range = {y | y > 0} domain = {x | x Reals} y(0) = 0.9 DF = 0.92 rate = -0.08 range = {y | y > 0} domain = {x | x Reals} y(0) = -1.82 GF = 1.14 rate = 0.14 range = {y | y < 0} Click the mouse button or press the Space Bar to display the answers.

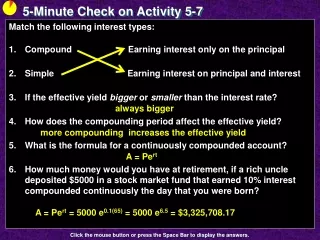

Activity 5 - 7 Time Is Money

Objectives • Distinguish between simple and compound interest • Apply compound interest formula to determine the future value of a lump-sum investment earning compound interest • Apply the continuous compounding formula A = Pert

Vocabulary • Compound Interest – interest earned is added to principal before the new interest is calculated • Future Value – the value of an amount in the future at a specific interest rate and compounding structure • Effective Yield – percentage by which the balance will grow in one year • Continuous Compounding – compounds interest each instant of time

Activity Congratulations, you have inherited $20,000! Your grandparents suggest that you save half of the inheritance for a “rainy day.” Suppose the $10,000 is deposited in a bank at 6.5% simple annual interest. What is the interest earned after 1 year? What would be the interest in 10 years? 10,000 (0.065) = 650 10,000 (0.065) 10 = 650 10 = 6,500

Simple vs Compounded Interest Simple interest means that you earn only interest on the principal over the time period invested. Compounded interest, the interest paid on most bank’s savings accounts, pays interest on the principal and the interest it has already earned. A = P(1 + r/n)nt where A is the current balance P is the principal (original deposit) r is the annual interest rate (in decimal form) n is the number of time per year interest is compounded t is the time in years the money has been invested

Simple vs Compounded Example Suppose you won (tax-free) a million dollars and deposited it in an account earning 5% interest simple interest. How much will you have after 10 years? If it was deposited in an account earning 5% compounded yearly, how much will you have after 10 years? 1,000,000 (0.05) 10 = 50,000 10 = $500,000 A = P(1 + r/n)ntA = 1,000,000(1 + .05/1)1(10) = 1,000,000(1.62889463) = 1,628,884.63 or about $628,884 in interest!

Calculate the Effective Yield Determine the growth factor (n is number of times compounded per year) b = ( 1 + r/n)n Subtract 1 from b and write the result as a decimal re = b – 1 = (1 + r/n)n – 1 Effective yield, re, will always be slightly greater than the interest rate.

Compounding Periods Determine the effective yield associated with each of the growth factors (interest rate of 6.5% with different compounding schedules) in the following table. Does the number of times compounded make a difference? Yes!

Effective Yield Example Determine the effective yields for the following rates and compounding schedules: • r = 4.5%, compounded monthly • r = 2.5%, compounded quarterly • r = 5.5%, compounded daily re = b – 1 = (1 + r/n)n – 1 = (1 + 0.045/12)12 – 1 = 4.594% re = b – 1 = (1 + r/n)n – 1 = (1 + 0.025/4)4 – 1 = 2.524% re = b – 1 = (1 + r/n)n – 1 = (1 + 0.055/365)365 – 1 = 5.653%

Continuous Compounding Compounded interest formula approaches A = P(1 + r/n)nt A = Pert as the number of times the interest is compounded approaches infinity (continuous compounding). Like a horizontal asymptote on a graph. Some banks use this method for compounding interest. e is the natural number, 2.718281828, devised by mathematician Leonhard Euler (1707-83). It is the base we will see later in the chapter for natural logarithms.

Compounding Example Calculate the balance of your $10,000 investment in 10 years with an annual interest rate of 6.5% compounded continuously What is the growth factor in this case? What is the effective yield? A = Pert A(10) = 10,000e0.065(10) = 19,155.41 b = e0.065 = 1.06716 b = e0.065 = 1.06716 re = b – 1 = 6.716%

Retirement Income Historically, investments in the stock market have yielded an average rate of 11.7% per year (over the long haul). Suppose on graduating high school a rich aunt deposits 10,000 in an account at an 11% annual interest rate that compounds continuously. She claims that you will have over a million dollars by retirement time (age 65). Is she right? 65 – 18 = 47 years A = 10,000e0.11·47 = 10,000e5.17 = 1,759,148.38 over 1.75 million Yes!

Summary and Homework • Summary • Compound interest formula: A = P(1 + r/n)ntwhere A = current balance P is the principal (original deposit) r is the annual interest rate (in decimal form) n is the number of times per year of compounding t is the time in years money is invested • Continuous compounding formula: A = Pert • If the number of compounding periods is large, then the compound interest formula can be approximated by continuous compounding formula. • Homework • pg 595 – 597; problems 1-3