Download

1 / 20

200 likes | 208 Views

What Is Russian Gas Insight ?. RGI is a multi-client report that analyzes volumes, costs and benefits of all operations with natural gas that gets into the pipeline system of Russian gas monopoly Gazprom.

E N D

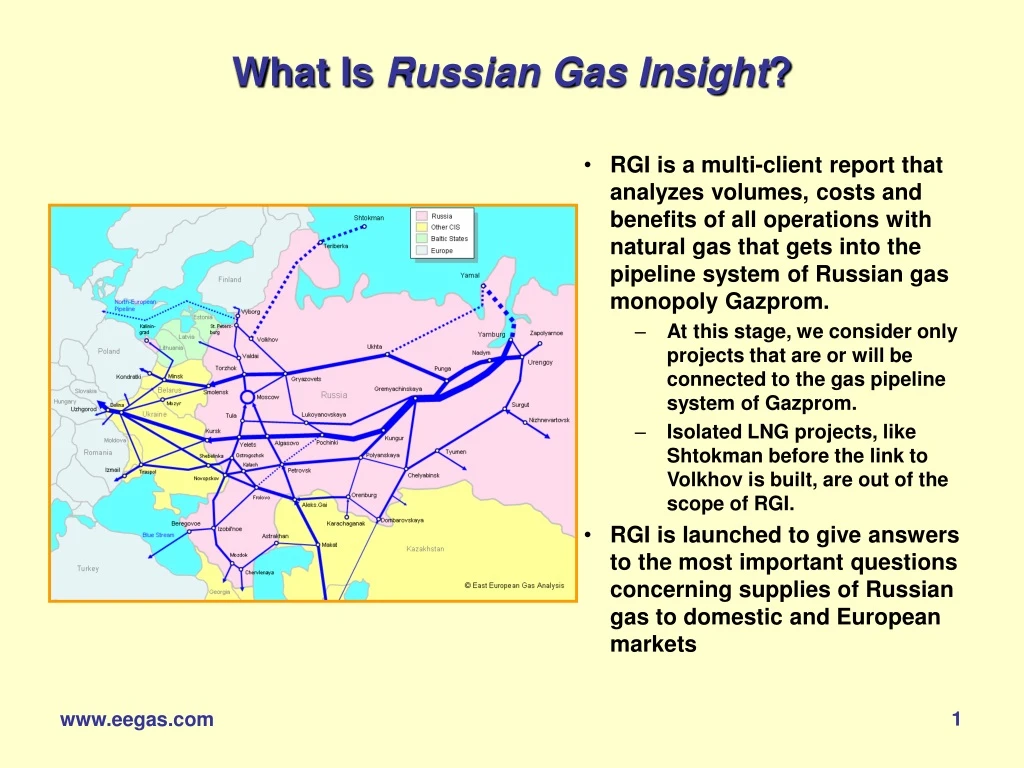

What Is Russian Gas Insight? • RGI is a multi-client report that analyzes volumes, costs and benefits of all operations with natural gas that gets into the pipeline system of Russian gas monopoly Gazprom. • At this stage, we consider only projects that are or will be connected to the gas pipeline system of Gazprom. • Isolated LNG projects, like Shtokman before the link to Volkhov is built, are out of the scope of RGI. • RGI is launched to give answers to the most important questions concerning supplies of Russian gas to domestic and European markets www.eegas.com

Answers to Key Questions • Where and at what cost is Gazprom going to get the gas volumes in 2015-2025 to meet its supply obligations and to implement its ambitious expansion plans? • Would Gazprom’s negotiating position be stronger or weaker after the expiration of existing gas export contracts to Europe? • What is the real future cost of gas delivered to Europe? • What is the difference between a rational investment plan and the investment plan of Gazprom? • Rational investment assumes Max utilization of existing capacities • Governmental agencies tend to focus on maximum spending • What are the major threats to security of supply of Russian gas to Europe? • Can Gazprom survive a drop in oil price? www.eegas.com

