Download

1 / 2

0 likes | 19 Views

Revocable trusts are a type of trust that can be established, modified, or revoked while the grantor is still alive. After it has been established, an irrevocable trust, including a living trust inheritance tax that becomes such upon the grantor's demise, cannot be changed or canceled.

E N D

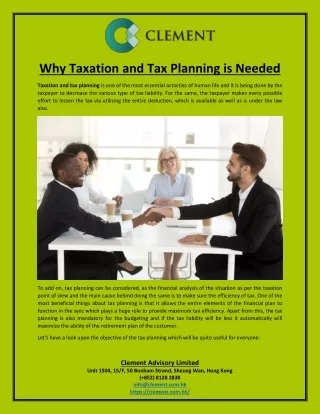

Why Living Trust Inheritance Tax Is Needed Typically, trust beneficiaries rather than the trust itself— pay taxes on the income distributions they receive. Distributions from the trust's principal, or the money that was first deposited into the trust, are not subject to taxation by beneficiaries. When a trust makes a distribution, it deducts the income from its tax liability and sends the beneficiary a Schedule. On it, which specifies how much of their payout interest income as opposed to principle is, the receiver can deduct a specific portion of the distribution as taxable income. A trust is a fiduciary arrangement in which one party, the trustor or grantor, gives another, the trustee, the power to hold onto assets for the benefit of a third, the beneficiary. To offer lea gal protection and protect assets, trusts are typically created as part of estate planning. Trusts can make a guarantee that assets are allocated judiciously and in accordance with the grantor's objectives. Additionally, trusts can help avoid probate and lower estate and inheritance taxes. IWC Probate And Will Services Suite 43-45 Airport House, Purley Way, Croydon, Surrey CR0 0XZ Phone: 020 8150 2010 admin@iwcprobateservices.co.uk https://www.iwcprobateservices.co.uk/

How to get an inheritance in a living trust Revocable trusts are a type of trust that can be established, modified, or revoked while the grantor is still alive. After it has been established, an irrevocable trust, including a living trust inheritance tax that becomes such upon the grantor's demise, cannot be changed or canceled. Depending on the type of income the trust gets and whether the trust is revocable or irrevocable, different tax regulations apply to beneficiaries. Interest versus Principal Distributions. Taxes are not due from trust beneficiaries on distributions made from the trust's principal. The Internal Revenue Service assumes that this money was taxed prior to entering the trust. Gains from the trust are taxed as income, either to the beneficiary or to the trust. The beneficiary's distribution is subtracted from the accrued principal after first deducting it from income for the current year. The principal is the first donation plus any additional payments, and the recipient or the trust may be subject to capital gains tax. IWC Probate And Will Services Suite 43-45 Airport House, Purley Way, Croydon, Surrey CR0 0XZ Phone: 020 8150 2010 admin@iwcprobateservices.co.uk https://www.iwcprobateservices.co.uk/