Download

1 / 10

100 likes | 110 Views

This article focuses on the challenges faced in seasonally adjusting short time series and handling them during economic crises, including the instability of the data and the need for frequent parameter checks. It also discusses the impact of economic crises on seasonal adjusted series and the revision policies to be considered. Examples and proposals for treatment are provided.

E N D

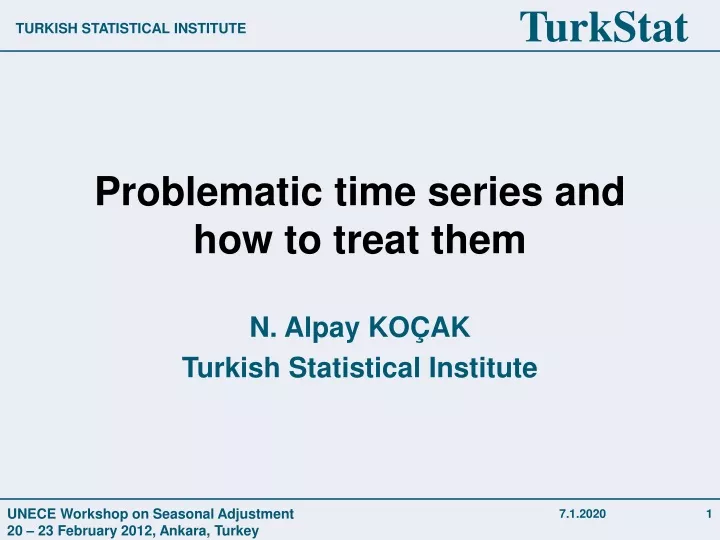

Problematic time series and how to treat them N. Alpay KOÇAK Turkish Statistical Institute

Seasonal adjustment of short time series • For some series that are too short to be seasonally adjusted using either TRAMO-SEATS or X-12-ARIMA, it ispossible to adjust them using alternative, less standard, procedures. For series that are long enough to run X-12-ARIMA or TRAMO-SEATS but remain quite short (3-7 years), some instability problems can appear. Severalempirical comparisons have been done to investigate the relative performance of X-12-ARIMA and TRAMOSEATSon short time series. • As a general rule when the series are shorter than seven years, the specification of the parameters used for pretreatmentand seasonal adjustment has to be checked more often (e.g. twice a year in order to deal with thehigher degree of instability of such series).

Seasonal adjustment of short time series • Series shorter than 3 years should not be seasonally adjusted. Seasonal adjustment of short time series (3-7 years) should be performed, whenever possible, with standard tools. • Moreover back-recalculated time series (even non-official) should be used to extend the sample and stabilise seasonal adjustment when they are reliable for estimating a seasonal component. • Simulations on relative performances of the existing standard tools for adjustment of short series should be carried out. Users should be informed of the greater instability of seasonally adjusted data for short series, and of methods used. • Clear publication policy rules should be defined. The settings and parameters for seasonal adjustment should be checked more than once per year.

Seasonal adjustment of short time series (Proposal) • Use TRAMO&SEATS for the series longer than 3 years! • 1) Find the best model at the start of the year, 2) fix the model specification and parameters values, and position of outliers and type of the calendar effects, 3) Check parameter stability twice a year for entire series! • Do not forget that Airline model (0,1,1)(0,1,1) may be the most representative model for a series!

Mongolia Example Intitial Assumptions: Model is Airline, Weekdays (1 regressor) and Moving Holidays (1 regressor) are in the model. Log/Level selectioin is automatic. Airline parameters, and calendar effect parameters are estimated, every quarter. Orange : Statistically significant at 10% Yellow : Statistically significant at 5% Green : Statistically significant at 1%

Seasonal adjustment in times of economic crises • In case of economic crises or turmoil, economic time series shows sudden changes in tendency, (rapidly up or down) • Given that a time series is represented by an ARIMA modelin the process process of seasonal adjustment, the changes in ARIMA model can be seen mostly. • Specification of ARIMA model, • Parameters of ARIMA model, • Types, dates and parameters of outliers • Parameters of calendar effects • When new data become available at the end of the data, huge revision of old published data probably can be seen if any of properties above mentioned has been changed.

Seasonal adjustment in times of economic crises • Actually, this issue is a matter of fact that which revision policy is chosen for the series. • Current seasonal adjustment → More revision • Concurrent seasonal adjustment → Less revision • Semi-concurrent revision → Mild revision

Seasonal adjustment in times of economic crises • Do not take into account an last observation as an outlier. • You can not judge this point as an AO or LS

Effect of 2009Q1 Economic Crisis on Seasonal Adjusted Series