Download

1 / 16

160 likes | 323 Views

Inflation & Growth. Parthasarathi shome director & CE , ICRIER. How important is the inflation-growth tradeoff ?.

E N D

Inflation & Growth Parthasarathi shomedirector & CE, ICRIER

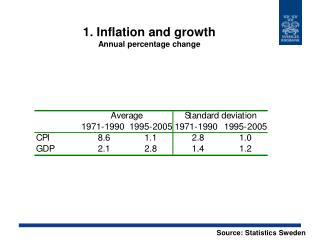

How important is the inflation-growth tradeoff? • The long-run rate of growth is determined by real factors: technical progress, demographics and the savings rate. Inflation on the other hand is a monetary phenomenon. Prima facie we expect them not to be related. • We can think of some qualifications, of course: • Inflation is a tax on money holders. A change in the rate of inflation can therefore change wealth-holders’ preference between holding their wealth in the form of money or in the form of real assets and thus affect the growth rate. However, given the small proportion of total wealth which is held in the form of money, such effects are likely to be small. • Inflation volatility increases uncertainty in a money-using economy thereby increasing the riskiness of investment projects and affecting the growth rate adversely. However, apart from hyperinflationary situations the additional inflation risk is likely to be small compared to other sources of risk such as exchange rate variations, labour or infrastructure environment, or political and climate uncertainty. • Inflation makes debtors better off because debt repayment now imposes a smaller burden in real terms. For the same reason it makes creditors worse off. Any increase in expenditure by the former would be cancelled in part by the decrease in expenditure by the latter and only the small residual that would remain one way or the other would affect growth. • If the tax system imposes taxes at different rates based on money income, inflation changes the burden of taxes Rising money income puts people in higher tax slabs even though the real purchasing power of that income might have been eroded in the meanwhile by inflation.This effect would persist till the time tax slabs are revised. This effect is also likely to be small except in hyperinflation. • Thus, for moderate rates of inflation, the rate of inflation is unlikely to be related to the rate of long-run growth.

Growth vs. Inflation: India, 1951-2011 The Indian evidence above shows the lack of any simple unidirectional relationship between inflation and growth.

The short-run inflation-output tradeoff Demand-side inflationary pressures arise from excess demand pushing actual output above the economy’s long-term output level, raising the marginal cost of production of firms. Firms in turn raise prices to cover their marginal costs. Cost-side inflationary pressures come from rising prices of domestic raw materials and imported goods.

The role of expectations Inflationary pressures determine the rate of change of the inflation rate. Excess demand accelerates the rate of inflation compared to the expected rate of inflation. Deficient demand slows it down. Even without any demand-side or cost-side pressures firms increase prices if they expect other firms to do so … ... workers press for increase in their wages if they expect other workers to receive higher wages and firms to increase prices. Managing inflationary expectations is essential for inflation control. For example, following an oil price shock, if firms expect monetary policy to accommodate the shock they would immediately raise the price of non-oil commodities even before the exhaustion of their existing oil stocks.

Monetary policy and the management of expectations Monetary policy affects inflation through its effect on aggregate demand. Since inflation today depends on inflation expected tomorrow, what matters is not just today’s policy but also the expected policy response to future events. The policy regime matters more than particular decisions. A credible anti-inflationary stance makes monetary policy more effective by anchoring inflationary expectations. If the monetary authority is seen as being committed to its inflation targets there is much less danger of a temporary inflation shock turning into a persistent wage-price spiral. On the other hand, if the monetary authority is seen as being willing to accommodate inflationary pressures, the private sector begins to expect any inflationary trend to persist and it becomes harder to fight inflation.

The course of monetary policy The RBI has raised the repo rate* 10 times and by 275 basis points since March 2010. Between 2009-10 and 2010-11 the WPI inflation rate has gone up by 576 basis points from 3.80% to 9.56%. By not responding aggressively enough to inflationary pressures the RBI faces the risk of inflationary expectations becoming entrenched. While the RBI’s cautious approach has avoided a major negative impact on output and employment right now, it creates the risk of having to pay a much larger price in lost output later when it has to fight the inflationary expectations which are becoming entrenched now. A policy of easy money does not bring any growth dividend in the long-run since actual output cannot be kept above the economy’s productive capacity permanently and the growth of productive capacity is determined by real and not monetary forces. * The repo rate is the rate at which the RBI lends money to commercial banks.

External constraints on monetary policy • The short-run interest rates in the US are close to zero. The long-run rates have been pushed down by the two rounds of quantitative easing. • Pursuit of an anti-inflationary high interest rate policy in India would lead to destabilising capital inflows and appreciation pressures on the Rupee. • The RBI faces the classic trilemma, One cannot have • fixed exchange rates, • free capital flows • and monetary policy autonomy at the same time. • The RBI can counter the inflows by allowing the Rupee to appreciate continuously. But continuing appreciation of the Rupee would hurt competitiveness and may not still solve the inflow problem given the unpredictability of foreign investor sentiment.

Recent inflation driven by food prices? Growing demand for agricultural products arising from growing income. Agricultural output growth slower than overall output growth. A severe drought in 2009-10. Demand-supply mismatch raises the relative price of agricultural products. If other prices cannot adjust downward, absolute prices of agricultural products must rise.

The relative price of food: India, 1994-2010 The relative price of food is computed as the ratio of the WPI component for primary food commodities to an index of non-food manufacturing prices computed from WPI data.

Food price rise cannot explain all of current inflation • Between 2009-10 and 2010-11 WPI inflation was 17.7% for primary products; 12.3% for fuel, power, light and lubricants; and 5.7% for manufactured products. • The overall inflation rate was 9.6%. • How much of this inflation was contributed by primary products? • Suppose: • Manufactured product prices were to remain constant. • Inflation in fuel, power, light and lubricants was to still be 12.3%. • The overall inflation rate would then be only 4.6%. • This can be thought of as the contribution of primary products to overall inflation.

External constraints: correlation between domestic and world food prices

World Wheat Prices vs. MSP* *MSP: Minimum Support Price. A floor price set by the Government of India. Data sources: World-IMF; India-FCI

Monthly Wheat Prices (World vs. India) Sources: World-IMF; India-MCX Ltd.

Policy recommendations: short-run • In the short-run the RBI should raise interest rates sharply to protect its anti-inflationary credibility. • Fiscal consolidation to ensure that fiscal policy does not work at cross-purposes with monetary policy. • A loose fiscal policy, by increasing the debt burden both directly and through its effect on interest rates, would prove to be unsustainable in the long run • As the debt burden rises, the pressure to print money to finance the fiscal deficit would rise, thereby making it impossible to pursue an anti-inflationary monetary policy.

Policy recommendations: long-run Investment in infrastructure and human capital to ensure that desired growth does not exceed the productive capacity of the economy. Investment and promotion of organizational innovations in agriculture to ensure that food supply does not become a bottleneck to growth. Moving towards greater independence for the central bank and transparency in monetary policy to stabilise inflationary expectations. A policy debate on the possibility of imposing selective capital controls to augment RBI’s policy space.