Download

1 / 20

200 likes | 221 Views

Explore China's economic transitions post-Global Financial Crisis: shifts in consumption, investment, trade exports, policy responses, imbalances, and recent structural reforms affecting growth. Discover key factors contributing to economic evolution and challenges faced in maintaining stability and growth.

E N D

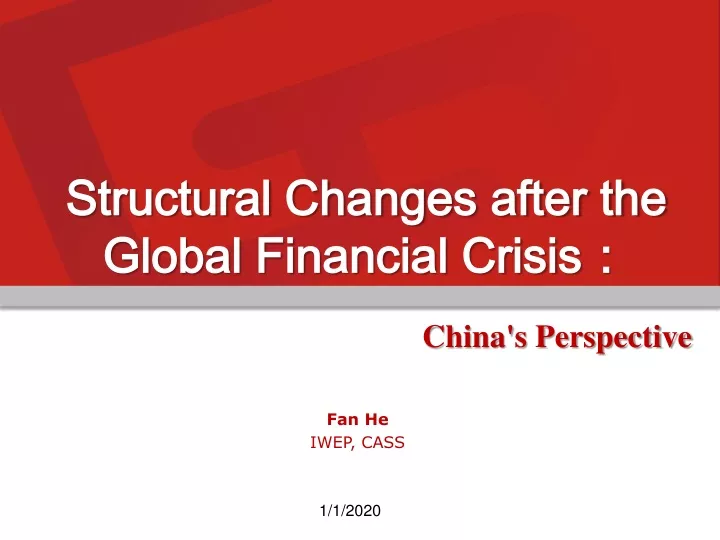

Structural Changes after the Global Financial Crisis: China's Perspective Fan He IWEP, CASS

Structural imbalances before 2007 • Weak consumption vs. Strong investment • From 2000-2007, the share of private consumption to GDP decreased 46.4% to 36.0%,the share of Investment to GDP increased from 35.2% to 41.7% • Why? • (1) The labor income share GDP dropped from 51.4% to 39.7%. • (2) Weak social security leads to precautionary saving of households. • (3) High saving rate for the enterprises. • (4) Inequality in distribution of wealth • (5) Financial repression.

Structural imbalances before 2007 • Underdeveloped service sector vs. very competitive manufacturing • The share of service sector in China’s GDP just increased from 39.0% to about 42% during 2000-2007 • China’s value added (% of GDP) in manufacturing is much higher than other emerging countries, which is 32.9% in 2007 (Brazil:15.4%, India: 16.0%, Russia: 17.6%) • Why? • (1)Globalization and trade liberalization. • (2)Free entry in the manufacturing sector but tight control on service sectors. • (3) No incentives for the local government to encourage the development of service sector. • (4)Price distortion.

Structural imbalances before 2007 • Heavy reliance on foreign demand • The share of exports in GDP increased from 20.8% to 35.2% from 2000 to 2007,and the share of net exports reached 8.8% • Then? • (1) Trade surplus. • (2) More than 3 trillion USD foreign exchange • (3) Environment pollution. • (4) Energy security.

Stimulus Policy after Crisis • 2008-11-18 “4 trillion yuan plan”. 1%, Health, Education and so on 4%, Industrial Innovation 7%, Indemnificatory Housing 8.75%, Environment 9.25%, Rural Welfare 25%, Reconstruction 45%, Infrastructure Figure 1 Destination of “4 trillion yuan plan” • Destination of funds

Stimulus Policy after Crisis • It’s rather a monetary stimulus than a fiscal one • Other sources include: • (1) Local government bonds • the scale of local government remains small, about 200 billion yuan per year • (2) Local government-backed investment platform • its money is mainly from bank credit. Other sources: 2.88 trillion Central government budget: 1.18 trillion Figure 2 Source of “4 trillion yuan plan”

Economic Performance after 2008 Figure 3 China’s Economic Growth from 2008 to present (Quarterly, YoY, %) Financial Crisis A new round of slowdown “4 trillion plan”

Deterioration of Structural imbalances • Deterioration in internal imbalance • (1)Investment explodes • The share of investment in GDP increased by another 8 percentage in 4 years between 2008 and 2011 • (2)Too much investment in infrastructure building • It counts nearly half of the “4 trillion policy” • Mainly “Rail way, high way and other infrastructure” • (3)State-owned sector resurges • Growth rate of investment in state-owned sector increase(18% to 21%) in 2009-2011, while private sector drops (48% to 38% )compared to 2005-2008

Deterioration of Structural imbalances • (3)Heavy reliance on local government and bank credit • 2010, China published the only data of local government’s debt, which is 10,717 billion yuan, more than 200% of local government’s revenue in 2011 Figure 4 Credit expansion in RMB, SA , 100 million yuan

Hard landing or soft landing? • China is faced with a new round of slow down after 2011, with growth rate’s graduate declining to below 8% YoY growth in 2012Q2 Figure 5 Growth rate after 2009, YoY, %

Hard landing or soft landing? • How does slowdown happen? • Macro-Policy is the main reason • In 2012H1, policy tightening explains 52% of the decrease in investment , most significant are investment in real estate sector (27%) and infrastructure sector (25%). • Policy tightening: • (1) end of the stimulus policy • (2) to suppress the housing price • (3) to control the inflationary pressure after the stimulus (CPI reached 6.5% in July, 2011, and is above 4% in 2011)

Silent revolution in 2012 • Consumption becomes strong • Growth rate of consumption per capita is 9.3% in 2012Q2, which is higher than 6.1% in 2010Q2 and 8.4% in 2011Q2, and is also above the average rate between 2003 and 2012 Figure 6 Growth in consumption per resident(after moved average), YoY, %

Silent revolution in 2012 • Structure of investment is improving in 2012H1 • Investment growth rate increases in service sectors science & technology (46% v.s 25%) ICT (43% v.s 3%), finance(130% v.s 28%) • The increase of investment in private sector outpaced that in the public sector. East • the growth rate of investment in west and mid China outsized that of east China in 2012H1 West Mid

Silent revolution in 2012 • Industrial structure is changing • There is a divergence in manufacturing PMI and non-manufacturing PMI after April, 2012 Figure 7 Manufacturing PMI and non manufacturing PMI, SA

Why structural change? • Can not be credited to the government. Thanks to the market forces. (1) Consumption rise because of fundamental changes, especially the change of demographic profile, causing a lower saving rate Figure 8 Share of population aged between 15-64, %

Why structural change? (2) exports sector is adjusting because of increasing labor cost Figure 8 Average minimum wage in different region of China, Yuan

Why structural change? • (3) Investment redistribution in sectors is the result of mixed events: • Slumped foreign demand, and thus there is no motive to invest more in export sector • Weak internal demand in steel and other industries, plus increasing cost in energy and labor • Improvement in financial repression

Implication • (1)Growth drops in the short run, but there is a positive structural change • (2)trade surplus will be back to a reasonable level, and China’s ODI will expand, both for market seeking and resource seeking, thus external imbalances will diminish gradually • (3)there are also short run factors which may cause these changes: • Slowing invest make consumption “seems ” strong and structure “seems” change • Policy support on ICT and other technology intensive industries

Australia’s opportunity and challenge • Bilateral trade is increasing fast, but it’s mainly a mining story. • More opportunities for high-quality agricultural produces, high-end manufactured products. • A ready market for Australian service sector. • Is Australia ready?

Thank you Fan He IWEP, CASS LOGO