Download

1 / 32

320 likes | 456 Views

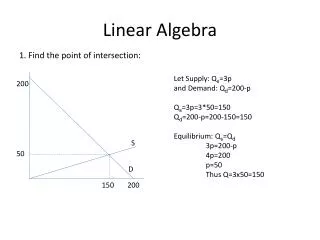

Numerical Linear Algebra in the Streaming Model. Ken Clarkson - IBM David Woodruff - IBM. The Problems. Given n x d matrix A and n x d’ matrix B , we want estimators for The matrix product A T B The matrix X * minimizing ||AX-B||

E N D

Numerical Linear Algebra in the Streaming Model Ken Clarkson - IBM David Woodruff - IBM

The Problems Given n x d matrix A and n x d’ matrix B, we want estimators for • The matrix product AT B • The matrix X* minimizing ||AX-B|| • A slightly generalized version of linear regression • Given integer k, the matrix Ak of rank k minimizing ||A-Ak|| • We consider the Frobenius matrix norm: square root of sum of squares

General Properties of Our Algorithms • 1 pass over matrix entries, given in any order (allow multiple updates) • Maintain compressed versions or “sketches” of matrices • Do small work per entry to maintain the sketches • Output result using the sketches • Randomized approximation algorithms • Since we minimize space complexity, we restrict matrix entries to be O(log nc) bits, or O(log nd) bits

Matrix Compression Methods • In a line of similar efforts… • Element-wise sampling [AM01], [AHK06] • Row / column sampling: pick small random subset of the rows, columns, or both [DK01], [DKM04], [DMM08] • Sketching / Random Projection: maintain a small number of random linear combinations of rows or columns [S06] • Usually more than 1 pass • Here: sketching

Outline • Matrix Product • Linear Regression • Low-rank approximation

An Optimal Matrix Product Algorithm • A and B have n rows, and a total of c columns, and we want to estimate ATB, so that ||Est-ATB|| ·ε||A||¢||B|| • Let S be an n x m sign (Rademacher) matrix • Each entry is +1 or -1 with probability ½ • m small, set to O(log 1/ δ) ε-2 • Entries are O(log 1/δ)-wise independent • Observation: • E[ATSSTB/m] = ATE[SST]B/m = ATB • Wouldn’t it be nice if all the algorithm did was maintain STA and STB, andoutput ATSSTB/m?

An Optimal Matrix Product Algorithm • This does work, and we are able to improve the previous dependence on m: • New Tail Estimate: for δ, ε > 0, there is m = O(log 1/ δ) ε-2so that Pr[||ATSSTB/m-ATB|| > ε ||A|| ||B||] ·δ (again ||C|| = [Σi, j Ci, j2]1/2) • Follows from bounding O(log 1/δ)-th moment of ||ATSSTB/m-ATB||

Efficiency • Easy to maintain sketches given updates • O(m) time/update, O(mc log(nc)) bits of space for STA and STB • Improves Sarlos’ algorithm by a log c factor. • Sarlos’ algorithm based on JL Lemma • JL preserves all entries of ATB up to an additive error, whereas we only preserve overall error • Can compute [ATS][STB]/m via fast rectangular matrix multiplication

Matrix Product Lower Bound • Our algorithm is space-optimal for constant δ • a new lower bound • Reduction from a communication game • Augmented Indexing, players Alice and Bob • Alice has random x 2 {0,1}s • Bob has random i 2 {1, 2, …, s} • also xi+1, …, xs • Alice sends Bob one message • Bob should output xi with probability at least 2/3 • Theorem [MNSW]: Message must be (s) bits on average

Lower Bound Proof • Set s := £(cε-2log cn) • Alice makes matrix U • Uses x1…xs • Bob makes matrix U’ and B • Uses i and xi+1, …, xs • Alg input will be A:=U+U’ and B • A and B are n x c/2 • Alice: • Runs streaming matrix product Alg on U • Sends Alg state to Bob • Bob continues Alg with A := U + U’ and B • ATB determines xi with probability at least 2/3 • By choice of U, U’, B • Solving Augmented Indexing • So space of Alg must be (s) = (cε-2log cn) bits

Lower Bound Details • U = U(1); U(2); …, U(log(cn)); 0s • Each U(k)is an£(ε-2) x c/2 submatrix with entries in {-10k, 10k} • U(k)i, j = 10k if matched entry of x is 0, else U(k)i, j = -10k • Bob’s index i corresponds to U(k*)i*, j* • U’ is such that A = U+U’ = U(1); U(2); …, U(k*); 0s • U’ is determined from xi+1, …, xs • ATB is i*-throw of U(k*) • ||A|| ¼ ||U(k*)|| since the entries of A are geometrically increasing • ε2||A||2¢ ||B||2, the squared error, is small, so most entries of the approximation to ATB have the correct sign

