Download

1 / 40

400 likes | 576 Views

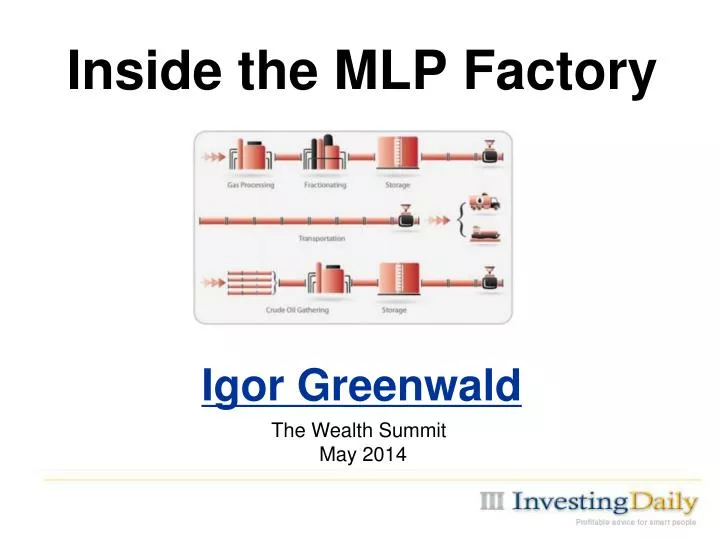

Inside the MLP Factory. Igor Greenwald. The Wealth Summit May 2014. Do You Like Sausage?. I know I do; let me count the ways:. Grilled, with onions Smoked with sauerkraut On a stick, fried in pancake batter (Not really, but someone out there does.).

E N D

Inside the MLP Factory Igor Greenwald The Wealth Summit May 2014

I know I do; let me count the ways: • Grilled, with onions • Smoked with sauerkraut • On a stick, fried in pancake batter (Not really, but someone out there does.)

What does sausage have to do with master limited partnerships? Only this: The end result is much more appealing than the preparation process

Why the bad rap for sausage factories? Blame this man: “If you like laws and sausages, You should never watch either one being made.” ─ Otto von Bismarck, maybe Another thing The Iron Chancellor probably didn’t say: “If you like pithy quotes, don’t worry too much about attribution.”

How are MLPs like laws and sausages? • Complex process • Assembled by specialists • Defects hard to spot • Fill a need for the public • Producers can profit by fooling consumers

The insinuation: If only you knew “The $500 billion master-limited-partnership sector is the sausage maker of the investment world. Buyers love the yields ─ now averaging about 6% ─but many know little about how the yields are generated. And Kinder Morgan, the country's largest energy-infrastructure company, may be the biggest sausage maker of them all.” “Kinder Morgan: Trouble in the Pipelines?” Barron’s, Feb. 22, 2014

And yet, here’s what we know: • Sausage is tasty • Laws keep anarchy at bay • MLPs have been the best investment so far in this century

How Fresh Is That Sausage? • Past performance does not predict future • Outperformance won’t last forever • Risk of reversion rises over time • The role of sentiment in market cycles

Reality Check Source: William Blair

The People’s Choice • Predictable tax-deferred income • Exempt from corporate income tax • Long-term contracts, regulated tariffs • Yield above bonds, REITs, utilities • Growth industry amid US shale boom • Great long-term track record

No Contest Source: Alerian

Drill, Baby, Drill Projected US energy production Source: US Energy Information Administration

Moveable Feast Government shale forecasts keep missing low Source: RBN Energy

Good Times, Not So Bad Times Selected Alerian MLP Index annual returns since 1996 Five Best Years 2009: 76% 2000: 46% 2003: 45% 2001: 44% 2010: 36% Five Worst Years 2008: -37% 1999: -8% 2002: -3% 1998: -3% 2012: 5% Sources: Alerian, Hinds Howard

MLP Bulls Come Lately New investment vehicles by year of launch

Drilling for Cheap Capital Source: Hinds Howard

C-Corps♥Selling MLPs Recent Spinoffs: • Phillips 66 Partners (PSXP) from Phillips 66 (PSX) – top ‘13 MLP IPO • Valero Energy Partners (VLP) from Valero Energy (VLO) • Western Refining Logistics (WNRL) from Western Refining (WNR) • EnLink Midstream Partners (ENLK) from Devon (DVN) and Crosstex (XTXI) • Enable Midstream (ENBL) from CenterPoint (CNP) and OGE Energy (OGE) More In Store: • Dominion Midstream LNG MLP from Dominion (D) • Antero Resources Midstream MLP from Antero Resources (AR) • LNG tanker MLP from GasLog (GLOG) • Offshore drilling rig MLP from Transocean (RIG) • LNG processing MLP from Energy Transfer Equity (ETE)

