Download

1 / 38

380 likes | 392 Views

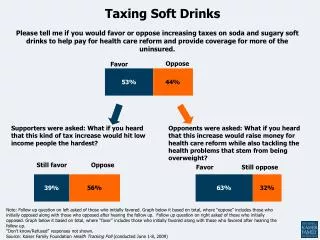

Environmental Taxation Taxing Flights. Cormac O’Dea (Institute for Fiscal Studies) cormac_o@ifs.org.uk. Outline . Some background Rising greenhouse gas emissions Aviation rising particularly quickly Rationale for Environmental Taxation Restructuring Air Passenger Duty Deficiencies

E N D

Environmental TaxationTaxing Flights Cormac O’Dea (Institute for Fiscal Studies) cormac_o@ifs.org.uk

Outline • Some background • Rising greenhouse gas emissions • Aviation rising particularly quickly • Rationale for Environmental Taxation • Restructuring Air Passenger Duty • Deficiencies • Some simulations • Emissions Trading • EU Emissions Trading Scheme Aviation Taxation

Global CO2 emissions, 1971–2005 Source: OECD (2008) Aviation Taxation

Global CO2 emissions, 1971–2005 Source: OECD (2008) Aviation Taxation

Global CO2 emissions, 1971–2005 Source: OECD (2008) Aviation Taxation

Aviation CO2 emissions (UK)1970 - 2006 Source: DEFRA e-Digest of Environmental Statistics Aviation Taxation

Aviation CO2 emissions (UK)1970 - 2006 Source: DEFRA e-Digest of Environmental Statistics Aviation Taxation

UK emissions targets • Kyoto Protocol (1997) • Reduce greenhouse gas emissions 12.5% by 2008–12 compared to 1990 level • Domestic targets • Reduce CO2 emissions by 20% by 2010 compared to 1990 level • Reduce CO2 emissions by 26-32% by 2020 compared to 1990 level • Reduce CO2 emissions by 60% by 2050 compared to 1990 level • International Aviation Emissions are not counted towards any of these targets ? ? Aviation Taxation

Why use taxes? • Environmental damage as a market failure • Externalities argument • Costs of damage to society not taken into account by polluter • Tax increases private costs to match social costs • Generates socially optimal level of pollution – NB not zero! • Balance costs of pollution reduction with benefits of production • Green taxes as “Pigovian Taxes” (Pigou, 1920) • Tax rate should be set to equal the size of the marginal externality at the socially optimal outcome Aviation Taxation

MSC MPC P1 p0 MB q0 q1 Pigovian Tax Number of Flights Aviation Taxation

MSC MPC + t t MPC P1 p0 MB q0 q1 Number of Flights Pigovian Tax Aviation Taxation

Pigovian Tax MSC MPC + t t MPC P1 p0 MB q0 q1 Number of Flights Aviation Taxation

What about a “double dividend”? • Argument often used: green tax revenues used to reduce other distorting taxes • Environmental benefit + more efficiency in tax system = double dividend (Terkla, 1984) • Political soundbites: • “Tax bads not goods” • “Pay as you burn rather than pay as you earn” • Highly controversial • Not clear that green taxes less distortionary. Can exacerbate existing distortionary taxes (Bovenberg and de Mooij, 1994) • Green taxes should be justified by their environmentalimpacts only Aviation Taxation

Revenues in 2006 Source: ONS Environmental Accounts, Autumn 2007 Aviation Taxation

Revenues in 2006 Source: ONS Environmental Accounts, Autumn 2007 Aviation Taxation

What determines the magnitude of the Marginal Social Cost? • Emissions Generated by the engine • Length of the flight • Efficiency of the Engine (Older engines tend to be less efficient) • Congestion at airport (and in the skies) • Effect of noise • Type of plane • Is the airport in a densely populated area? • Time of departure? • The load factor of the plane • The ideal tax will take account of all these, but administrative cost could be prohibitive Aviation Taxation

Aviation Taxes: APD • First charged from November 1994 • Most passengers departing from most UK airports • Varies according to destination (Europe/Other) and, since 2001, travel class • Approximately £2 billion revenue in 2007-08 • PBR 2007: New tax on planes rather than passengers announced • PBR 2008: Plane tax shelved, change in APD instead Aviation Taxation

