Download

1 / 22

230 likes | 249 Views

Gain insights into the CFPB's role in private education loans, relevant reports, and future projections for consumer protection. Learn about student debt initiatives and upcoming regulations from this informative presentation.

E N D

CFPB Update John Dean Washington Partners, LLC January 2012

About this presentation • This presentation is not legal advice and should not be relied upon as such. • Information included represents the views and perspectives of the presenter and not Washington Partners, LLC, the Consumer Bankers Association, or any member of CBA. • Information is believed to be accurate as of the date of this presentation.

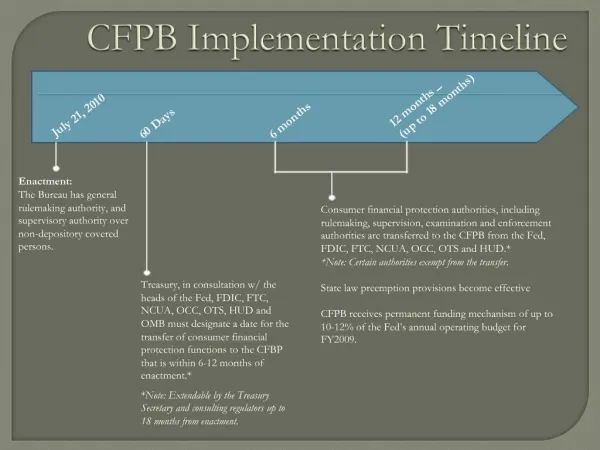

The CFPB • In a nutshell, with a director now in place CFPB has full rulemaking, supervision, and enforcement authority relating to consumer protection that were previously exercised by the Fed, FDIC, OCC, and FTC. Covered statutes include Truth-in-Lending, Fair Credit, and Fair Lending. • New authorities include rulemaking and enforcement relating to "unfair, deceptive or abusive" acts and practices. (Could loans made by for-profit schools be an early area of activity?)

The CFPB and Student Loans Private Education Loans are a major priority of the Bureau: • Section 1077 Report. • Private Student Loan Ombudsman. • Know Before You Owe. • Student Loan Repayment Guidance. • Focus on Collections. • Enforcement Actions.

Private Education Loan Report • Section 1077 of Dodd-Frank—due July 21, 2012. • Report to be written with involvement of ED, the Department of Justice, and the FTC. • Report is likely to include recommendations (including legislative changes) for “effective” disclosures and communications with borrowers (including co-signers) • CFPB collecting data for use in writing report.

Private Loan Report Report Contents: • Definition of market, including retrospective. • Attempt to understand market drivers. • Focus on use of private loans (arguably with presumption that loans are sometimes used unnecessarily). • A review of private loan borrowers

Private Loan Report Report Contents: • Review of lenders (including non-banks and schools). • Fair Lending-relevant data—underwriting criteria (i.e., use of school criteria). • Review of loan products. • Inquiry into existing consumer protections. • Recommendations. http://www.dodd-frank-act.us/Dodd_Frank_Act_Text_Section_1077.html.

Are recommendations already written? • “Consumer advocates” don’t need a report to know what is needed. • Will the CFPB simply adopt the myriad of already outstanding recommendations made by these groups? Will the section 1077 report findings really only be “supporting information” for recommendations already decided upon?

Project on Student Debt Agenda Help more Americans complete meaningful education and training at a reasonable cost • Improve and promote tools to help students make wise choices about costs and debt • Strengthen policies to protect students and taxpayers from waste, fraud and abuse • Promote strong and effective regulation of career education programs Strengthen consumer protections for private student loan borrowers • Protect borrowers from unfair and deceptive private loan practices • Require lenders to certify loans with the borrower's school before disbursing funds • Improve reporting and data collection about private student loans • Treat private student loans like other consumer debt in bankruptcy . http://projectonstudentdebt.org/initiative_view.php?initiative_idx=6.

Projections on Findings • Current Title X Disclosures are not carefully read by borrowers and thus to not achieve the consumer education and protection afforded. • Significant unnecessary borrowing is occurring. • Available data is inadequate to determine compliance with Fair Lending, but evidence suggests there may be violations. • Some products (especially loans made by proprietary schools) are abusive. Debt service often exceeds ability of borrower to repay. • Current product diversity confuses borrowers, especially in terms of flexible repayment. This diversity is not in best interest of borrowers. • Loan servicing practices often contribute to delinquency/default. • Borrowers do not have easy enough access to consumer help in the event of problems.

Projections on Recommendations • Increased borrower disclosure intended to discourage “unnecessary” borrowing, especially where ability to repay may be questionable. • New disclosure procedures to assure information is received and acted upon. • Increased federally-mandated data collection by the CFPB for use in enforcing Fair Lending and other consumer protection laws. • Consideration of servicing standards for private education loans. • Promotion of additional resources for borrowers with repayment problems; include info on such resources in disclosures.

Private Education Loans: Nov. 17 RFI • On Nov. 17, the CFPB issued a RFI seeking data and comment on what information would help students make informed decisions about which financial services and products are right for them and what approaches would best assist recent graduates facing (or about to face) difficulty making private education loan payments. • The questions are grouped into four broad categories: (1) scope and use of private education loans, (2) information and shopping for private education loans, (3) institutional loans, and (4) repayment. http://www.consumerfinance.gov/notice-and-comment/request-for-information-regarding-private-education-loans-and-private-educational-lenders/.

