Download

1 / 5

50 likes | 183 Views

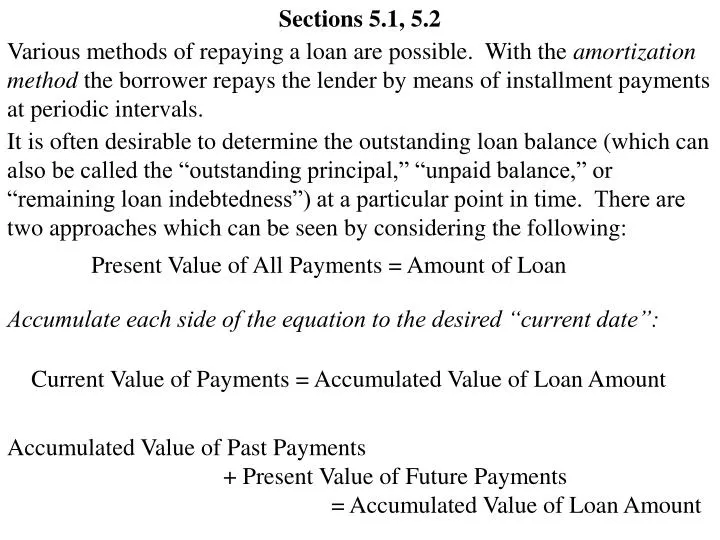

Sections 5.1, 5.2. Various methods of repaying a loan are possible. With the amortization method the borrower repays the lender by means of installment payments at periodic intervals.

E N D

Sections 5.1, 5.2 Various methods of repaying a loan are possible. With the amortization method the borrower repays the lender by means of installment payments at periodic intervals. It is often desirable to determine the outstanding loan balance (which can also be called the “outstanding principal,” “unpaid balance,” or “remaining loan indebtedness”) at a particular point in time. There are two approaches which can be seen by considering the following: Present Value of All Payments = Amount of Loan Accumulate each side of the equation to the desired “current date”: Current Value of Payments = Accumulated Value of Loan Amount Accumulated Value of Past Payments + Present Value of Future Payments = Accumulated Value of Loan Amount

Present Value of Future Payments = Accumulated Value of Loan Amount – Accumulated Value of Past Payments Prospective Method = Retrospective Method Each side of this equation represents one of two approaches which are equivalent in general: With the prospective method, the outstanding loan balance at any point in time is equal to the present value at that date of the remaining payments. With the retrospective method, the outstanding loan balance at any point in time is equal to the original amount of the loan accumulated to that date less the accumulated value at that date of all payments previously made. The outstanding loan balance at time t will be denoted by Bt and when desirable, Btp and Btr will be used to distinguish between the prospective and retrospective methods respectively.

Consider a loan of at interest rate i per period being repaid with payments of 1 at the end of each period for n periods. For 0 < t < n, the outstanding loan balance after exactly t periods is a – n| Btp = from the prospective method, a ––– n–t| Btr = from the retrospective method. (1 + i)t– a – n| s– t| Prove algebraically that Btr = Btp . 1 – vn —— i (1 + i)t– 1 ———— i (1 + i)t– = (1 + i)t– = a – n| s– t| (1 + i)t– vn–t – (1 + i)t+ 1 —————————— = i 1 – vn–t ——— = i a ––– n–t|

A loan is being repaid with 16 quarterly payments, where the first 8 payments are each $200 and the last 8 payments are each $400. If the nominal rate of interest convertible quarterly is 10%, use both the prospective method and the retrospective method to find the outstanding loan balance immediately after the first six payments are made. With the prospective method, we have B6p = 200(v + v2) + 400v2(v + v2 + … + v8) = 400(v + v2 + … + v10) – 200(v + v2) = 400 – 200 = a –– 10| a – 2| 400(8.75206) – 200(1.92742) = $3115.34 With the retrospective method, we have that the original loan amount is 200(v + v2 + … + v8) + 400v8(v + v2 + … + v8) = 400(v + v2 + … + v16) – 200(v + v2 + … + v8) = 400 – 200 = 400(13.05500) – 200(7.17014) = $3787.97 a –– 16| a – 8| We now find B6r = $3787.97(1.025)6– 200 = s– 6| 4392.90 – 200(6.38774) = $3115.35

A loan is being repaid with 15 annual payments of $500 each. At the time of the tenth payment, the borrower wishes to pay an extra $500 and then repay the balance over 6 years with a revised annual payment. If the effective rate of interest is 8%, find the amount of the revised annual payment. The loan balance after ten years (prospectively) is B p = 500 = 10 a – 5| 500(3.99271) = $1996.355 With the extra $500 payment, the loan balance is $1496.35 If X represents the revised annual payment, then X = 1496.35 a – 6| X = 1496.35 / 4.62288 = $323.68