Air Passenger Duty- Rates Aviation Taxation

Air Passenger Duty- New Rates Aviation Taxation

MSC MPC + t t MPC P1 p0 MB q0 q1 Number of Flights Pigovian Tax Aviation Taxation

Pigovian Tax: Larger Externality MSC MPC + t t P1 MPC p0 MB q0 q1 Number of Flights Aviation Taxation

Which tax base • Passenger? • Simple, but no variation in burden according to load factor • Should it be a fixed charge or percentage (currently no VAT on tickets)? • Flight? • Passengers on empty planes pay more. • Fuel? • Correlates well with emissions, but international agreements prevent using it • Emissions? • Ideal environmental tax, but hard to measure? • Combination of the above? • Keen and Strand (2007) show that the optimal tax is a combination of VAT and fuel duty Aviation Taxation

Illustrative simulation: a per-seat tax • Per-seat tax akin to a flight tax: tax on empty seats has to be passed on or absorbed • Incentives to load aircraft fully • Environmental incentives would require sharper targeting • Data from CAA: departing flights, passengers and number of seats by departure airport and destination (2006) • 1.2 million flights, 120 million passengers • Simulate two per-seat taxes and compare to APD • Various assumptions: • Revenue-neutral relative to APD • No behavioural change by airlines or passengers Aviation Taxation

Simulated taxes • All options generate revenue of £1.96bn • Mean per-passenger payment of £16.58 • Passenger tax (APD) • £10 / £40 per passenger depending on destination • Seat tax • £7.53 / £30.14 per seat depending on destination • Payment depends on load factor explicitly Aviation Taxation

Simulated taxes • Two-part seat tax • Fixed component covering e.g. noise costs, variable component covering distance-based costs • Tax = £S + £(Y x km) • There is an infinite number of S,Y pairs that will yield any given revenue target. • £3.78 fixed charge + £4.22 / 1,000 km • At the cost of additional complexity, could vary: • S by airport of departure or time of day • Y by cleanliness of the engine Aviation Taxation

Per-passenger tax Aviation Taxation

Per-passenger tax Aviation Taxation

Seat tax: example flights Aviation Taxation

Seat tax: example flights Aviation Taxation

Seat tax: example flights • The point of the tax is to reduce the number of flights. Flights with low capacity are obvious candidates for flights to be cut Aviation Taxation

Per-seat tax: winners and losers relative to APD • Winners: flying short distances on fully-loaded aircraft • Losers: flying long distances on empty planes • More complex structure would vary patterns of relative beneficiaries more: • Flying on clean, quiet planes departing airports away from residential areas Aviation Taxation

EU Emissions Trading Scheme • Emissions Trading Scheme (ETS) • An overall emissions cap set. Each tonne of emission requires a permit. • Permits allocated using some mechanism (auctioning/grandfathering). • Firms that don’t use their permits can sell them to firms who exceed their allowance. • Those firms that can abate most efficiently will do so. Cash incentive for abatement. Aviation Taxation

EU Emissions Trading Scheme • Phase 1 2005-2007, Phase 2 2008-2012 • Covers CO2 emissions for relatively big firms in certain industries • Countries allocate permits to firms in their jurisdiction based on past emissions levels • Firms must hold enough permits to cover their emissions at the end of each year • €100/tonne penalty for insufficient permits • “Cap-and-trade” system • Trading establishes ‘market price’ of a tonne of CO2 Aviation Taxation

Aviation and the ETS • Planned reform to APD in 2009 • Current plans from EU environment ministers to bring aviation into ETS from 2012 • Aim to cover all flights to / from EU countries • Plan to auction 10% of permits • Allocations to airlines depending on tonnage-kilometres flown between 2004 – 2006 • What role for aviation duty? • CO2 externality effectively internalised by ETS • Other greenhouse gases, noise and congestion costs provide rationale for ongoing aviation taxes • Ideally auction CO2 permits and target domestic taxes on other externalities Aviation Taxation