November 17 RFI • Some questions appear drafted to solicit responses that will support increased data collection and other policy outcomes already identified by consumer advocates. • Lenders limiting responses to RFI questions to those on which substantive, supportable answers are possible. • Will CFPB reject “speculative” responses submitted by other groups?

“Know Before You Owe” “For generations, a college degree has helped Americans . . . achieve a better future. But the increasing cost of higher education, the financial crisis, and continuing tough economic times mean that more students will rely on student loans to pay for tuition and make ends meet while in school. Students should be able to understand the costs, risks, and benefits of the loans they will use to help pay for the school of their choice.”

“Know Before You Owe” • CFPB: “The school financial aid offer is one of the most important ways students receive this information. But we’ve heard from students, college counselors, and community organizations that many of these offers don’t always effectively deliver this information. They may be filled with jargon or difficult to compare, and they may not clearly distinguish loans from other forms of aid.” • At Congress’ direction, ED will publish a model format for the financial aid award offer letter. http://www2.ed.gov/policy/highered/guid/aid-offer/index.html.

Private Student Loan Ombudsman Rohit Chopra announced as first Private Student Loan Ombudsman. FUNCTIONS OF OMBUDSMAN:(1) in accordance with regulations of the Director, receive, review, and attempt to resolve informally complaints from borrowers of loans described in subsection (a), including, as appropriate, attempts to resolve such complaints in collaboration with the Department of Education and with institutions of higher education, lenders, guaranty agencies, loan servicers, and other participants in private education loan programs;(2) establish a memorandum of understanding with the student loan ombudsman established under section 141(f) of the Higher Education Act of 1965 (20 U.S.C. 1018(f)), to ensure coordination in providing assistance to and serving borrowers seeking to resolve complaints related to their private education or Federal student loans;(3) compile and analyze data on borrower complaints regarding private education loans; and(4) make appropriate recommendations to the Director, the Secretary, the Secretary of Education, the Committee on Banking, Housing, and Urban Affairs and the Committee on Health, Education, Labor, and Pensions of the Senate and the Committee on Financial Services and the Committee on Education and Labor of the House of Representatives. See: http://www.dodd-frank-act.us/Dodd_Frank_Act_Text_Section_1035.html.

Other Initiatives: Student Debt Repayment Assistant Computerized guidance to borrowers on repaying their loan: “While our Student Debt Repayment Assistant can’t give you advice for your exact situation, we hope it can point you in the right direction and help you learn about some of your options.” “Call your non-federal loan servicer and ask what options are available to you. Most of the big lenders say that they have alternate payment programs for borrowers who might not be able to make a full payment. You can often find out about these options on your servicer’s website.” http://www.consumerfinance.gov/students/repay/.

“Abusive” Acts or Practices Here's what the CFPB Supervision and Examination Manual defines as “abusive” acts or practices: • Materially interferes with the ability of a consumer to understand a term or condition of a consumer financial product or service or • Takes unreasonable advantage of – • A lack of understanding on the part of the consumer of the material risks, costs, or conditions of the product or service; • The inability of the consumer to protect its interests in selecting or using a consumer financial product or service; or • The reasonable reliance by the consumer on a covered person to act in the interests of the consumer. • Although abusive acts also may be unfair or deceptive, examiners should be aware that the legal standards for abusive, unfair, and deceptive each are separate.“ The term "abusive" is more subjective and more extensive than the previously established standards of "unfair or deceptive." The CFPB manual provides no concrete examples. A full understanding of what CFPB will find to be a violation of this standard can only be gained as we observe examination findings. Link to CFPB examination manual: http://www.consumerfinance.gov/guidance/supervision/manual/.

Collection Agencies • The FTC, the agency previously charged with enforcement and rulemaking under the FDCPA, had limited jurisdiction over nonprofit debt collectors. By some accounts, it’s rulemaking and enforcement under the FDCPA was “less threatening” than that is expected from the CFPB. • Richard Cordray was a critic of collection agencies while Ohio AG. In September 2009, heissued a public warning to collectors based on consumer complaints. In April 2010, he announced a large settlement with National Enterprise Systems based on complaints the company was harassing consumers while attempting collection.

Office of Financial Education • CFPB Website: “Coming Soon” • Expected to be active on the Financial Literacy and Education Commission and the President’s Advisory Council on Financial Capability. http://www.treasury.gov/resource-center/financial-education/Pages/Advisory.aspx and http://uscode.house.gov/download/pls/20C77.txt • Part of Office of Consumer Education & Engagement • Same CFPB silo as “Office of Students,” “Office of Seniors,” “Office of Servicemembers,” etc. • Office headed by Gail Hillebrand, formerly senior attorney with Consumers Union.

Additional Resources CBA Org Chart of the CFPB: http://www.cbanet.org/files/GRFiles/CFPB/Consumer%20Financial%20Protection%20Bureau%27s%20Planned%20Organization%20FINAL%20LA.pdf.

Thank You John Dean Washington Partners, LLC jdean@jdean-law.com 202.289.3900