The Contents of RGI • Executive Summary • Part 1. Russian Gas Business Environment • Taxes, wages, prices and tariffs • Part 2. Gas Balance and Volumetric Analysis • Historic and projected sales • Production and import • Gas flows and pipeline bottlenecks • Part 3. Cost & Benefit Analysis • Production costs of Gazprom • Transmission costs • Cost of gas delivered to different markets • Profits and net cash flow • Part 4. Comments to Financial Reports of Gazprom • Part 5. RGI Focus: Russian-Ukrainian Gas Dispute www.eegas.com

Part 1. Russian Gas Business Environment • In this section, we publish updates on relevant external factors affecting Russian gas sector • Taxation, regulated domestic price of gas, regulated transmission tariffs • Cost of labor, materials and supplies • Gazprom’s relations with independent gas producers • In RGI 2006-1, we comment on the following issues • Cost of Russian labor continues to grow at a very high rate of over 30% a year (in USD terms) • Huge difference in labor cost by region and industrial sector – a 17-times difference between regions of Tyumen province, West Siberia • Weak ruble in Gazprom projections • Gazprom is strengthening control over the FSU market (the way of Standard Oil of the 1880s) Price of gas in different markets, $/mcm www.eegas.com

Part 2. Gas Balance and Volumetric Analysis • Gas consumption is addressed by region and by consumer sector • We assume a moderate growth of gas consumption in the service area of Gazprom in Russia • In 2003-2005, annual growth rate of industrial production exceeded 6%, while consumption of pipeline gas in Russia was growing 1.6% a year • High energy price will affect gas consumption in Russia • High share of gas in the fuel balance of power plants in European Russia does not give much space for growth of gas use • Efficiency improvement is a more likely way of power sector development • Gazprom plans its domestic gas sales in 2006 at the same level as in 2005 www.eegas.com

Export Projections • RGI considers only exports via Gazprom pipelines, including transit of Central Asian gas • LNG projects that are not connected to the existing pipeline system of Gazprom are out of the scope of RGI • High energy price is likely to affect gas consumption in the FSU • European exports are broken down by country and by terminal • Velke Kapusany • Drozdowichi • Beregovoe • Satu Mare • Izmail • Vyborg Finland • Brest • Kondratki • Blue Stream • Vyborg NEGP • Primorsk LNG www.eegas.com

Sample Production Forecast of Gazprom, bcm www.eegas.com

Gazprom Production Breakdown • All reservoirs are broken down by cost category • Cenomanian-1 – old low-cost giant and super-giant fields of W. Siberia • Cenomanian-2 – medium-cost West Siberian reservoirs commissioned after 2000 or to be commissioned in the future • Cenomanian-3 – high-cost fields of Yamal and Gydan peninsula • Deep & small – Neocomian, Valanginian, Achimov and other deep reservoirs of West Siberia and all fields of Severgazprom and Gazpromdobycha-Kuban’ • High sulfur – Orenburg (1.5% of H2S) and Astrakhan (25.7% of H2S) • Shtokman • In regional breakdown, net input into gas pipelines is shown by field and by company for regions of Russia www.eegas.com

Gazprom Production: Seasonal Swing • RGI addresses seasonal swing of producing branches of Gazprom • Urengoygazprom and Yamburggazdobycha have high winter peaks • West Siberian gas producers have 30% of production capacity dedicated for winter peaks • In European Russia, winter peaks of production are very small • Low well flow and high cost • Independent gas producers do not have winter peaks • The record high daily production of 1700 mmcmd, reached on January 22, 2006, discloses actual capacity of pipelines in West Siberia • We will address this issue in RGI 2006-2 www.eegas.com

Independent Gas Production Forecast Production investment requires incentives www.eegas.com

Import and Transit from Central Asia • Imports and transit are broken down by country and by terminal • Turkmenistan • Uzbekistan • Kazakhstan • Aleksandrov Gai • Karachaganak-Orenburg • Makat-Northern Caucasus • About 2 bcmy (6 mmcmd) of Central Asian gas is delivered via the old Bukhara-Urals pipeline (commissioned in 1963) • This small volume is added to the volumes delivered to Aleksandrov Gai • We expect the Bukhara-Urals pipeline to be decommissioned soon www.eegas.com