MLP Alchemy • Devon valued (still!) at less than 5x EV/EBITDA • Deal valued auxiliary midstream assets at 11x EBITDA • Devon’s contribution to MLP valued at $4.8 billion • Market has since repriced to more than $7 billion, or 16x EBITDA • MLP trading at three timesDevon’s cash flow multiple

PSX vs. PSXP The high cost of the extra “P” PSX EV = $49.3B EBITDA = $3.4B EV/EBITDA = 14.5 PSXP EV = $3.5B EBITDA = $67.7M EV/EBITDA = 51.7 • PSX owns 72% of PSXP LP units plus 2% GP interest • Investors paying more than triple for PSXP over PSX • Fast distribution growth is nice, but at 1.6% yield, not fast enough • PSXP up 93% in 9 months since IPO, 48% year-to-date • Troubling faith in perpetual growth

Bonds Have More Fun Why comparisons with credit yields may prove misleading • Fixed income in fourth decade of bull market • Government bonds don’t have business risk • On plus side, bond coupons don’t grow like MLP payouts • If rates rise, MLP yields could follow via capital losses

What’s WrongWith This Picture? • Anchoring bias assumes starting price is the right one • No guarantee distribution growth builds partnership value • No guarantee yield is justified by business prospects • Many MLPs are beyond reproach and have very bright prospects, but the exceptions to this rule can be very costly

The MLP Profits Philosophy • We recommend investments, not tax shelters • We do so based on long-term fundamentals, not yield • We’re bullish on many strong MLPs and GPs • But we’re also not afraid to sell and criticize • Or to admit mistakes and change course

Strong Performance Record • Last year’s picks returned nearly 40% annualized by year-end • Portfolio comfortably beat MLP benchmark as well as S&P 500 Timely buys: Energy Transfer Equity (ETE) +66% since 6/7/13 EQT Midstream Partners (EQM) +64% since 8/12/13 Sunoco Logistics Partners (SXL) +42% since 8/12/13 Targa Resources (TRGP) +35% since 11/15/13 Timely sells: Eagle Rock Partners (EROC) -49% since 5/29/13 Boardwalk Pipeline Partners (BWP) -42% since 11/15/13 Timely re-buys: Boardwalk Pipeline Partners (BWP) +15% since 4/4/14

Key MLP Profits Growth Themes • LPG Exports (EPD, TRGP, NGLS) • LNG Exports (ETE, WMB, KMI, TGP) • Oil, Fuels Surge (MMP, SXL, BPL, OILT) • Northeast Energy (EQM, WMB, MWE) • GPs With IDRs (ETE, KMI, WMB, AHGP) • Propane Logistics (APU, NGL)

A Margin Of Safety Top 3 Best Buys (EPD, MMP, SXL) averaged excess coverage of more than 50% of distributions at end of 2013 Excess coverage can fund capital projects in place of equity/debt issuance, aiding returns Top 3 up 16% YTD, 38% in year before yield

Let’s Talk Incentives Incentive Distribution Rights (IDRs) pay general partner (GP) growing percentage of MLP cash flow Typical: 15% of payout above X, 25% above Y, 50% above Z, per unit Stated rationale: incents GP to grow MLP Unmentioned: dilutes rewards of growth for limited partners Perverse: Top hedge funders charge 2/20 fees; many GPs 2/50 Means GP can profit even from losing investment; fund with debt then collect almost 50% of notional cash flow boost. A sweet deal. Or fund with equity and collect extra IDRs on new units long before any return. Also why some GPs turn their MLPs into serial acquirers IDRs can have huge effect on returns and are main reason we tend to favor GPs over affiliated MLPs

In Summary • MLPs in sweet spot of domestic energy boom • Lofty valuations suggest increased risk • Downside from higher rates, lower energy prices • Returns can be tasty, but insiders eat first • We watch sausage get made so you can enjoy