Download

1 / 15

150 likes | 310 Views

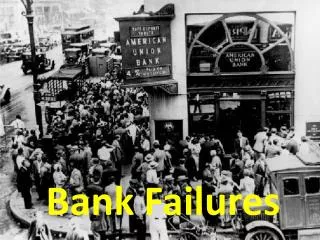

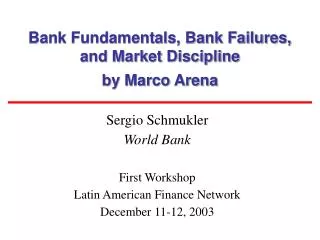

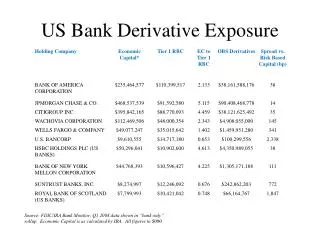

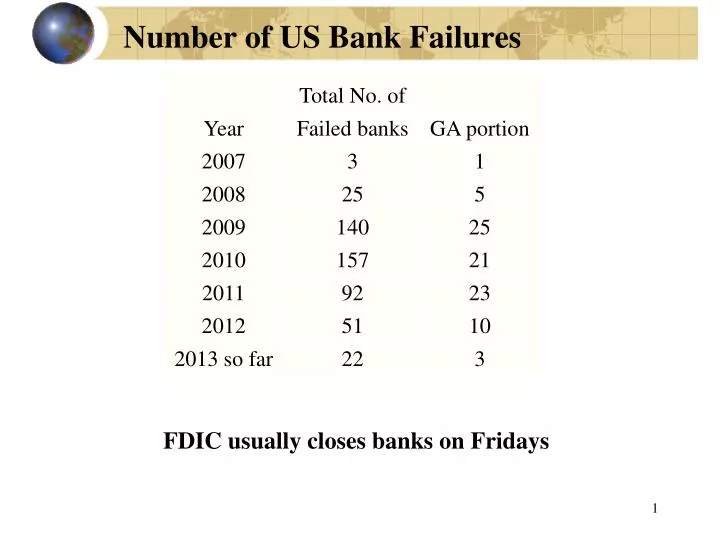

Number of US Bank Failures. FDIC usually closes banks on Fridays. 20 in Loans Go Uncollectable. Solvent Bank. Assets Liabilities. Reserves 30 Loans 90 Invests 90 Premises 5. Deposits 200 Capital 15. Insolvent Bank.

E N D

Number of US Bank Failures FDIC usually closes banks on Fridays

20 in Loans Go Uncollectable Solvent Bank Assets Liabilities Reserves 30 Loans 90 Invests 90 Premises 5 Deposits 200 Capital 15 Insolvent Bank Assets Liabilities Reserves 30 Loans 70 Invests 90 Premises 5 Deposits 200 Capital -5 FDIC closes bank

Market Rate of Interest Rate • Market rate of interest performs an allocative function by assuring • SSUs rate will be low enough so someone will borrow from them • DSUs rate will be high enough so someone will lend to them. • In addition to Fed, interest rates affected by business opportunities (production opportunities, in book) in the economy. • The lower the rate of interest, the greater the number of business ventures that should be profitable. • “time preference for consumption”

Loanable Funds • Sources of loanable funds • consumer savings • business savings • state/local government surpluses • federal government surpluses • central bank action that increases money supply • Uses for loanable funds • consumer credit purchases • business investment • state/local government deficits • federal government deficits

Nominal vs. Real Rate of Interest Nominal interest rate is the observed rate (the market rate). Real rate of interest is nominal rate minus inflation. Real rate of interest has historically been between about 2% and 4%. Nominal interest rate consists of the real interest rate plus extra amount to compensate for the erosion in purchasing power caused by inflation.

Fisher Equations • Let • idenote nominal rate of interest • r denote real rate of interest (i.e., rental rate) • denote expected rate of inflation. Regular Fisher equation Exact Fisher equation

Components of Exact Fisher Equation The three terms see to it that lender gets compensated for: • rental of purchasing power • anticipated loss of purchasing power on the principal • anticipated loss of purchasing power on the interest

Example 1 • Normally, when we lend money, we do it to increase purchasing power. Let’s be precise about taking inflation into account. • We lend $100 for one year under the condition that the $100 gains 5% in purchasing power. Expected inflation is 8%. What interest rate should we charge?

Example 2 Going to lend a company $3 billion to help it through a financial crisis at a rental rate of 10% plus compensation for 4% inflation. Boss says figure out interest rate to charge. What is difference between regular and exact?

Realized Real Interest Rate • ex ante means based upon anticipated effects (i.e., what lies ahead) • ex post means based upon analysis of past performance (i.e., what lies behind) • ex ante, we assume r and forecast (expected) • ex post, we know both iand (actual) • Note difference between and

Other Forms of Fisher Equations regular for ex ante use: exact for ex ante use: regular for ex post use: exact for ex post use:

Example 3 Suppose a loan were set up with a nominal interest rate of 12%. What would be realized real rate of return if inflation turned out to be 4%? approx: exact:

When Inflation Deviates From Anticipated • Inflation greater than anticipated: benefits borrowers. Results in an unintended transfer of PP from lender to borrower. • Inflation less than anticipated: benefits lenders. Results in an unintended transfer of PP from borrower to lender. Suppose i is constructed with a specific anticipated rate of inflation built in.

What is Fisher Effect? …that embedded in nominal interest rates are inflation expectations.