Download

1 / 8

80 likes | 240 Views

S Corporations. Income is only taxed once – to shareholders No corporate income tax Doesn’t matter if income is distributed Requirements < 100 shareholders Traditional family considered one shareholder Shareholders must be individuals, estates, grantor trust One class of stock

E N D

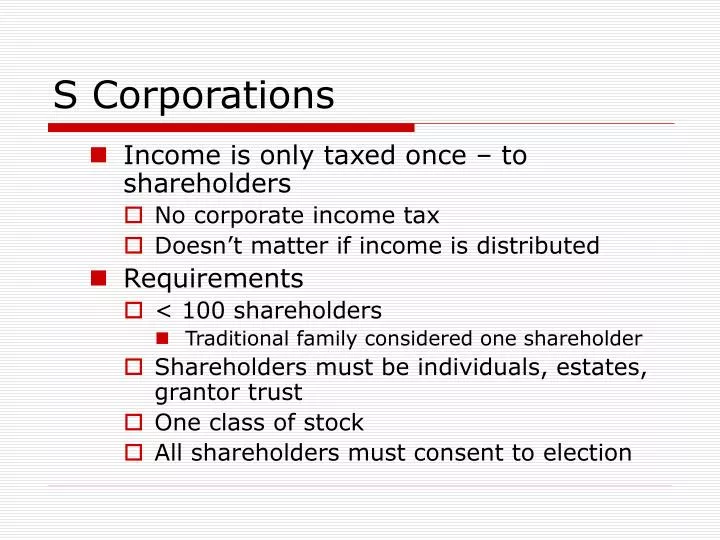

S Corporations • Income is only taxed once – to shareholders • No corporate income tax • Doesn’t matter if income is distributed • Requirements • < 100 shareholders • Traditional family considered one shareholder • Shareholders must be individuals, estates, grantor trust • One class of stock • All shareholders must consent to election

S corporations • Losses limited to basis • Basis: cash invested • Basis increased by income, loans to S corp • Basis reduced by losses • Losses limited by basis carried over until basis is created

C corporations • Corporate income tax rates • 34 – 35%, generally, on income above $75,000 • More than all but the top individual rates for MFJ with taxable income above $350,000 • Dividends paid: not deductible • Currently taxed at capital gains rates to recipients • Most taxpayers: 15% • Dividends received: • Own < 20% company: 70% not taxed • Own > 80%: not taxable

C corporations • Capital gains: taxed as ordinary income • Capital losses: can only offset capital gains • Excess carried back three years; forward five years

C corporations • AMT • Pay AMT if more than tax computed using tax rates • Large income, no income tax, makes Congress sad • Taxable income calculated differently for AMT purposes • AMTI • ACE adjustment: Book Income vs. Taxable Income

C Corporations • Losses • Carried back 2 years, forward 20 years • Accumulated Earnings • Don’t want corporations to not pay dividends • What are the plans for the funds? • Excessive compensation • To avoid dividends?

LLCs • Limited liability: like a corporation • But no corporate income tax • Income taxed to owners like a partnership • Rules vary by state • Some states require multiple owners • Corporations, partnerships can be owners (unlike S corp) • LLPs • Similar to LLCs but only professionals can own (doctors, attorneys, etc.)

LLCs • Can choose to be taxed as either a partnership or C corporation • Can change: • Within 75 days on start of year of desired change • Can’t change again for five years • But can change within first five years of entity