How will the ETS and Aviation Duty interact? • If Aviation Duty is maintained at its current level • Passengers pay twice for the same externality. • One of these payments goes to the government, one of these goes to the airlines (as there is an opportunity cost to the airlines using the permit) • Net transfer from passengers to aviation sector • If Aviation Duty is abolished/reduced • Government loses a source of revenue • Net transfer from government to the aviation sector • Aviation Sector gains either way! • This is not surprising, as they’re being endowed with permits which have a value • Either way, the incentive to reduce CO2 emissions is preserved Aviation Taxation

Conclusions • Aviation contributing fast-growing share of UK carbon emissions • Current APD system not particularly well-targeted on environmental costs • Per-flight tax provides scope for sensible reforms • Would create more variation in payments to reflect e.g. load factor, distance, emissions, noise etc. • Complexity in administration to be considered against better targeting of the external costs • Interaction with proposed reform of Emissions Trading Scheme crucial Aviation Taxation

References • Aviation Taxation in the UK • Leicester, A and O’Dea, C (2008), “Aviation Taxation” in Chote, R., Emmerson, C., Shaw, A. and Miles, D. (eds.), IFS Green Budget 2008, (http://www.ifs.org.uk/budgets/gb2008/08chap9.pdf) • What is the marginal cost of flying: • Dings, J. M. W, Wit, R. C. N., Leurs, B. A and Davidson, M. D. (2003), “External Costs of Aviation”, Centre for Energy Conservation and Environmental Technology, http://www.umweltdaten.de/publikationen/fpdf-l/2297.pdf • Pearce, B. and Pearce, D. (2000), “Setting Environmental Taxes for Aircraft: A Case Study of the UK”, CSERGE Working Paper GEC 2000-26, http://www.uea.ac.uk/env/cserge/pub/wp/gec/gec_2000_26.pdf • UK Green Tax Instruments • Leicester, A. (2006), “The UK Tax System and the Environment”, (http://www.ifs.org.uk/comms/r68.pdf) • Etheridge, B. & Leicester, A. (2007), “Environmental Taxation” in Chote, R., Emmerson, C., Leicester, A. and Miles, D. (eds.), IFS Green Budget 2007, (http://www.ifs.org.uk/budgets/gb2007/07chap11.pdf) • UK Green Tax Revenues • ONS Environmental Accounts (http://www.statistics.gov.uk/statbase/Product.asp?vlnk=3698 for latest, published twice a year) • HM Treasury Consulation • Aviation: A Consulation (http://www.hm-treasury.gov.uk/consultations_and_legislation/aviation/consult_aviation_duty.cfm) Aviation Taxation

References • Emissions Statistics Data • Global: OECD Factbook 2008 (http://www.sourceoecd.org/factbook) • UK: DEFRA (http://www.defra.gov.uk/environment/statistics/globatmos/download/xls/gatb05.xls) • Theoretical Discussion of Green Taxes • Keen M. and Strand J., ‘Indirect taxes on international aviation’, Fiscal Studies, 2007, 28(1): 1–41 • Pigou, A. C. (1920), The Economics of Welfare, (http://www.econlib.org/library/NPDBooks/Pigou/pgEWtoc.html) • Smith, S. (1995), “ ‘Green’ Taxes and Charges: Policy and Practice in Britain and Germany”, (http://www.ifs.org.uk/comms/r48.pdf) – Chapters 2 & 3 • Stern, N. (2006), The Stern Review of the Economics of Climate Change, (http://www.tinyurl.com/vgzxv) • Double Dividend • Terkla, D. (1984), “The Efficiency Value of Effluent Tax Revenues”, Journal of Environmental Economics and Management, Vol. 11, pp. 107–123 • Goulder, L. (1995), “Effects of Carbon Taxes in an Economy With Prior Tax Distortions: An Intertemporal General Equilibrium Analysis”, Journal of Environmental Economics and Management, Vol. 29, pp. 271–297 • Bovenberg, A. & de Mooij, R. (1994), “Environmental Levies and Distortionary Taxation”, American Economic Review, Vol. 84, No. 4, pp. 1085–1089 Aviation Taxation