Outline • Matrix Product • Linear Regression • Low-rank approximation

Linear Regression • The problem: minX ||AX-B|| • X* minimizing this has X* = A-B, where A- is the pseudo-inverse of A • Every matrix A = UΣVT using singular value decomposition (SVD) • If A is n x d of rank k, then • U is n x k with orthonormal columns • Σis k x k diagonal matrix, diagonal is positive • V is d x k with orthonormal columns • A- = VΣ-1UT • Normal Equations: ATA X = ATB for optimal X

Linear Regression • Let S be an n x m sign matrix, m = O(dε-1log(1/δ)) • The algorithm is • Maintain STA and STB • Return X’ solving minX ||ST(AX-B)|| • Space is O(d2ε-1log(1/δ)) words • Improves Sarlos’ space by log c factor • Space is optimal via new lower bound • Main claim: With probability at least 1- δ, ||AX’-B|| · (1+ε)||AX*-B|| • That is, relative error for X’ is small

Regression Analysis • Why should X’ solving minX ||ST(AX-B)|| be good? • ST approximately preserves AX-B for fixed X • If this worked for all X, we’re done • ST must preserve norms even for X’, chosen using S • First reduce to showing that ||A(X*-X’)|| is small • Use normal equation ATAX* = ATB • Implies ||AX’-B||2 = ||AX*-B||2 + ||A(X’-X*)||2 • Bounding ||A(X’-X*)||2 equivalent to bounding ||UTA(X’-X*)||2, where A = UΣVT, from SVD, and U is an orthonormal basis of the columnspace of A

Regression Analysis Continued • Bounding ||¯||2 := ||UTA(X’-X*)||2 • ||¯|| · ||UTSSTU¯/m|| + ||UTSSTU¯/m-¯|| • Normal equations in sketch space imply (STA)T(STA)X’ = (STA)T(STB) • UTSSTU¯ = UTSSTA(X’-X*) = UTSSTA(X’-X*) + UTSST(B-AX’) = UTSST(B-AX*) • || UTSSTU¯/m|| = ||UTSST(B-AX*)/m|| · (ε/k)1/2||U||¢||B-AX*|| (new tail estimate) = ε1/2 ||B-AX*||

Regression Analysis Continued • Hence, ||¯||2 := ||UTA(X’-X*)||2 • ||¯|| · ||UTSST¯/m|| + ||UTSSTU¯/m-¯|| · ε1/2 ||B-AX*|| + ||UTSSTU¯/m-¯|| • Recall the spectral norm: ||A||2 = supx ||Ax||/||x|| • Implies ||CD|| · ||C||2 ||D|| • ||UTSSTU¯/m-¯|| · ||UTSSTU/m-I ||2 ||¯|| • Subspace JL: for m = (k log(1/δ)), STapproximately preserves lengths of all vectors in a k-space • ||UTSSTU¯/m-¯|| · ||¯||/2 • ||¯|| · 2ε1/2||AX*-B|| • ||AX’-B||2 = ||AX*-B||2 + ||¯||2 = ||AX*-B||2 + 4ε||AX*-B||2

Regression Lower Bound • Tight (d2 log (nd) ε-1) space lower bound • Again a reduction from augmented indexing • This time more complicated • Embed log (nd) ε-1independent regression sub-problems into hard instance • Uses deletions and geometrically growing property, as in matrix product lower bound • Choose the entries of A and b so that the algorithm’s output x encodes some entries of A

Regression Lower Bound • Lower bound of (d2) already tricky because of bit complexity • Natural approach: • Alice has random d x d sign matrix A-1 • b is a standard basis vector ei • Alice computes A = (A-1)-1 and puts it into the stream. Solution x to minx ||Ax=b|| is i-th column of A-1 • Bob can isolate entries of A-1, solving indexing • Wrong:A has entries that can be exponentially small!

Regression Lower Bound • We design A and b together (Aug. Index) 1 A1, 2 A1, 3 A1, 4 A1,5 0 1 A2, 3 A2, 4 A2,5 0 0 1 A3, 4 A3,5 0 0 0 1 A4,5 0 0 0 0 1 x1 x2 x3 x4 x5 0 A2,4 A3,4 1 0 = x5 = 0, x4 = 1, x3 = 0, x2 = 0, x1 = -A1,4

Outline • Matrix Product • Regression • Low-rank approximation

Best Low-Rank Approximation • For any matrix A and integer k, there is a matrix Ak of rank k that is closest to A among all matrices of rank k. • Since rank of Ak is k, it is the product CDTof two k-column matrices C and D • Ak can be found from the SVD (singular value decomposition), where C and D are orthogonal matrices U and VΣk • This is a good compression of A • LSI, PCA, recommendation systems, clustering