Cross-Regional Gas Flows • We calculate regional balances for regions of Russia and the FSU states • Annual balance • Daily balance (winter) • Based on historic daily flow data, we calculate daily flows across the state and regional borders from Europe to West Siberia • Spare capacity or capacity deficit is calculated for all pipeline sections by year www.eegas.com

Daily Flows and Consumption www.eegas.com

Sample Scenario: New Pipelines in 2006-2025 www.eegas.com

Part 3. Cost & Benefit Analysis • Detailed analysis of production costs by different reservoir category • Labor – Depreciation • Taxes – Interest • Other costs • Production investment requirements by reservoir category by year • Detailed analysis of transmission costs of Gazprom • Labor – Depreciation • Fuel gas – Taxes • Interest – Social cost • Other costs • Pipeline investment requirements by project and by pipe diameter, including replacement pipe • Cost of transit out of Russia • Cost of sales and cost of gas delivered to different markets • Gazprom’s profit by market segment and net cash flow from gas operations Anything can fly at $70/bbl www.eegas.com

Sample Cash Flow Projections • Growth of internal costs of Gazprom is more dangerous than a drop in oil price • Base Case assumes that internal costs grow 25% in 2006 and 10% in 2007-2008 • High Cost Case (red line) assumes that in 2006-2008 cost growth rate is 10% higher • In 2009-2025, cost growth rate is the same for both cases • We believe that Base Case assumptions are too optimistic • Cost of Gazprom are more likely to follow the High Cost scenario • NPV of net cash flow from gas operations under Base Case is $71 billion versus $45 billion of the High Cost Case (at 10% discount rate) www.eegas.com

Part 4. Comments to Financial Reports • Financial reports of Gazprom are transparent enough to reveal some serious discrepancies • Expenses of production and transmission segments of Gazprom are reported inaccurately • Very often quarterly and accrual numbers do not add up with the difference reaching $200 million • Current negligence in financial reporting is unacceptable • Since January 2004, Gazprom is effectively overpaying export duties by over $0.7 billion a year • Recent deal with RosUkrEnergo shows that Gazprom could legally cut payments of export duties • Reports indicate that Gazprom gives unfair advantages to RosUkrEnergo • The risk of successful lawsuits from Western shareholders of Gazprom is extremely high Gazprom reported the growth of tax payment as one of its major achievements in 2004 (Gazprom: Annual Report 2004, page 9) Source: www.gazprom.ru www.eegas.com

Part 5. Russian-Ukrainian Gas Dispute • Shareholders of Gazprom benefited from giving Ukrainian exports to Itera in 1998 • Many analysts believe the opposite • Sales of transit services to Itera were a way more profitable for Gazprom than deliveries of gas to Ukraine without being paid • Eural Trans Gas was and RosUkrEnergo is a loss for Gazprom • A fully-owned foreign subsidiary of Gazprom, like ZMB, could have been a better intermediary for all shareholders of Gazprom, including the state • Gazprom gives RUE a huge profit margin • In Jan-Sep-2005, RUE made a profit of $500 million with half of it transferred to private accounts in Switzerland • Apparently, the most profitable business – exports of Kazakh gas to Europe – formerly run by ZMB, is now given to RUE • Now RUE is making a daily profit of $6 million • Russian and Gazprom officials insist on RUE staying in business • The new transit agreement causes Gazprom a loss of about $1 billion a year. www.eegas.com

Dominating Political Factors Increase Uncertainty of Supplies of Russian Gas • For the first time in the history of gas exports, Russia deliberately stopped the gas flow • The gas transit conflict with Ukraine has caused an economic loss to Gazprom • The conflict is far from being solved • Russia’s vision of the future of European gas markets is absolutely different from European views • Gazprom would like to have a Standard Gas Company of Europe (like Standard Oil) controlled by Gazprom • President Putin’s vision of European gas market is explained in his letter (“Energy egotism – road to nowhere”) • Competition is counterproductive • Gas price should be regulated • Lack of competition leads to inefficiency • Are European consumers supposed to pay for Gazprom’s inefficiency? www.eegas.com

RGI keeps our clients on top of important events in Russian gas business www.eegas.com