Download

1 / 12

120 likes | 324 Views

Exchange Rate Determination in the Short Run. ECON 758 Advanced International Economics Dr. Jeffery Heinrich. Agenda. develop basic demand/supply model for foreign exchange define effective rate of return, and show how to compare returns on assets priced in different currencies

E N D

Exchange Rate Determination in the Short Run ECON 758 Advanced International Economics Dr. Jeffery Heinrich

Agenda • develop basic demand/supply model for foreign exchange • define effective rate of return, and show how to compare returns on assets priced in different currencies • equilibrium: define and explore the Covered Interest Parity condition • see how money demand and monetary policy influence rates of return and exchange rates

Basics: Demand • Demand for foreign exchange • to buy things denominated in it (goods, services, or assets) • to hold interest-bearing accounts in that currency • greater quantity demanded at lower price/exchange rate • Non-price Determinants of Demand. • increased (decreased) demand for foreign G&S • increased (decreased) domestic income • lower (higher) relative price levels for G&S denominated in currency • increased (decreased) relative return on assets denominated in foreign currency

Basics: Supply • Supply of foreign exchange: wanting to sell a currency • greater quantity supplied at higher price/exchange rate • People wanting to sell more (less) of a currency at any given XR is an increase (decrease) in supply • change in foreign income • change in relative price levels • change in relative rate of return on domestic assets

Equilibrium • Equilibrium XR where QD = QS • Shifts in D or S change XR • what happens if foreign goods get more costly? • what happens if US income falls? • Will $ prices of foreign goods fully reflect changes in XR? i.e., how complete is passthru?

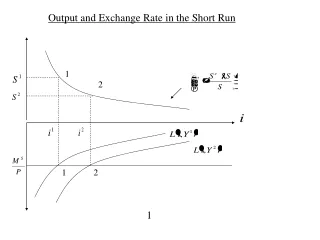

The Assets Approach to Exchange Rates • FX turnover far more than necessary for purchasing output FX mostly to purchase assets, incl. foreign currency! Process of interest arbitrage. • What determines demand for foreign currency deposits? Effective Rate of Return! • rate of return on the deposit • expected change in domestic currency value of foreign currency • simple interest rates insufficient ~ may be higher UK interest rate on £, but what if £ loses value against $? • uncertainties in predicting future value of any asset • risk and liquidity premiums

Determining Interest Rates: The Market for Money • Exchange Rate is a Relative Price of Monies! • Money • medium of exchange; unit of account; store of value • Supply ~ assume Central Bank controls MS • Demand (MD) ~ money only held for liquidity! • R = opportunity cost of money, i.e., the interest rate • P = price level of output (hold fixed for SR) • Y = real nat’l income • L(R,Y) = real aggregate money demand • L(R,Y) = MD/P

Comparing ERR across currencies • Nomenclature • R = rate of return on home currency • R* = rate of return on foreign currency • E = current spot rate (units home currency per unit foreign currency) • F = expected future spot rate (hold fixed for SR) • Leave out risk, liquidity factors (for now) • Return on home currency deposit $1 = $(1+R) ~ ERR$ = R • Return on foreign currency deposit of initial value of $1 • get 1/E units foreign currency • foreign currency return of (1+R*)/E • convert to home currency, get F(1+R*)/E dollars • ERR* = R* + (F-E)/E + R*·(F-E)/E • last term likely small for economies with stable currencies, low interest rates

Covered Interest Parity (CIP) • ERR$ = R; ERR* = R* + (F-E)/E = R* + expected%E • intuition: ERR on foreign deposit is the rate of change in the foreign currency value of the deposit (R*), plus the forward premium on the foreign currency [(F-E)/E ] (or expected rate of depreciation of $) • Example: R$ = .06, R* = .03, (Ee-E)/E = .04 • $ pays higher interest rate than FX, but the forward premium on foreign currency more than compensates for the lower foreign rate. • Equilibrium E: all deposits offer same ERR • Covered Interest Parity • CIP condition: R = R* + (F-E)/E • no incentive to buy or sell deposits of any currency ~ no change in demand or supply of currencies! • R* = R - (Ee-E)/E or R – R* = (F-E)/E • Uncovered Interest Parity (UIP)

Using CIP • Domestic and foreign money markets jointly determined XR! • Relevant Variables • domestic and foreign income • domestic and foreign price levels • domestic and foreign money supplies • expected future exchange rates/forward rate

Using CIP, cont. • What happens if foreign income falls? • foreign money demand , R* , need larger fwd prem. on FX…E ($ appr, FX depr) • spot rates tend to change with interest rates! • What happens if fwd rate increases? • no change in R or R*, so fwd prem must be unchanged…spot rate changes same amount • changes in expectations tend to manifest now! • If US R = 0.045, foreign R* = 0.07, what is fwd prem on FX? • FX is at fwd discount of 0.025 (2.5% expected depr)

Agenda • develop basic demand/supply model for foreign exchange • define effective rate of return, and show how to compare returns on assets priced in different currencies • equilibrium: define and explore the Covered Interest Parity condition • see how money demand and monetary policy influence rates of return and exchange rates • on to Module 2A – Exchange Rates in the Long Run