Best Low-Rank Approximation • Previously, nothing was known for 1-pass low-rank approximation and relative error • Even for k = 1, best upper bound O(nd log (nd)) bits • Problem 28 of [Mut]: can one get sublinear space? • We get 1-pass and O(kε-2(n+dε-2)log(nd)) space • Update time is O(kε-4), so total work is O(Nkε-4), where N is the number of non-zero entries of A • New space lower bound shows optimal up to 1/ε

Best Low-Rank Approximation and STA • The sketch STA holds information about A • In particular, there is a rank k matrix Ak’ in the rowspace of STA nearly as close to A as the closest rank k matrix Ak • The rowspace of STA is the set of linear combinations of its rows • That is, ||A-Ak’|| · (1+ε)||A-Ak|| • Why is there such an Ak’?

Low-Rank Approximation via Regression • Apply the regression results with A ! Ak, B ! A • The X’ minimizing ||ST(AkX-A)|| has ||AkX’-A||· (1+ ε)||Ak X*-A|| • But here X* = I, and X’ = (ST Ak)- STA • So the matrix AkX’ = Ak(STAk)-STA: • Has rank k • In the rowspace of STA • Within 1+εof smallest distance of any rank-k matrix

Low-Rank Approximation in 2 Passes • Can’t use Ak(STAk)- STA without finding Ak • Instead: maintain STA • Can show that if GT has orthonormal rows, then the best rank-k approximation to A in the rowspace of GT is A’kGT, where A’k is the best rank-k approximation to AG • After 1st pass, compute orthonormal basis GT for rowspace of STA • In 2nd pass, maintain AG • Afterwards, compute A’k and A’kGT

Low-Rank Approximation in 2 Passes • A’k is best rank-k approximation to AG • For any rank-k matrix Z, • ||AGGT – A’kGT|| = ||AG-A’k|| · ||AG-Z|| · ||AGGT – ZGT|| • For all Y: (AGGT-YGT) ¢ (A-AGGT)T = 0, so we can apply Pythagorean Theorem twice: • ||A – A’kG|| = ||A-AGGT|| + ||AGGT – A’kGT|| · ||A-AGGT|| + ||AGGT – ZGT|| = ||A – ZGT||

1 Pass Algorithm • With high probability,(*) ||AX’-B|| · (1+ε)||AX*-B||, where • X* minimizes ||AX-B|| • X’ minimizes ||STAX-STB|| • Apply (*) with A ! AR and B ! A and X’ minimizing ||ST(ARX-A)|| • So X’= (STAR)-STA has ||ARX’-A|| · (1+ε)minX ||ARX-A|| • Columnspace of AR contains a (1+ε)-approximation to Ak • So, ||ARX’-A|| · (1+ε)minX ||ARX-A|| · (1+ε)2 minX ||A-Ak|| • Key idea: ARX’ = AR(STAR)-STA is • easy to compute in 1-pass with small space and fast update time • behaves like A (similar to SVD) • use it instead of A in our 2-pass algorithm!

1 Pass Algorithm • Algorithm: • Maintain AR and STA • Compute AR(STAR)-STA • Let GT be an orthonormal basis for the rowspace of STA, as before • Output the best rank-k approximation to AR(STAR)-STA in the rowspace of STA • Same as 2-pass algorithm except we don’t need a second pass to project A onto the rowspace of STA • Analysis is similar to that for regression

A Lower Bound binary string x matrix A index i and xi+1, xi+2, … k ε-1 columns per block 0s k rows 0, 0 0, 0 0, 0 … … -1000, -1000 -1000, 1000 1000, 1000 … … 10000, -10000 -10000, -10000 -10000, -10000 … … 0, 0 0, 0 0, 0 … … … … … … … 0 0 … … … 10, -10 -10, 10 -10,-10 … … -100, -100 100, 100 100, 100 … … n-k rows Error now dominated by block of interest Bob also inserts a k x k identity submatrix into block of interest

Lower Bound Details Block of interest: k ε-1 columns k rows 0s P*Ik 0s n-k rows * Bob inserts k x k identity submatrix, scaled by large value P Show any rank-k approximation must err on all of shaded region So good rank-k approximation likely has correct sign on Bob’s entry

Concluding Remarks • Space bounds are tight for product, regression • Sharpen prior upper bounds • Prove optimal lower bounds • Space bounds off by a factor of ε-1 for low-rank approximation • First sub-linear (and near-optimal) 1-pass algorithm • We have better upper bounds for restricted cases • Improve the dependence on εin the update time • Lower bounds for multi-pass algorithms?